Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

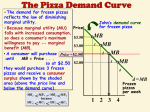

Answers to Practice Exam 2 1. What will happen to the equilibrium price and quantity of pizza if a hamburger place opens next door and the price of dough decreases? A. Price will fall and the effect on quantity is ambiguous. B. Price will rise and the effect on quantity is ambiguous C. Quantity will fall and the effect on price is ambiguous D. Quantity will rise and the effect on price is ambiguous 2. If two goods are compliments, their cross-price elasticity will be A. Positive B. Negative. C. Zero D. equal to the difference between the income elasticities of demand for the two goods 3. A company is willing to sell 5000 units of their good at $90 and they are willing to sell 3000 units of their good at $70. What is the elasticity of supply for this good? A. 4 B. .25 C. 3 D. .333… E. 2.0. F. .5 4. If buyers do not adjust their quantity demanded at all in response to a change in price, the price elasticity of demand is A. Inelastic B. Unit Elastic C. Elastic D. Perfectly Elastic E. Perfectly Inelastic. 5. Total surplus in a market with a tax is equal to A. Value to buyers - cost of sellers + tax revenue B. Amount received by sellers - amount paid by buyers + tax revenue C. Consumer Surplus +Producer Surplus + Tax revenue – Dead weight loss D. Amount received by sellers - costs of sellers + tax revenue 6. Dead weight loss is equal to: A. Consumer Surplus*1/2*total quantity B. Producer Surplus *1/2*lost quantity caused by the tax C. Amount of the tax* 1/2 * total quantity D. Amount of the tax* 1/2* lost quantity caused by the tax Label the following Chart: 7. Which letter represents the Producer Surplus? A. B. C. D. E. F. G 8. Which letter represents the Price for Buyers? A 9. If the government removes a price ceiling from the market, then the price paid by the buyer will A. increase and the quantity sold in the market will increase. B. increase and the quantity sold in the market will decrease C. decrease and the quantity sold in the market will increase D. decrease and the quantity sold in the market will decrease 10. A legal minimum price at which a good can be sold is called a price A. support B. ceiling C. floor. D. subsidy 11. The dead weight loss in a market will be smallest when the elasticity of demand is A. Perfectly elastic B. Perfectly inelastic C. Unit elastic D. Elastic E. Inelastic 12. Which of the following is not studied in welfare economics/the allocation of resources? A. How much of each good is produced B. Why the good is produced C. Which producer produces it D. Which consumer consumes it 13. When a tax is placed on the sellers of sports cars A. sellers bear the entire burden of the tax B. buyers bear the entire burden of the tax C. burden of the tax will be shared by the buyers and the sellers, but the division of the burden is not always equal. D. burden of the tax will be always divided equally between the buyers and the sellers Buyers Jack Gary Lisa Tyler Willingness to pay $30 $50 $15 $65 14. How many units are purchased when the marginal buyer is willing to pay $22? A. 1 B. 2 C. 3 D. 4 15. What is the consumer surplus when the price is set at $15? A. 0 B. 160 C. 100 D. 35 E. Incalculable 16. What is the producer surplus when the price is set at $15? A. 0 B. 160 C. 100 D. 35 E. Incalculable 17. A price ceiling will create A. Deadweight loss B. a surplus C. a shortage D. tax revenue 18. Which good would have the smallest Dead Weight Loss, insulin or Advil? A. Insulin B. Advil C. They have the same Dead Weight Loss because they are both medical goods 19. A cost is: A. Just the monetary value that is needed to produce a good B. The monetary cost of all the natural resources used to produce a good C. The value of everything a seller must give up to produce a good, including time.