Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

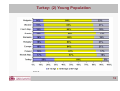

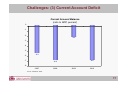

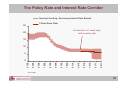

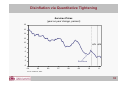

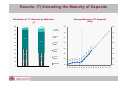

CENTRAL BANK OF THE REPUBLIC OF TURKEY The Challenges of Balancing Hot Money Inflows vs Conducting a Prudent Monetary Policy Dr. Đbrahim Turhan Deputy Governor 5 May 2011 1 Presentation Outline I. Monetary Policy in Advanced Economies vs Emerging Economies II. The Turkish Economy III. Monetary Policy Response:Turkey’s Experience IV. Financial Stability Outcomes So Far 2 I. Monetary Policy in Advanced Economies vs Emerging Economies 3 Growth Differentials Growth Rates (annual change) 10 8 6 4 2 0 -2 Advanced Countries -4 Emerging Countries -6 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Source: Bloomberg, CBRT 4 Inflation Differentials Core Inflation (annual change) 5 Advanced Countries 4 Emerging Countries 3 2 1 Jan-11 Oct-10 Jul-10 Apr-10 Jan-10 Oct-09 Jul-09 Apr-09 Jan-09 Oct-08 Jul-08 Apr-08 Jan-08 Oct-07 Jul-07 Apr-07 Jan-07 0 Source: Bloomberg, CBRT 5 Interest Rate Differentials Policy Rates (percent) 12 10 Advanced Countries Emerging Countries 8 6 4 2 Apr-11 Jan-11 Oct-10 Jul-10 Apr-10 Jan-10 Oct-09 Jul-09 Apr-09 Jan-09 Oct-08 Jul-08 Apr-08 Jan-08 Oct-07 Jul-07 Apr-07 Jan-07 0 Source: Central Banks, CBRT 6 Quantitative Easing Balance Sheets of Major Central Banks 350 300 250 200 150 100 BoE 50 Jan-07 Jul-07 Jan-08 ECB Jul-08 Jan-09 Jul-09 Fed Jan-10 Jul-10 Jan-11 * Index: March 2007=100 Source: Central Banks 7 Result: Surge in Capital Flows After the crisis both the magnitude and the composition of capital flows have changed: magnitude due to exceptionally looose monetary policies and QE in advanced economies; composition – due to risk averseness Net Capital Flow to Emerging Countries 1,400 1,200 Other Investments Net Portfolio Investments Net Direct Inflows Net Private Inflows 1,000 800 600 400 200 0 -200 2007 2008 2009 2010* 2011** 2012** * Estimate ** Forecast 8 Result: Appreciation Pressure USD against EM currencies * (4 Jan 2010=1) 1.15 Announcement of QE2 by the FED 1.10 1.05 Depreciation 1.00 Appreciation 0.95 0.90 01-10 03-10 05-10 07-10 09-10 11-10 01-11 03-11 * Average of emerging market currencies including Brazil, Chile, Colombia, Czech Republic, Indonesia, Hungary, Mexico, Poland, Republic of Korea and South Africa. Source: Bloomberg, CBRT 9 II. The Turkish Economy 10 Turkey: (1) Commodity Importer Impact of Energy Prices 60 50 40 35.5 30 25.2 20.9 17.6 17 20 10.5 10 0 1.6 4.4 9.1 9.9 10 10.7 11.8 12.9 12.7 12.3 13.2 2002 2003 2004 2005 2006 2007 2008 2009 2010 0 Real Energy Imports with 2002 Prices Price Effect Total of Energy Imports Source: Treasury 11 Turkey: (2) Young Population Source: UN 12 Turkey: (3) Low Savings Rate Gross national savings (Percent of GDP, 2009) 60 50 40 30 20 10 0 China India Indonesia Korea Brazil Turkey Source: IMF WEO 13 Turkey: (4) Convergence to the EU GDP (2009 PPP based, current international dolar) 3.0 2.5 2.0 1.5 1.0 Austria Greece Sweden Belgium Netherlands Poland Turkey Spain Italy France United Kingdom Germany 0.0 Switzerland 0.5 Source: IMF WEO 14 Challenges: (1) Surge in Capital Flows Composition of Capital Flows (12-month rolling sum, billion USD) Finance of Current Account Deficit (percentage of CAD) 120 50 Portfolio Investments+ Deposits 40 Short Term Credit + Portfolio Investments + Deposits 100 80 FDI 30 60 40 20 20 10 0 0 -20 FDI -40 -10 Private Sector Credit* -20 -30 01-07 01-08 01-09 * After controlling for the effect of change in Decree No. 32 Source: TURKSTAT, CBRT 01-10 -60 -80 -100 01-06 01-07 01-08 01-09 01-10 Source: TURKSTAT, CBRT 15 Challenges: (2) Rapid Credit Growth Credit Use and Current Account Deficit 9 8 14 Current Account Deficit/GDP* 12 7 10 6 5 8 4 6 3 ∆ in Credit Stock/GDP (right axis)** 4 2 2 1 0 1203 0304 0604 0904 1204 0305 0605 0905 1205 0306 0606 0906 1206 0307 0607 0907 1207 0308 0608 0908 1208 0309 0609 0909 1209 0310 0610 0910 1210 0 *12-months cumulative current account deficit / GDP ** Rate of annual change in credit stock / GDP Source: BRSA, CBRT. 16 Challenges: (3) Current Account Deficit Current Account Balance (ratio to GDP, percent) 0 -1 -2 -2.2 -3 -4 -5 -6 -5.3 -7 -6.6 -6.8 -8 2007 2008 2009 2010 Source: TURKSTAT, CBRT 17 Challenges: (4) Weakness in External Demand Domestic Demand and Exports (2008 Q1=100) Turkey’s External Demand Index* (June 2008=100) 112 110 Global Economic Activity Index Domestic Demand 105 108 100 104 95 90 100 85 Turkey’s External Demand Index 96 92 2006 Goods and Services Exports 80 75 2007 2008 2009 2010 2011 2012 * The shares of countries within the exports of Turkey and weighted GDP data are employed in the calculation of the external demand index of Turkey. Source: Bloomberg, Consensus Forecasts, IMF WEO, TURKSTAT, CBRT 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 2005 2006 2007 2008 2009 2010 Source: TURKSTAT, CBRT 18 Challenges: (5) Output Gap Capacity Utilization Rate Non-Farm Unemployment Rate (seasonally adjusted) 85 (seasonally adjusted, percent) 22 20 80 18 75 16 70 14 65 12 Source: CBRT. 0111 1010 0710 0410 0110 1009 0709 0409 0109 1008 0708 0408 0108 10 1007 0411 0111 1010 0710 0410 0110 1009 0709 0409 0109 1008 0708 0408 0108 1007 0707 0407 0107 60 Source: TURKSTAT, CBRT. 19 III. Monetary Policy Reponse: Turkey’s Experience 20 Monetary Policy Since 2003 Accelerating Inflation Price Stability TARGET 2003-2005 Favorable Supply Shock Decelerating Inflation Policy Rate Macroprudential Instruments Decelerating Credit Growth Financial Stability Accelerating Credit Growth 21 Monetary Policy Since 2003 2006 Q2 Adverse Supply Shock and High Demand Shock Accelerating Inflation Policy Rate Macroprudential Instruments Price Stability TARGET Decelerating Inflation Decelerating Credit Growth Financial Stability Accelerating Credit Growth 22 Monetary Policy Since 2003 2008 Q1 Accelerating Inflation Adverse Supply Shock Policy Rate Macroprudential Instruments Price Stability TARGET Decelerating Inflation Decelerating Credit Growth Financial Stability Accelerating Credit Growth 23 Monetary Policy Since 2003 Accelerating Inflation Price Stability TARGET 2008 Q3-2010 Q4 Decelerating Inflation Global Financial Crisis Policy Rate Macroprudential Instruments Decelerating Credit Growth Financial Stability Accelerating Credit Growth 24 Monetary Policy Since 2003 Accelerating Inflation Price Stability TARGET 2011 Q1Current Conjuncture Decelerating Inflation Policy Rate Macroprudential Instruments Decelerating Credit Growth Financial Stability Accelerating Credit Growth 25 Quantitative Easing vs. Quantitative Tightening • Quantitative easing in major economies has continued in response to weakness in economic activity and heightened sovereign risks, resulting in unprecedented increases in central banks’ balance sheets. • Facing a significant degree of capital inflows, some emerging economies have resorted to quantitative macroprudential tightening, even capital flow measures. • Turkey has also initiated quantitative tightening via its exit strategy in April-November 2010 (QT1) and reserve requirement hikes after November 2010 (QT2). 26 Two Different Approaches • Approach 1: Use capital flow measures to restrict inflows while tightening via interest rates (Brazil, Republic of Korea) • Approach 2: Use macroprudential measures to restrict domestic credit and domestic demand while keeping the short term interest rate differentials as low as possible (Turkey) 27 Macroprudential Measures Measures against capital flows Supervision/ Inspection Measures against exchange risk exposure Measures against liquidity management and credit supply Measures against excessive rise in asset prices 0 5 10 15 20 25 Number of countries 28 The New Policy Mix: Turkey A lower policy rate, higher reserve requirement ratios and a wider interest rate corridor • The framework we adopt is not significantly different from the conventional inflation targeting framework. • The only difference is that, previously our policy instrument was the oneweek repo rate, but currently our instrument is a “policy mix” • We seek to use these instruments in the right combination in order to cope with both inflation and macro-financial risks. • The monetary policy stance in this framework is determined not by policy rates alone, but as a combination of all the policy instruments. 29 The Policy Rate and Interest Rate Corridor Overnight Lending - Borrowing Interest Rate Spread 1 Week Repo Rate 25 Introduction of 1 week repo rate as policy rate 20 15 10 5 0411 0111 1010 0710 0410 0110 1009 0709 0409 0109 1008 0708 0408 0108 0 Source: CBRT 30 Reserve Requirements as a Macroprudential Tool Reserve Requirement Ratios (percent) 18 Longer Than 1 Year 16 6-12 Months 14 3-6 Months 12 1-3 Months 10 Up to 1 Month 8 Demand Deposit 6 4 2 0 Nov-10 Step 1 Step 2 Step 3 Step 4 Dec-10 Jan-11 Mar-11 Apr-11 Source: CBRT 31 Reserve Requirements as a Macroprudential Tool Reserve Requirement Ratios (percent) 25 20.5 20.0 20 15 13.5 11.8 10.0 10 8.0 4.0 3.5 Poland 5 Russia 6.0 India Indonesia Peru Turkey (FX)* Turkey (TRY)* Brazil China 0 * Weighted averages Source: Central Banks, CBRT 32 Disinflation via Quantitative Tightening Services Prices (year-on-year change, percent) 18 16 14 12 10 QT1 QT2 8 6 4 2 Services 0 04 05 06 07 08 09 10 11 Source: TURKSTAT, CBRT 33 Goods Prices Goods and Services Prices (year-on-year change, percent) 18 16 Goods 14 12 10 8 6 4 Services 2 0 04 05 06 07 08 09 10 11 Source: TURKSTAT, CBRT 34 Comparison of Inflation Rates Inflation Rates in Turkey and around the Globe (March 2011, percent) 10 9 8 7 6 5 4 3 2 1 Russia Indonesia Brazil China Rep.of Korea Greece Hungary Poland S. Africa UK Turkey Canada Mexico USA Euro Area Germany France Czech R. 0 Source: Bloomberg, CBRT 35 Price Stability Inflation and Output Gap Forecasts Source: CBRT 36 Financial Stability: Objectives 1. Debt Ratios: Use of more equity, more prudent borrowing 2. Debt Maturities: Extending maturities of domestic and foreign borrowing and deposits 3. FX Positions: Strengthening FX positions of public and private sectors 4. Risk management: More effective management of all types of risks by all agents in the economy 37 Macroprudential Tools • It may not always be possible to attain price stability and financial stability together, by means of policy rates alone. • Solution: Use macroprudential tools in coordination with other public authorities. • Macroprudential tools: 1. Reserve requirements 2. Liquidity management 3. Capital adequacy ratios 4. Liquidity adequacy ratios 5. Taxes 6. Primary expenditures of government 38 Measures Taken by Other Authorities 1. Fiscal discipline 2. Ban on FX loans to households 3. Domestic currency bond market 4. Loan/value restrictions 5. Tax hikes on certain consumer loans 6. Restrictions on credit card borrowing 39 IV. Financial Stability Outcomes So Far 40 Results: (1) Tightening the Liquidity Reserve Requirements Balances (billion TRY) 70 The new reserve requirements is effective as of Apr 15, 2011 (approx. 19.1 billion TRY) 60 50 40 TRY required reserves 30 20 10 FX Required Reserves 0 01-09 04-09 07-09 10-09 01-10 04-10 07-10 10-10 01-11 04-11 Source: CBRT 41 Results: (2) Funding More Dependent on CB Central Bank Liquidity (billion TRY) Weekly Repo Funding Sterilization through ON Borrowing 3-month Repo Funding Net Liquidity Provided 40 30 QT1 QT2 20 10 0 -10 -20 01-09 04-09 07-09 10-09 01-10 04-10 07-10 10-10 01-11 04-11 Source: ISE, CBRT 42 Results: (3) Volatility in Overnight Rates Overnight Interest Rates (percent) Volatility in Overnight Interest Rates (2-week standard deviation) 1.8 11 10 1.6 CBRT Lending Rate 9 1.4 Policy Rate 8 1.2 7 1.0 6 0.8 5 Overnight Interest Rate 4 0.6 0.4 3 CBRT Borrowing Rate 2 1 08-10 09-10 10-10 Source: ISE, CBRT 11-10 12-10 01-11 02-11 03-11 04-11 0.2 0.0 09-10 10-10 11-10 12-10 01-11 02-11 03-11 04-11 Source: ISE, CBRT 43 Results: (4) Tightening of Monetary Conditions Yield Curve* (percent) Inflation Expectations* (percent) 10 9.5 Apr 6, 2011 9.0 9 12-month forward 8.5 8 8.0 7 7.5 6 Oct. 1, 2010 7.0 24-month forward 5 6.5 0.5 1.0 1.5 2.0 2.5 3.0 3.5 * Calculated from the compounded returns on bonds quoted in ISE Bills and Bonds Market by using ENS method. Source: ISE, CBRT 4.0 4 12-07 06-08 12-08 06-09 12-09 06-10 12-10 * CBRT Expectations Survey results from the second survey period. Source: ISE, CBRT 44 Results: (5) Creating Wedge between Interest Rates Interest Rates on Saving Deposits* Interest Rates on Loans* 12.5 9.5 12.0 11.60 9.0 11.5 11.0 8.5 10.5 10.53 8.0 10.0 9.5 7.5 9.12 9.0 7.0 Up to 1 month Up to 6 months Up to 3 months Up to 1 year 04.11 03.11 02.11 12.10 11.10 10.10 09.10 08.10 8.0 07.10 04.11 03.11 02.11 01.11 12.10 11.10 10.10 09.10 08.10 07.10 6.5 01.11 8.36 8.5 Commercial Loan Consumer Loan (Other Consumer+Vehicle+Housing) 45 Results: (6) Alleaviating the Pressure on Currency USD against EM Currencies and TRY* (4 Jan 2010=1) 1.15 Announcement of QE2 by the FED TRY 1.10 Depreciation 1.05 1.00 Appreciation 0.95 EM Average 0.90 01-10 03-10 05-10 07-10 09-10 11-10 01-11 03-11 * Average of emerging market currencies including Brazil, Chile, Colombia, Czech Republic, Indonesia, Hungary, Mexico, Poland, Republic of Korea and South Africa. Source: Bloomberg, CBRT 46 Results: (7) Extending the Maturity of Deposits Breakdown of TL Deposits by Maturities Average Maturity of TL Deposits (Day) (%) 100 1.1 4.0 0.7 90 2.1 1.3 7.3 80 80 75 75 70 70 65 65 1 Year and more 80 58.3 50 52.6 55 50.2 48.2 47.0 47.5 46.9 46.9 60 50 12.11 11.11 10.11 09.11 03.11 02.11 01.11 45 12.10 15.04.11 45 11.10 26.11.10 Sight dep. 10.10 0 09.10 15.1 08.10 14.4 50 07.10 10 Up to 1 Month 45.6 18.4 20 46.0 55 28.8 06.10 30 Up to 3 Month 54.7 60 40 08.11 Up to 6 Month 07.11 55.9 60 06.11 51.0 05.11 Up to 1 Year 04.11 70 Results: (8) Containing the Acceleration in Credit Growth Loans* and Deposits** to GDP (%) Annual Change in Credit Volume (%) 14 50 12 40 10 30 8 6 20 4 10 2 0 0 2011 2010 Change in Loans -10 12.06 03.07 06.07 09.07 12.07 03.08 06.08 09.08 12.08 03.09 06.09 09.09 12.09 03.10 06.10 09.10 12.10 03.11 04.11 Change in Deposits 2009 2008 2007 -2 Corporate Retail 48 CENTRAL BANK OF THE REPUBLIC OF TURKEY The Challenges of Balancing Hot Money Inflows vs Conducting a Prudent Monetary Policy Dr. Đbrahim Turhan Deputy Governor May 2011 49