Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

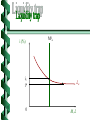

The liquidity preference theory was an attempt to displace the prevailing theory of interest (and financial asset pricing)--the loanable funds theory (also known as the “classical” or “time preference” theories) of interest. A successful assault on loanable funds was essential to the success of Keynes’s new theory of unemployment, since the old theory ostensibly preserves the validity of Say’s Law when a monetary economy is under consideration. Key elements Humans are “present-oriented” and hence must be compensated for deferring gratification. Interest earned on bonds is the “reward for waiting”--that is, the monetary compensation required to induce present-oriented individuals to abstain from consumption (to save). The willingness to wait (saving) is a positive function of the yield of bonds (or other financial assets). Don’t tell me you didn’t know that bond prices and yields move inversely! S is saving I is investment i is the interest rate (yield of bonds) S = f(i) [1] S/i > 0 [1a] I = (i) [2] I/i < 0 [2a]a S=I [3]b a Explained by the diminishing marginal product of capital b Equilibrium condition in the loanable funds market i (%) i2 S1 S2 1 i1 0 An improvement of thrift stimulates I--which explains the preference of some economists for measures (e.g., reduced taxes on capital gains) that ostensibly stimulate saving. 2 I1 I2 I S, I I I •Leakages are defined as income received by households but not spent for the purchase of new goods and services in domestic goods. •Injections are expenditures in domestic markets made by units other than domestic households. National Income S In a mature, industrialized economy the existing stock of debt held by individuals and institutions is vast. The flow of new debt issues in any brief time interval is but a tiny fraction of stock of debt outstanding. Taking into account the development of organized secondary markets, previously issued bonds are a nearperfect substitute for newly-issued bonds (from the wealth-holders point of view). The primary determinant of the yield of new issues is therefore the yield prevailing in the secondary market for similar types of securities. Definitions L The liquidity preference function; Lt The transactions demand for liquid balances; La The asset or speculative demand for liquid balances; i The yield of bonds; PB The price of bonds; M0 The (exogenously-determined) nominal money stock.; M0t Money held for transactions purposes; M0a Money held for asset purposes; Y Real gross domestic product. That the FED can control rr is not subject to dispute. If the more controversial proposition holds--that is, the FED can target Ra (highpowered money)--then it follows that the FED can target Dd. Which is to say, money is exogenous Let: •Dd deposit liabilities of the banking system •Ra total reserves of the banking system •rr legal reserve ratio If banks are “fully loaned up,” then: rr = Ra/Dd It follows from [1] that: Dd = Ra/rr [1] The model L = Lt + La (1) Lt =f(Y) (2) Lt’(Y) > 0 (2.1) La = f (i) (3) La’(i) < 0 (3.1) M 0= M 0t + M 0a L = M0 (4) (5) i (%) M0a i1 i* 0 0 La M, L i (%) M0a Bond yields fall, and bond prices rise i2 i1 0 0 La M, L i (%) M0a Bond yields rise, and bond prices fall i2 i1 0 0 La M, L