Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Financial economics wikipedia , lookup

History of the Federal Reserve System wikipedia , lookup

Life settlement wikipedia , lookup

Financialization wikipedia , lookup

Money supply wikipedia , lookup

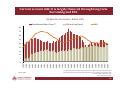

Interest rate ceiling wikipedia , lookup

Quantitative easing wikipedia , lookup

Global saving glut wikipedia , lookup

Interest rate wikipedia , lookup

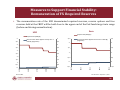

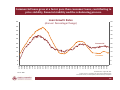

ExternalImpactofUSMonetaryPolicy onEmergingMarkets SeminarconvenedbytheEuropeanEconomicsandFinancial Centre(London) atPalaceofWestminster September09,2015 UncertaintiesFacedbytheGlobalEconomy Theglobaleconomycurrentlyfacesheighteneduncertainty intwoimportantareas: 1) growthprospectsofdifferentregionsandeconomies 2) paceofthenormalization ofglobalmonetarypolicies (1)ismoreimportantthan(2) 1) GrowthinmostEMEshassloweddown,withworseningprospects • forthosewithgreaterfinancialstabilityconcernsand • forthosefacingadverserelativepriceshocksfromthesubstantial declinesintheirexportedcommodityprices. 2 UncertaintiesFacedbytheGlobalEconomy 2) The strengtheninggrowthoutlookinAEsmaynot continuewithouttheexistingpolicysupport, includingMP. Theglobaleconomyalsosuffersfromariskof secularstagnation. MonetaryauthoritiesinAEshavebeencarefully calibratingpolicyactions • abalancebetweenpolicystimulusandfinancial excesses. 3 MonetaryPoliciesinAEs Withthese policychallengesinmindcentralbanksthat areexpectedtonormalizeearlierthanothershavesofar followedacautiouspolicystance. Inaddition,theabruptandexcessivemarketreactions experiencedduringthetaperingtantrumhaveforced centralbanks toclearlycommunicatetheirpolicy strategiesincludingthetimingandpaceoftheiractions. This,ofcourse,reflectsthefactthatchangesin the low interestrateandriskpremiaenvironmentwouldleadto greaterchangesinpricesandhencegreatermarket reactions. 4 Recent Global Economic andFinancial Market Developments Volatilityinglobalfinancialmarketsspikedin reaction tomarketdevelopmentsinChina particularlytothedevaluationof the Renminbi. Thisisessentiallydrivenbyuncertaintyonthe paceoftheslowdowninChinaanditsimpacton theglobaleconomy. Ofcourse,itmagnifiesuncertaintyassociatedwith themarketimpactofthepossibleFedratelift‐off decision. 5 MonetaryPoliciesinAEs Despiteheightenedvolatilityinmostfinancialmarkets, including stock,commoditiesandexchangerate markets,bondsmarketshave stayedrelativelycalmwithmuch lowerincreasesinliquidityandprice volatilityindices. Atthisconjuncture,inTurkeywehostedB20,G20ministerialand variousBISmeetings. Allofthesemeetingsservedasplatformsforsharingmarket experiences,economicoutlooksandrespectivepolicyresponses. Andofcourse,G20memberstateministersandgovernorsengaged in lengthydiscussionstoreachaconsensusviewofthe globaleconomic outlookandrespectivepolicyactionsbyeachmembercountry. 6 TheG20Communiqué "...willcontinuetomonitordevelopments,assessspillovers and addressemergingrisksasneededtofosterconfidenceandfinancial stability." "...willrefrainfromcompetitivedevaluations." "...willalsocarefullycalibrateandclearlycommunicate,especiallyour majormonetarypolicyactions,tominimisenegativespillovers, mitigateuncertaintyandpromotetransparency." "...butmonetarypolicyalonecannotleadtobalancedgrowth." "...pledgedtotakedecisiveactiontokeeptheeconomicrecoveryon trackandweareconfidenttheglobaleconomicrecoverywillgain speed." 7 PortfolioFlowstoEmergingMarkets CapitalFlowProxy Source: Bloomberg, CBRT Calculations (*) Emerging markets : Brazil, India, South Africa, Indonesia, Mexico, Poland, Hungary and Turkey Bloomberg Capital Inflow Index: 0.1*SPGSCI Index+0.3* MSCIEM Index+0.3*EMBI Index+0.3*FX CarryTrade Index 8 Investorshavebeendifferentiating among EMEs. Cumulative Equity and BondFlows in2015 (US$million) Source:EPFR Source: EPFR 9 PortfolioFlowstoTurkey Source: CBRT 10 NetInternationalIssuancesofEMCompanies Source: Sobrun and Turner (2015) 11 EMcurrencieshavedepreciatedsignificantly. Indollarsperunitoflocalcurrency. Source: Sobrun and Turner (2015) 12 RecentvolatilitylevelsofEMcurrenciesarestillbelowthelevels reachedduringtheEurozonesovereignbondcrisis. CurrencyVolatility(3MImpliedVolatility) Source: Bloomberg Emerging Economies: Turkey, South Africa, Brazil, Indonesia, Mexico, Russia, Colombia,, Poland, Czech Republic, Romania 13 EMsovereignandlocalcurrencybondyieldshavebeen relativelystable. EM10YearBondYields (3MRollingAverageofAbsoluteDailyChanges) Source: Bloomberg. (*) Emerging markets : Brazil, India, South Africa, Indonesia, Chile, Colombia, Mexico, Poland, Czech Republic, Romania and Turkey 14 InflationratesinEMEshavebeendiverging. InflationRatesin EMEs Source: Bloomberg 15 RealpolicyratesinEMEshavebeendiverging. RealPolicy(Effective)Ratesin EMEs Source: Bloomberg 16 FundamentalsandPoliciesRequiredDuring the Normalization ofGlobalMonetaryPolicies Sound growth outlook Stable inflation outlook Repairing imbalances Adequate external safety net Policy buffers A rich set of policy tools 17 FundamentalsandPoliciesRequiredDuring the Normalization ofGlobalMonetaryPolicies Sound growth outlook Stable inflation outlook Repairing imbalances Adequate external safety net Policy buffers A rich set of policy tools 18 GDPcontinuestogrowatamoderatepace. Contribution to Annual GDP Growth (Percentage Points) 20 Change in Inventories Net Exports Final Domestic Demand GDP 15 10 5 0 ‐5 Source: TURKSTAT 03/15 12/14 09/14 06/14 03/14 12/13 09/13 06/13 03/13 12/12 09/12 06/12 03/12 12/11 09/11 06/11 03/11 12/10 09/10 06/10 03/10 ‐10 Last Observation: 2015 Q1 19 FundamentalsandPoliciesRequiredDuring the Normalization ofGlobalMonetaryPolicies Sound growth outlook Stable inflation outlook Repairing imbalances Adequate external safety net Policy buffers A rich set of policy tools 20 Food andenergypricedevelopmentshelp disinflation intheshortrun… (Annual Percentage Change) 13 12 CPI H I 11 10 9 8 7 6 5 4 Source: TURKSTAT 08/15 06/15 04/15 02/15 12/14 10/14 08/14 06/14 04/14 02/14 12/13 10/13 08/13 06/13 04/13 02/13 12/12 10/12 08/12 06/12 04/12 02/12 12/11 10/11 08/11 3 Last Observation: August 2015. 21 …whileexchangeratemovementsdelaytheimprovementin thecoreindicators. Core Inflation Indicators H and I (Seasonally adjusted, Annualized 3‐Month‐Average, Percent) 16 H 14 I 12 10 8 6 4 2 Source: TURKSTAT, CBRT 08/15 05/15 02/15 11/14 08/14 05/14 02/14 11/13 08/13 05/13 02/13 11/12 08/12 05/12 02/12 11/11 08/11 05/11 02/11 0 Last Observation: August 2015. 22 The decline inimport prices limits the pass‐through from exchange rates to domestic inflation. Import Price Index (2010=100) 260 240 220 Import Prices (TL) 200 180 160 140 120 Import Prices (USD) 100 80 60 0110 Source: TURKSTAT, CBRT 0810 0311 1011 0512 1212 0713 0214 0914 0415 Last Observation: July 2015. 23 FundamentalsandPoliciesRequiredDuring the Normalization ofGlobalMonetaryPolicies Sound growth outlook Stable inflation outlook Repairing imbalances Adequate external safety net Policy buffers A rich set of policy tools 24 Thefavorableimpactofloweroilpricesonthecurrentaccount balancewillbemorepronouncedintheforthcomingperiod. Energy Imports (12‐Month Cumulative, Billion USD) 65 60 55 50 45 40 35 Source: TURKSTAT 0715 0415 0115 1014 0714 0414 0114 1013 0713 0413 0113 1012 0712 0412 0112 1011 0711 0411 0111 1010 0710 0410 0110 30 Last Observation: July 2015. 25 ExportstotheEUcontinuetogrowineuro terms. Exports to European Union (12 months cumulative, billion Euros) 60 55 50 45 40 35 Source: TURKSTAT 0715 0115 0714 0114 0713 0113 0712 0112 0711 0111 0710 0110 0709 0109 0708 0108 0707 0107 30 Last Observation: July 2015. 26 Recently exports showed some recovery inreal terms.. 135 130 125 120 115 110 105 100 export (excluding gold) 95 import (excluding gold) 90 1 2 3 2010 Source: CBRT 4 1 2 3 2011 4 1 2 3 2012 4 1 2 3 2013 4 1 2 3 2014 4 1 2 2015 Last Observation: 2015 Q2. 27 Currentaccountbalancehasimprovedmarkedlysince2011and furtherimprovementisexpectedinthe forthcoming period. Current Account Balance (CAB) (12‐Month Cumulative, Billion USD) ‐30 ‐35 CAD ‐40 CAD (Excluding gold) ‐45 ‐50 ‐55 ‐60 ‐65 ‐70 Source: CBRT 06/15 04/15 02/15 12/14 10/14 08/14 06/14 04/14 02/14 12/13 10/13 08/13 06/13 04/13 02/13 12/12 10/12 08/12 06/12 04/12 02/12 12/11 10/11 08/11 06/11 04/11 02/11 12/10 ‐80 10/10 ‐75 Last Observation: June 2015. 28 Currentaccountdeficitislargelyfinancedthroughlongterm borrowingandFDI. (12‐Months Cumulative, Billion USD) Portfolio and Short Term** FDI and Long Term* CAD 85 75 65 55 45 35 25 15 5 Source: CBRT 06/15 04/15 02/15 12/14 10/14 08/14 06/14 04/14 02/14 12/13 10/13 08/13 06/13 04/13 02/13 12/12 10/12 08/12 06/12 04/12 02/12 12/11 10/11 08/11 06/11 04/11 02/11 12/10 10/10 ‐5 *Long term inflows are sum of banking and real sectors’ long term net credit and bonds issued by banks and the Treasury. Short term capital movements are sum of banking and real sectors' short term net credit and deposits in banks. Last Observation: June 2015. 29 Halfofthe corporateforeigncurrency debt hasmore than three‐year maturity. Maturity Structure of External Liabilities of the Corporate Sector (Percent Share) 09.14 03.15 06.15 0‐1 Year 1‐2 Years 28,6 29,2 19,3 21,8 20,7 18,7 2‐3 Years 14,2 14,8 15,5 17,5 15,5 17,2 16,6 13,2 17,7 17,3 18,1 22,0 28,5 33,4 03.14 3‐5 Years 5 Years + Source: CBRT, External Debt Statistics of Non‐Financial Corporate Sector 30 Loanvolumescontinuetoexpandatareasonablepacedueto cautiousmonetarypolicystanceandmacroprudentialmeasures. Total Loan Growth Rate (Year on Year Change, Percent) 40 35 30 25 20 15 Source: CBRT 07/15 05/15 03/15 01/15 11/14 09/14 07/14 05/14 03/14 01/14 11/13 09/13 07/13 05/13 03/13 01/13 11/12 09/12 07/12 05/12 03/12 01/12 11/11 09/11 07/11 05/11 03/11 01/11 10 Last Observation: August 28, 2015. Total loan is inclusive of all types of banks (deposit banks, participation banks, and development/investment banks) and credit cards. Adjusted for exchange rate. 31 Measures to Support Financial Stability: SupportingTurkishLiraCoreLiabilities The remuneration rate of Turkish lira required reserves may be revised to reduce the intermediation cost of banking sector and to support core liabilities. Credit/Deposit Ratio (Percent) 130 130 120 120 110 110 100 100 90 90 Announcement of Required Reserve Measures in Financial Stability Report 80 80 70 Source: BRSA 0914 1114 0115 0315 0515 0715 0913 1113 0114 0314 0514 0714 0912 1112 0113 0313 0513 0713 0911 1111 0112 0312 0512 0712 0910 1110 0111 0311 0511 0711 0110 0310 0510 0710 70 Last Observation: August 07, 2015. 32 NPLratiosforFXcorporateloanshavebeendeclining. NPL Ratios For Corporate Loans (Percent) 5,0 Total Corporate TL FX 4,5 4,0 3,5 3,1 3,0 2,5 2,1 2,0 1,5 1,0 0,9 0313 0413 0513 0613 0713 0813 0913 1013 1113 1213 0114 0214 0314 0414 0514 0614 0714 0814 0914 1014 1114 1214 0115 0215 0315 0415 0515 0615 0,5 Source: CBRT Financial Stability Report, No:20 Last Observation: June 2015. 33 FundamentalsandPoliciesRequiredDuring the Normalization ofGlobalMonetaryPolicies Sound growth outlook Stable inflation outlook Repairing imbalances Adequate external safety net Policy buffers A rich set of policy tools 34 ReserveRequirementPolicies FX liquidity will be released via reserve requirement policies (before and during normalization). CBRT Reserves (Billion USD ) FX for FX RR 140 CBRT Other FX Reserve ROM FX CBRT Other Gold Reserves Gold for Precious Metal ROM Gold 120 100 80 60 40 20 Source: CBRT 07/15 05/15 03/15 01/15 12/14 10/14 08/14 06/14 04/14 02/14 12/13 10/13 08/13 06/13 05/13 03/13 01/13 11/12 09/12 07/12 05/12 03/12 01/12 11/11 0 09/11 Last Observation: July 31, 2015. 35 Measures to Support Financial Stability: LengtheningtheMaturityofNoncoreFXLiabilities FX required reserve ratios for newly originated FX noncore liabilities of the banks will be adjusted to encourage further maturity extension (before and during). Maturity Breakdown of Non‐Core FX Liabilities (Percent) 60 Required Reserve Measures 55 Up to 1-Year 50 45 40 Longer than 3-Years 35 Source: CBRT 07/15 06/15 05/15 04/15 03/15 02/15 01/15 12/14 11/14 10/14 09/14 08/14 07/14 06/14 05/14 04/14 03/14 02/14 30 01/14 Last Observation: July 31, 2015. 36 FXLiquidity Measures:ForeignExchangeDepositMarket Borrowing limits on foreign exchange deposit accounts will be increased (before normalization). After the planned change, the size of the FX liquidity that the financial system can access from CBRT, which is the sum of FX holdings in ROM and limits of the foreign exchange deposit market, will be considerably above the external debt payments of the banks in the coming year. 37 Measures to Support Financial Stability: RemunerationofFXRequiredReserves The remuneration rate of the USD denominated required reserves, reserve options and free reserves held at the CBRT will be held close to the upper end of the Fed funds target rate range (before and during normalization). Euro USD Deposit Rate (EUR) (%) Deposit Rate (USD) (%) 5 5 Remuneration Rates Applied To Req. Res. in USD (%) (Right Axis ) 4,5 4,5 4 2,5 2,5 Commission Rates Applied to Accounts in EUR (%) (Right Axis) 2 2 4 3,5 3,5 3 1,5 1,5 3 2,5 2,5 2 2 1,5 1 1 0,5 0,5 1,5 1 1 0 0 0,5 Source: CBRT ‐0,5 0915 0815 0715 ‐0,5 0615 0915 0815 0715 0 0615 0 0515 0,5 0515 Last Observation: September 7, 2015. 38 FundamentalsandPoliciesRequiredDuring the Normalization ofGlobalMonetaryPolicies Sound growth outlook Stable inflation outlook Repairing imbalances Adequate external safety net Policy buffers A rich set of policy tools 39 PolicyBuffers Amplefiscalpolicyspace: • verylowbudgetdeficit, aswellasprimarysurplus • lowpublicdebttoGDPratio Amplemonetarypolicyspace Amplemacroprudential policy space 40 FundamentalsandPoliciesRequiredDuring the Normalization ofGlobalMonetaryPolicies Sound growth outlook Stable inflation outlook Repairing imbalances Adequate external safety net Policy buffers A rich set of policy tools 41 TheRoadMapDuringtheNormalization ofGlobalMonetaryPolicies Liquidity Management Simplification •More narrow,more symmetric interest rate corridor •Restriction onfunding to primary dealers •More simplified collateral conditions FXLiquidity Measures •Flexible FXselling auctions •Adjustments inrequired reserve and Reserve Options Mechanism conditions •Measures onFXdeposit market Measures to Support Financial Stability •Lengthening the maturity ofnoncore FX liabilities •Supporting core liabilities inTurkish Lira •Remuneration ofFXrequired reserves 42 TheRoadMapDuring theNormalization ofGlobalMonetaryPolicies Policy Measure Timing Interest RateCorridor During Normalization Funding Before Normalization CollateralConditions BeforeandDuringNormalization FlexibleFXSellingAuctions BeforeNormalization ReserveOptions Before and During Normalization MeasuresonFXDepositMarket Before Normalization LengtheningtheMaturityofNoncoreFX Liabilities BeforeNormalization SupportingTLCoreLiabilities Before and During Normalization RemunerationofFXRequiredReserves Before and During Normalization 43 The liquidity policy hasbeen tight and will befurther tightened aslong asdeemed necessary. Interest Rates (Percent) 13 Interest Rate Corridor CBRT Average Fund Rate BIST Interbank Market O/N Rates One‐Week Repo Rate 13 Source: CBRT 09/15 08/15 07/15 06/15 05/15 04/15 02/15 03/15 01/15 3 12/14 3 11/14 4 10/14 4 09/14 5 08/14 5 07/14 6 06/14 6 05/14 7 04/14 7 02/14 03/14 8 01/14 8 12/13 9 11/13 9 10/13 10 09/13 10 08/13 11 07/13 11 06/13 12 05/13 12 Last Observation: September 7, 2015. 44 Yieldcurvehasbeen invertedduetotightliquiditypolicy. Interest Rates (Percent) 5‐Year Market Rate 12 3‐Month Market Rate 12 10 10 8 8 6 6 4 4 5 year‐3 month spread Source: CBRT 08/15 06/15 04/15 02/15 12/14 10/14 08/14 06/14 04/14 02/14 12/13 10/13 08/13 06/13 04/13 02/13 12/12 10/12 08/12 06/12 04/12 02/12 ‐2 12/11 ‐2 10/11 0 08/11 0 06/11 2 04/11 2 Last Observation: September 7, 2015. 45 Commercialloansgrowatafasterpacethanconsumerloans,contributingto pricestability,financialstabilityandtherebalancingprocess. Loan Growth Rates 50 50 (Annual Percentage Change) 45 45 40 40 35 35 30 30 Commercial 25 25 20 20 15 15 Consumer 10 10 Source: CBRT 0715 0515 0315 0115 1114 0914 0714 0514 0314 0114 1113 0913 0713 0513 0313 0113 1112 0912 0712 0512 0312 0112 1111 0911 0711 0511 0311 0111 1110 0910 0710 0 0510 0 0310 5 0110 5 Last Observation: August 28, 2015. Inclusive of loans extended by all types of banks (deposit banks, Participation banks, and development/investment banks). FX adjusted. 46 FXLiquidity Measures:Flexible FXSale Auctions Flexibility of FX sale auctions is increased to contain exchange rate volatility. FX Sale Auctions (Million USD ) 120 1200 Monthy Quantity of FX Sales* (Right Axis) Daily FX Sales 100 1000 80 800 60 600 40 400 20 200 0 Source: CBRT 09/15 08/15 07/15 06/15 05/15 04/15 03/15 02/15 01/15 12/14 11/14 10/14 09/14 08/14 07/14 0 06/14 *The value for September is as of September 7, 2015. Last Observation: September 7, 2015. 47 Thankyou! SeminarconvenedbytheEuropeanEconomicsandFinancial Centre(London) atPalaceofWestminster September09,2015