Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Chapter 12

Analytical Issues in

Disinflation Programs

© Pierre-Richard Agénor and Peter J. Montiel

1

Topics in Exchange-Rate-Based Programs.

The Role of Credibility in Disinflation Programs.

Disinflation and Nominal Anchors.

2

Topics in Exchange-RateBased Programs

Although use of the exchange rate as a key nominal

anchor brought hyperinflation to a halt with small output

cost, success has been limited in chronic-inflation

countries.

The Southern Cone tablita experiments of the late 1970s:

slow reduction in the inflation rate;

appreciation of real exchange rate.

Such programs have been accompanied by an initial

expansion in economic activity, followed by a significant

contraction.

Example: Morocco.

Boom-recession cycle has been observed in both

successful and unsuccessful stabilization attempts.

4

Figures 12.1 and 12.2: behavior of real interest rates in

exchange-rate-based stabilization programs.

Real interest rates

declined at the inception of the program in the

Southern Cone tablita experiments of the late 1970s;

rose sharply in the heterodox programs of the 1980s

implemented in Argentina, Brazil, Israel, and Mexico.

Key aspect of some of the models: effect of varying

expectations about present and future government

policies.

5

F

i

g

u

r

e

1

2

.

1

a

R

e

a

l

I

n

t

e

r

e

s

t

R

a

t

e

s

i

n

t

h

e

T

a

b

l

i

t

a

E

x

p

e

r

i

m

e

n

t

s

(

R

e

a

l

l

e

n

d

i

n

g

r

a

t

e

s

,

i

n

p

e

r

c

e

n

t

p

e

r

y

e

a

r

)

8

0

A

r

g

e

n

t

i

n

a

6

0

4

0

2

0

0

2

0

4

0

6

0

7

8

q

1

7

9

q

1

8

0

q

1

8

1

q

1

8

2

q

1

S

o

u

r

c

e

:

V

é

g

h

(

1

9

9

2

)

.

N

o

t

e

s

:

R

e

a

l

i

n

t

e

r

e

s

t

r

a

t

e

s

a

r

e

c

a

l

c

u

l

a

t

e

d

b

y

s

u

b

t

r

a

c

t

i

n

g

t

h

e

o

n

e

q

u

a

r

t

e

r

a

h

e

a

d

i

n

f

l

a

t

i

o

n

r

a

t

e

f

r

o

m

t

h

e

n

o

m

i

n

a

l

l

e

n

d

i

n

g

r

a

t

e

.

S

h

a

d

e

d

a

r

e

a

s

i

n

d

i

c

a

t

e

p

e

r

i

o

d

s

d

u

r

i

n

g

w

h

i

c

h

t

h

e

p

r

o

g

r

a

m

s

w

e

r

e

i

n

p

l

a

c

e

.

6

F

i

g

u

r

e

1

2

.

1

b

R

e

a

l

I

n

t

e

r

e

s

t

R

a

t

e

s

i

n

t

h

e

T

a

b

l

i

t

a

E

x

p

e

r

i

m

e

n

t

s

(

R

e

a

l

l

e

n

d

i

n

g

r

a

t

e

s

,

i

n

p

e

r

c

e

n

t

p

e

r

y

e

a

r

)

1

2

0

C

h

i

l

e

1

0

0

8

0

6

0

4

0

2

0

0

7

7

q

1

7

8

q

1

7

9

q

1

8

0

q

1

8

1

q

1

8

2

q

1

8

3

q

1

S

o

u

r

c

e

:

V

é

g

h

(

1

9

9

2

)

.

N

o

t

e

s

:

R

e

a

l

i

n

t

e

r

e

s

t

r

a

t

e

s

a

r

e

c

a

l

c

u

l

a

t

e

d

b

y

s

u

b

t

r

a

c

t

i

n

g

t

h

e

o

n

e

q

u

a

r

t

e

r

a

h

e

a

d

i

n

f

l

a

t

i

o

n

r

a

t

e

f

r

o

m

t

h

e

n

o

m

i

n

a

l

l

e

n

d

i

n

g

r

a

t

e

.

S

h

a

d

e

d

a

r

e

a

s

i

n

d

i

c

a

t

e

p

e

r

i

o

d

s

d

u

r

i

n

g

w

h

i

c

h

t

h

e

p

r

o

g

r

a

m

s

w

e

r

e

i

n

p

l

a

c

e

.

7

F

i

g

u

r

e

1

2

.

1

c

R

e

a

l

I

n

t

e

r

e

s

t

R

a

t

e

s

i

n

t

h

e

T

a

b

l

i

t

a

E

x

p

e

r

i

m

e

n

t

s

(

R

e

a

l

l

e

n

d

i

n

g

r

a

t

e

s

,

i

n

p

e

r

c

e

n

t

p

e

r

y

e

a

r

)

6

0

Ur u

g u

a

y

4

0

2

0

0

-2

0

-4

0

7

8

q

7

1

9

q

8

1

0

q

8

1

1

q

8

1

2

q

8

1

3

q

1

S

o

u

r

c

e

:

V

é

g

h

(

1

9

9

2

)

.

N

o

t

e

s

:

R

e

a

l

i

n

t

e

r

e

s

t

r

a

t

e

s

a

r

e

c

a

l

c

u

l

a

t

e

d

b

y

s

u

b

t

r

a

c

t

i

n

g

t

h

e

o

n

e

q

u

a

r

t

e

r

a

h

e

a

d

i

n

f

l

a

t

i

o

n

r

a

t

e

f

r

o

m

t

h

e

n

o

m

i

n

a

l

l

e

n

d

i

n

g

r

a

t

e

.

S

h

a

d

e

d

a

r

e

a

s

i

n

d

i

c

a

t

e

p

e

r

i

o

d

s

d

u

r

i

n

g

w

h

i

c

h

t

h

e

p

r

o

g

r

a

m

s

w

e

r

e

i

n

p

l

a

c

e

.

8

F

i

g

u

r

e

1

2

.

2

a

R

e

a

l

I

n

t

e

r

e

s

t

R

a

t

e

s

i

n

H

e

t

e

r

o

d

o

x

E

x

p

e

r

i

m

e

n

t

s

(

R

e

a

l

l

e

n

d

i

n

g

r

a

t

e

s

,

i

n

p

e

r

c

e

n

t

p

e

r

y

e

a

r

)

900

700

250

A

200

150

500

300

100

50

0

100

0

-5 0

-1 0 0

-1 0 0

8

8

4

8

5

q

8

6

q

8

1

7

q

1

8

q

8

1

q

8

1

4

1

8

5

q

8

6

q

1

7

q

1

S

o

u

r

c

e

:

V

é

g

h

(

1

9

9

2

)

.

N

o

t

e

s

:

R

e

a

l

i

n

t

e

r

e

s

t

r

a

t

e

s

a

r

e

c

a

l

c

u

l

a

t

e

d

b

y

s

u

b

t

r

a

c

t

i

n

g

t

h

e

o

n

e

q

u

a

r

t

e

r

a

h

e

a

d

i

n

f

l

a

t

i

o

n

r

a

t

e

f

r

o

m

t

h

e

n

o

m

i

n

a

l

l

e

n

d

i

n

g

r

a

t

e

.

S

h

a

d

e

d

a

r

e

a

s

i

n

d

i

c

a

t

e

p

e

r

i

o

d

s

d

u

r

i

n

g

w

h

i

c

h

t

h

e

p

r

o

g

r

a

m

s

w

e

r

e

i

n

p

l

a

c

e

.

9

F

i

g

u

r

e

1

2

.

2

b

R

e

a

l

I

n

t

e

r

e

s

t

R

a

t

e

s

i

n

H

e

t

e

r

o

d

o

x

E

x

p

e

r

i

m

e

n

t

s

(

R

e

a

l

l

e

n

d

i

n

g

r

a

t

e

s

,

i

n

p

e

r

c

e

n

t

p

e

r

y

e

a

r

)

500

60

400

40

I

sr

20

300

0

200

- 20

100

- 40

0

- 60

84q1

85q1

86q1

87q1

88q1

89q1

87q1

88q1

89q1

90q

91

S

o

u

r

c

e

:

V

é

g

h

(

1

9

9

2

)

.

N

o

t

e

s

:

R

e

a

l

i

n

t

e

r

e

s

t

r

a

t

e

s

a

r

e

c

a

l

c

u

l

a

t

e

d

b

y

s

u

b

t

r

a

c

t

i

n

g

t

h

e

o

n

e

q

u

a

r

t

e

r

a

h

e

a

d

i

n

f

l

a

t

i

o

n

r

a

t

e

f

r

o

m

t

h

e

n

o

m

i

n

a

l

l

e

n

d

i

n

g

r

a

t

e

.

S

h

a

d

e

d

a

r

e

a

s

i

n

d

i

c

a

t

e

p

e

r

i

o

d

s

d

u

r

i

n

g

w

h

i

c

h

t

h

e

p

r

o

g

r

a

m

s

w

e

r

e

i

n

p

l

a

c

e

.

10

The Boom-Recession Cycle.

Expectations, Real Interest Rates, and Output.

The “Temporariness” Hypothesis.

An Assessment.

The Behavior of Real Interest Rates.

Credibility, Nominal Anchors, and Interest Rates.

Expectations, Fiscal Adjustment, and Interest Rates.

Disinflation and Real Wages.

11

The Boom-Recession Cycle

First attempt at explaining the expansion-recession

cycle that appears to characterize exchange-rate-based

disinflation programs: Rodríguez (1982).

Alternative explanation: Calvo and Végh (1993a,

1993b).

Key feature of the latter approach: interactions between

lack of credibility and intertemporal substitution effects

in the transmission policy shocks to the real sphere of

the economy.

12

Expectations, Real Interest Rates,

and Output

The model developed by Rodríguez (1982) explains the

behavior of output in exchange-rate-based programs.

It is implemented in a small open economy.

Exchange-rate path is preannounced.

Money supply is endogenous.

Expectations follow a backward-looking process.

Capital is perfectly mobile internationally.

Domestic rate of inflation:

= N + (1-),

0 < < 1.

(1)

13

Rate of increase in world tradable prices is set to zero.

Inflation in nontraded goods prices:

N = Na + ’dN,

(2)

Na: expected behavior of prices in that sector;

dN: excess demand for nontradables.

(1) and (2) yield

= a + dN,

’ > 0.

= ’,

(3)

where a = Na + (1-).

Price expectations are revised using an adaptive

process:

.a

= ( - a),

> 0.

14

~

Aggregate supply is assumed constant at y.

Aggregate spending c varies inversely with the

expected real interest rate r = i - a, where i denotes the

nominal interest rate and c’ < 0.

Excess demand for tradable goods, dT (equal to the

trade balance deficit) depend negatively on the relative

price of these goods, defined as z = E/P.

Excess demand for nontradables:

~

+ -

dN = c(r) - y - dT(z) = dN(z, r).

(5)

15

Substituting (5) into (3) yields

- a = dN(z, r).

(6)

Unexpected movements in inflation are determined

uniquely by excess demand for home goods.

At any moment in time, real exchange rate z is given.

Over time, it changes according to

.

z/z = - .

(7)

16

Domestic nominal interest rate:

i = i* + ,

i*: constant world interest rate;

: devaluation rate.

To express the model in a compact form, differentiate r

with respect to time and use (4) and (6), so that

.

r = - dN(z, r).

(8)

(9)

Using (8) and the definition of r to substitute out for the

expected inflation rate in (6) yields

= i* + - r + dN(z, r).

(10)

17

Substituting (10) in (7) yields

.

z/z = r - i* - dN(z, r).

(11)

(9) and (11) constitute a differential equation system in r

and z.

For given levels of these variables, (10) determines .

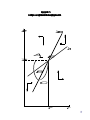

Figure 12.3: steady-state equilibrium of the model.

.

[r = 0]:

Obtained from (9).

Combinations of r and z for which there is no excess

demand in the nontraded goods market (dN = 0).

Positive slope since a depreciation in z creates

excess demand for home goods, which requires an

18

increase in r to restore equilibrium.

F

i

g

u

r

e

1

2

.

3

E

q

u

i

l

i

b

r

i

u

m

a

n

d

A

d

j

u

s

t

m

e

n

t

i

n

t

h

e

R

o

d

r

í

g

u

e

z

M

o

d

e

l

.

z

z

=

0

.

r

=

0

A

~

E

z

B

C

~

r

r

19

.

[z = 0]:

Derived from (11).

Positively sloped.

Combinations of r and z rate for which the latter

variable remains constant.

~

(9) and (11): in the steady state, r = i*.

(10): long-run is equal to .

20

System composed of (9) and (11) is stable if the

coefficient matrix defined by

M =

-(dN/r)

-(dN/z)

1 - (dN/r)

-(dN/z)

has a positive determinant and a negative trace:

detM = (dN/z) > 0,

trM = -[(dN/z) + (dN/r)] < 0.

Condition on detM is always satisfied, but condition on

trM does not necessarily hold.

21

Assume: trM holds ensures the local stability of the

long-run equilibrium of the economy (point E in Figure

12.3).

Assume: reduction in from h to s < h.

.

.

Change in does not affect the position of [r = 0] and [z

= 0], and therefore has no effect on the long-run

equilibrium levels of r and z.

However, reduction in reduces domestic r on impact

since, with expected given, it leads to a one-to-one

reduction i.

System moves from E to a short-run equilibrium position

such as point A, since z is predetermined.

Initial fall in r generates an excess demand for home

goods.

22

Reduction of tends to reduce prices, but the

emergence of excess demand tends to raise them.

Net effect on is positive, as indicated by (10) and (8).

Actual rises above the expected rate, which also

begins to rise.

Increase in expected reduces r further.

This leads to gradual appreciation of z.

Then excess demand for nontraded goods generated

by fall in r begins to dampen rate of z appreciation,

leading to an elimination of excess demand.

Equilibrium of nontraded goods market is restored at B.

23

Nevertheless, z continues to appreciate, because at B

domestic exceeds . This leads to

excess supply of nontraded goods;

fall in expected ;

rise in r (movement from B to C).

At C rate of change of z is zero, but excess supply

prevails.

Actual and expected continue to fall, leading to

depreciation of the exchange rate;

further rise in r.

Therefore, in the long run, the economy returns to its

initial equilibrium position at E.

New steady-state value of is equal to s < h.

24

Result: adjustment process following a permanent

reduction in is characterized by a period of excess

demand (short-run boom).

Rodríguez model: expansion of demand occurs as a

consequence of the assumption of backward-looking

expectations.

Initial reduction in leads to

fall in i;

downward jump in r;

increase in the demand for nontraded goods.

This expansion of demand in the home goods sector

puts upward pressure on domestic prices.

25

Ensuing appreciation of z dampens the expansion of

demand and eventually dominates the initial

expansionary effect, leading to a contraction in demand,

which results from domestic exceeding .

26

The “Temporariness” Hypothesis

Calvo and Végh (1993a, 1993b): alternative explanation

of boom-recession cycle based on rigorous optimizing

foundations and forward-looking expectations.

Small open economy producing traded and nontraded

goods.

Representative household maximizes the discounted

lifetime sum of utility, with instantaneous utility

separable in both goods:

0

ln(cT, cN)e-tdt,

>0

(12)

cN (cT): consumption of nontraded (traded) goods.

27

Households face a cash-in-advance constraint:

z-1cN + cT -1m,

> 0,

(13)

z = E/PN: real exchange rate;

m: real money balances measured in terms of traded

goods.

Households hold a stock bp of internationally traded

bonds, which bears a constant real rate of interest i*

determined on world capital markets.

a = m + bp: real financial wealth in terms of traded

goods.

28

Intertemporal resource constraint faced by the

consumer, which equates lifetime resources to lifetime

expenditures:

a0 +

0

(z-1yN + yT + )e-tdt =

0

(14)

(z-1cN + cT + im)e-tdt ,

yN: output of nontraded goods;

yT: exogenous level of output of traded goods;

: real transfers from the government;

i = i* + : domestic nominal interest rate, assuming that

uncovered interest parity condition holds (: devaluation

29

rate).

Households take as given a, yT, yN, , i, and z and

maximize (12) subject to the cash-in-advance constraint

(13) and lifetime resource constraint (14) by choosing a

sequence {cN, cT, m}

t=0.

Assuming that subjective discount rate is equal to the

world interest rate ( = i*), first-order conditions:

1/cT = (1 + i),

(16)

cN = zcT,

(17)

: marginal utility of wealth.

(16) equates the marginal utility of traded goods to the

product of the marginal utility of wealth and their real

30

effective price.

Real effective price: market price and opportunity cost

of holding units of money necessary to carry out the

transaction, i.

(17) equates the ratio of cN and cT to the relative price of

traded goods.

Output of nontraded goods is demand determined.

Rate of change of in the nontraded good sector, N, is

assumed to be negatively related to excess demand

(difference between actual output and its long-run level,

y~N):

.

N = -(cN - y~N) = (y~N - zcT),

> 0. (18)

31

Price mechanism specified in (18) follows the model of

staggered prices and wages developed by Calvo

(1983).

It relies on the assumption that firms in the nontraded

goods sector

determine the prices of their products in a

nonsynchronous manner;

while doing this, take into account the expected

future path of demand and of the average price

prevailing in the economy.

At any moment in time, only a small subset of firms may

change their individual prices.

Price level is thus a predetermined variable, but inflation

can jump, because it reflects changes in individual

prices set by firms.

32

Example:

When excess demand develops in the nontraded goods

sector, some firms increase their individual prices and

inflation rises.

Because the subset of firms that have yet to adjust their

prices to excess demand diminishes quickly, inflation in

home goods prices decreases over time.

Hence change in the home goods is inversely related

to excess demand for nontraded goods.

Formally:

There exists a large number of firms in the nontraded

goods sector, indexed in the interval between 0 and 1.

Each firm produces a non-storable good at a zero

variable cost, the quantity of which is demand

33

determined.

Probability of receiving the price signal n periods from

now is exp(-n), where > 0.

Under perfect foresight, price set by the firm price as of

period t is given by

V=

t

[pN(s) + EN(s)e-(s-t)ds,

>0

(19)

V: price quoted at t;

pN(s): price index for nontraded goods at period s;

EN(s) = cN - yN: excess demand at period s for

nontraded goods.

34

If price-change signal is independent across firms, the

proportion of prices set at time s that have not been

modified as of time t is given by e-(t-s).

Price index for nontraded goods is defined as the

weighted average of prices currently quoted:

pN =

t

Vse-(s-t)ds.

(20)

In the above formulation, pN, is a predetermined

variable at time t.

In contrast, V may jump when an unexpected change

takes place.

Along paths where pN and EN are uniquely determined,

V is a continuous function of time.

35

Differentiating (20) with respect to time yields

N = (V - pN),

(21)

.

where N pN.

Note that (21) holds at any point in time; in particular, it

holds at those points in time at which EN is not

continuous.

Hence, anticipated discontinuities in N cannot take

place even in the presence of anticipated discontinuities

in EN.

This is important when temporary changes in policy are

considered.

36

At points in time where EN is continuous, (19) can be

differentiated to yield

.

V = (V - pN - EN).

(22)

It follows from (21) and (22) that, at points in time at

which EN is continuous, and setting = 2 > 0 yields

.

~

= -EN = -(cN - yN).

Due to staggered price setting in the nontraded goods

sector, z is predetermined in the short run.

Differentiating z = E/PN with respect to time yields:

.

z/z = - N.

(23)

37

Assume: government buys no goods and redeems back

to households

interest income on the central bank's net foreign

assets

revenue from money creation.

Present value of government transfers:

0

e-tdt

g

= b0 +

0

.

(m + m) e-tdt,

(24)

g

b0: government's initial stock of bonds.

38

Combining (14), (15), and (16); defining the total stock

of bonds in the economy as b = bp + bg; and imposing

the transversality condition limt e-tb = 0 yields overall

resource constraint:

b0 + yT/ =

0

cTe-tdt,

(25)

b0: economy's initial stock of bonds.

(25) equates present value of tradable resources to

present value of purchases of traded goods.

39

Assuming further that transfers are used to compensate

households for the depreciation of real money balances

yields the economy's current account balance:

.

b = yT + i*b - cT.

Overall inflation rate is written as a weighted average of

devaluation rate and rate of inflation in home goods

prices:

= N + (1-),

0 < < 1,

: weight depends on the share of home goods in total

consumption expenditure.

40

Dynamics of the model are determined by (18), (23),

and (26).

Because output of traded goods is exogenous and

consumption of traded goods depends only on the

marginal utility of wealth, the system is recursive.

For a given path of cT and , (18) and (23) form

interdependent block:

.

~

0

-z

z

. = -c~ 0

N

T

z

+

N

~

z

~

~

yN - zcT

(28)

41

First row of (28): for z to remain constant over time, in

home goods prices must be equal to .

Second row: cN must be equal to long-run output for in

home goods prices to remain constant over time.

~ determinant of the matrix of coefficients

Since c~T = y~N/z,

~

is -yN < 0.

The system is therefore saddlepath stable.

42

Reduction of : Full Credibility

At time t the government announces an immediate and

permanent reduction in from h to s < h.

Permanent nature of the shock is interpreted as

indicating that the announcement carries full credibility.

Through the interest parity condition, reduction in

leads to a concomitant fall in i.

Because of full credibility, private agents will expect i to

remain forever at its lower level.

Since exchange-rate adjustment is expected to last

forever, private agents have no incentives to engage in

intertemporal consumption substitution.

Because tradable resources do not change, cT remains

constant over time.

43

Since cT is not affected by permanent changes in , a

fall in N that exactly matches the fall in immediately

moves the system to a new steady state.

Overall rate of the economy also falls instantaneously

to its new level, s.

Result: permanent, unanticipated reduction in

reduces instantaneously at no real costs and is thus

superneutral.

This result holds also if the system starts away from an

initial steady-state position.

Important property of the Calvo-Végh model:

Immediate downward jump in and absence of real

effects associated with a reduction in occurs despite

staggered price setting.

44

Price level rigidity does not imply stickiness in .

Reduction of : Imperfect Credibility

Government announces at t a reduction in , but the

public believes that the exchange-rate adjustment will

be reversed at some period T in the future.

Formally,

= s

for t0 t < T

= h > s

for t T.

Calvo and Végh interpret the belief that the policy is

temporary as arising from lack of credibility.

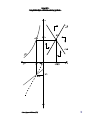

Figure 12.4: dynamic behavior of c, the current

account, z, and and r associated with a temporary

exchange-rate policy.

45

F

i

g

u

r

e

1

2

.

4

a

D

y

n

a

m

i

c

s

o

f

t

h

e

C

a

l

v

o

V

é

g

h

"

T

e

m

p

o

r

a

r

i

n

e

s

s

"

M

o

d

e

l

w

i

t

h

I

m

p

e

r

f

e

c

t

C

r

e

d

i

b

i

l

i

t

y

C

o

n

s

u

m

p

t

i

o

n

o

f

t

r

a

d

e

d

g

o

o

d

s

C

u

r

r

e

n

t

a

c

c

o

u

n

t

t

0T

0

t

i

m

e

t

t

i

m

e

0T

S

o

u

r

c

e

:

C

a

l

v

o

a

n

d

V

é

g

h

(

1

9

9

3

b

,

p

.

1

7

)

.

46

F

i

g

u

r

e

1

2

.

4

b

D

y

n

a

m

i

c

s

o

f

t

h

e

C

a

l

v

o

V

é

g

h

"

T

e

m

p

o

r

a

r

i

n

e

s

s

"

M

o

d

e

l

w

i

t

h

I

m

p

e

r

f

e

c

t

C

r

e

d

i

b

i

l

i

t

y

I

n

f

l

a

t

i

o

n

r

a

t

e

i

n

h

o

m

e

g

o

o

d

s

p

r

i

c

e

s

t

t

i

m

e

0T

R

e

a

l

e

x

c

h

a

n

g

e

r

a

t

e

t

t

i

m

e

0T

S

o

u

r

c

e

:

C

a

l

v

o

a

n

d

V

é

g

h

(

1

9

9

3

b

,

p

.

1

7

)

.

47

F

i

g

u

r

e

1

2

.

4

c

D

y

n

a

m

i

c

s

o

f

t

h

e

C

a

l

v

o

V

é

g

h

"

T

e

m

p

o

r

a

r

i

n

e

s

s

"

M

o

d

e

l

w

i

t

h

I

m

p

e

r

f

e

c

t

C

r

e

d

i

b

i

l

i

t

y

C

o

n

s

u

m

p

t

i

o

n

o

f

h

o

m

e

g

o

o

d

s

t

0T

t

i

m

e

D

o

m

e

s

t

i

c

r

e

a

l

i

n

t

e

r

e

s

t

r

a

t

e

t

0T

t

i

m

e

S

o

u

r

c

e

:

C

a

l

v

o

a

n

d

V

é

g

h

(

1

9

9

3

b

,

p

.

1

7

)

.

48

By (15), temporary reduction in implies that i is lower

in the interval (0, T).

Effective price of traded goods is also lower during the

interval (0, T) and cT jumps upward to a level higher

than initial permanent income (given by yT + i*b0).

Since intertemporal resource constraint of the economy

(25) must be satisfied for all equilibrium paths, cT must

subsequently (for t T) fall below initial permanent

income and remain forever at that lower level.

Upward jump in cT leads on impact to a current account

deficit.

During (0, T), the deficit increases due to a reduction of

interest receipts on foreign bonds.

When the policy is abandoned,

49

current account jumps into balance;

stock of foreign bonds remains permanently at a

lower level than initially.

Prices:

Effect of the reduction in on home goods prices is

ambiguous:

lower dampens in home goods prices;.

increase in aggregate demand raises .

In general, net effect is a reduction in in home goods

prices, but by less than .

After the initial fall, in home goods prices rises

continuously in anticipation of the expected resumption

of the higher .

At time T, the policymaker must decide whether to

abandon the program or maintain at the lower level.

50

If the authorities abandon the program, in home goods

prices will continue to increase toward its initial level

(Figure 12.4).

If the authorities decide to maintain the lower- policy,

then in home goods prices will jump downward at time

T and converge from below toward s.

Overall follows the same adjustment path during (0, T)

as in home goods prices.

Thus, temporary reduction in leads to inertia.

The more temporary the exchange-rate policy, or the

lower its degree of credibility, the lower the initial fall in .

Real exchange rate:

Because in home goods prices remains above , z

appreciates during (0, T).

51

At time T, regardless of whether the exchange-rate policy

is reversed or not, z begins to depreciate.

If at that moment the lower-devaluation policy is not

abandoned, in home goods prices falls below ,

generating real depreciation.

Domestic real interest rate:

Domestic r falls, because N drops by less than and the

concomitant fall in i.

It begins rising at first and then falls during the transition,

jumping upward when T is reached, due to the jump in i.

Since domestic increases gradually over time, r falls

monotonically toward its unchanged steady-state value

given by i*.

52

Consumption:

Since relative price of home goods in terms of traded

goods cannot change, increase in cT leads to a

proportional rise in c of home goods [Equation (17)].

Gradual appreciation of z reduces private expenditure on

home goods over time.

If the horizon is sufficiently far in the future, a recession

may set before T is reached.

If the horizon is short, output will remain above its fullemployment level throughout the transition period.

At time T cT and cN jumps downward.

After T, z begins to depreciate toward its long-run value,

stimulating c of home goods.

Thus, there is an initial c boom followed by a contraction.

53

The smaller T is, the more pronounced are the

intertemporal substitution effects, and the larger is the

initial rise in cT and c of home goods.

54

An Assessment

Rodríguez model:

Assumption of a backward-looking expectations are

untenable in the economies undergoing a comprehensive

macroeconomic adjustment program.

Predictions of the model can be altered once behavioral

functions are derived from a well-defined microeconomic

optimization process.

Calvo and Végh (1994): even in the presence of

backward-looking price expectations a permanent

reduction in may have a contractionary effect, rather

than an expansionary effect as predicted by Rodríguez.

This result is obtained because the appreciation of z has

an ambiguous effect on output:

55

real appreciation has a negative impact because it

increases the relative price of home goods;

it stimulates output because it leads to a reduction in

the domestic, consumption-based r.

Whether or not the latter effect dominates depends on

whether the intertemporal elasticity of substitution is

larger than the intratemporal elasticity of substitution

between traded and home goods.

Hence, backward-looking expectations may not be

sufficient to explain the initial expansion in output.

Calvo and Végh model:

Provides a conceptually appealing formulation of major

mechanisms at work in the behavior of output in

exchange-rate-based disinflation programs.

56

Emphasizes the role of forward-looking behavior and

expectations of future policy reversals.

Can be extended to account for uncertainty about the

date of the policy reversal and thus provides

explanation of the volatility of aggregate variables in

programs that lack credibility.

Corresponds well to the evidence observed in several

exchange-rate-based stabilization attempts that ended

in failure.

Prediction of a growing current account deficit may be

the only sign that the stabilization program is

unsustainable in this type of model.

57

Problems related to emphases on intertemporal

elasticity of substitution in Calvo-Végh model:

Model can explain the boom-recession puzzle

depending on the extent to which the degree of

intertemporal substitution can explain the large

observed changes in private consumption expenditure.

But, available evidence on the intertemporal channel

does not provide strong support for the theory.

Table 12.1: results of some recent studies that have

attempted to estimate the intertemporal elasticity of

substitution in developing countries.

Early estimates: elasticity is small and not

significantly different from zero.

Arrau (1990): elasticity is relatively low but

nevertheless statistically different from zero.

58

Even with low elasticities, observed movements in

interest rates may be large enough to generate

substantial changes in c.

Reinhart and Végh (1995):

despite low elasticities, predicted changes in c match

reasonably well the actual changes in the four

heterodox programs implemented in the 1980s;

but accuracy is poor.

Result: overall evidence does not provide

overwhelming support for the view that lack of credibility

and intertemporal factors explain output behavior in

exchange-rate-based programs.

59

Size of intertemporal elasticity of substitution may be

less important, since results depend also on whether

m and c are Pareto-Edgeworth complements.

Representative household attempts to keep the marginal

utility of consumption constant over time.

To do so, household must change the path of c if is

expected to increase at a well-defined future date.

Direction of this change depends on whether c and m are

substitutes or complements.

If cT and m are Pareto-Edgeworth complements, then

private agents consume more when i is temporarily lower,

leading to a deterioration of the current account.

If cT and m are Pareto-Edgeworth substitutes, agents

reduce c expenditure following a temporary fall in i,

leading to a transitory current account surplus.

60

Problems related to dependence of dynamic effects of

imperfectly credible policy to degree of

temporariness.

Because the period at which the policy is believed to be

discontinued is given, credibility is exogenous.

Key aspect of credibility is endogenous interactions

between policy decisions, economic outcomes, and the

degree of confidence that private agents attach to

policymakers' commitment to disinflate.

Existence of uncertainty regarding degree of

temporariness of stabilization program is also important.

Mendoza and Uribe (1996): uncertainty about duration

of the program may be sufficient to lead to boomrecession cycle, deteriorating current account, and z

appreciation.

61

Instead of sequence of jumps, gradual reduction in :

Obstfeld (1985): dynamics associated with this type of

policy, using an optimizing framework with continuous

market clearing and perfect foresight.

He emphasizes the importance of intertemporal

substitution effects in c generated by a gradual and

permanent reduction in .

Such a policy increases m, and, if m and c are

substitutes, c rises on impact and falls over time.

Initially: z appreciates and a current account deficit

emerges.

Later on: real depreciation occurs, and a gradual

reduction of the deficit takes place.

However, these predictions depend on the treatment of

62

m and c in households' utility function.

In Obstfeld's analysis, consumer's utility function

belongs to the constant relative-risk aversion class and

is defined by

u(c, m) =

(cm1- )1-/(1-) if < 1 or > 1

lnc + (1-)lnm

if = 1

0 < < 1;

1/: elasticity of intertemporal substitution.

Intratemporal elasticity of substitution between c and m

is equal to unity.

When < 1, c and m are Edgeworth-Pareto

complements, while when > 1 they are substitutes.

63

Roldós (1993):

Analysis of a gradual lowering of .

Models money also through a cash-in-advance

constraint.

Gradual, fully credible reduction in causes a real

exchange-rate appreciation and sustained current

account deficits.

Important feature: emphasis on the supply-side effects

of exchange-rate policy.

Initial boom occurs only when the intertemporal

elasticity of substitution in labor supply is larger than

that in consumption.

It occurs in both tradables and nontradables sectors as

real wages fall.

64

Reduction in raises the marginal value of wealth,

raising the opportunity cost of leisure and inducing an

increase in labor supply in the initial phase of the

program.

Recession does not occur later on.

This model provides a useful interpretation of the recent

Mexican stabilization experiment.

But its empirical importance is unclear.

Inclusion of durable goods:

Anticipated increase in and opportunity cost of

purchases immediately would induce

increase in spending on durable goods;

accumulation of inventories by firms;

investment in capital goods;

65

thereby causing a large increase in absorption.

Drazen (1990):

Behavior of imports of durable goods in exchange-ratebased disinflation programs.

Temporary exchange-rate freeze lead to fluctuations in

domestic output and durable goods imports

if there is uncertainty about the date at which the

freeze will end;

if it is believed to be associated with substantial

variations in relative prices.

Matsuyama (1991):

Exchange-rate-based stabilization programs may be

subject to “hysteresis” effects in the presence of durable

goods.

66

Temporary reduction in may have a permanent effect,

because such a change alters the initial condition for

some later moment when the policy is abandoned.

Other sources of real sector dynamics in exchangerate based stabilization programs:

Helpman and Razin (1987):

Based on the Blanchard-Yaari framework.

Unexpected exchange rate freeze generates capital

gains for agents currently alive.

Unexpectedly appreciated exchange rate increases the

real value of nominal asset holdings, such as money.

Since agents have a finite horizon, this wealth effect is

not fully offset by future tax liabilities.

Thus, exchange rate freeze brings about an increase in

67

c and deterioration of the current account.

Increase in future tax liabilities due to loss of reserves

attached to the freeze in the exchange rate.

Over time, share of population that benefits capital gain

declines while share that is subject to tax liabilities

increases, resulting in an eventual decline in c.

End result: temporarily higher c, worsening current

account, reserve losses and increase in government

debt.

68

The Behavior of Real

Interest Rates

Two alternative models:

They focus on

lack of credibility and presence of additional nominal

anchors;

expectations about future fiscal policy shocks.

69

Credibility, Nominal Anchors, and Interest

Rates

Rodríguez model: permanent, fully credible reduction in

leads to an immediate fall in r, because price

expectations are predetermined at any moment in time.

Calvo-Végh model: imperfectly credible exchange-rate

stabilization leads to an unambiguous fall in domestic r.

Calvo and Végh (1993b): if money is used as an

additional anchor due to imposition of capital controls or

adoption of a credit target, then r may rise at the

inception of imperfectly credible exchange-rate-based

program.

70

Example:

If capital controls are in place, money stock becomes

predetermined.

Increase in domestic money demand associated with

a reduction in requires an accommodating upward

adjustment in interest rates.

Given that falls, r will generally rise.

Israeli stabilization of the mid-1980s:

Sharp increase in r.

Restrictive credit policy is widely believed to have been

the major factor behind the rise in r.

However, there is not much evidence suggesting that

credit policy was significantly different in the programs

implemented in the 1970s and 1980s in Latin America.

71

Fiscal implications of exchange-rate-based

stabilization program:

Unanticipated reduction in leads to a deterioration of

financial position of the public sector, through

loss of seigniorage;

increase in real cost of servicing fixed-rate debt

issued when nominal interest rates were high.

Government must correct the fiscal deficit thus created

via changes in its policy instruments.

In a forward-looking world, expectations about the

nature of the instruments have effects on the behavior

of r.

72

Expectations, Fiscal Adjustment,

and Interest Rates

Implications of a two-stage stabilization program for the

behavior of r.

Lump-sum taxes are endogenously adjusted to balance

the budget.

Economy begins at t = 0 in a steady state, characterized

by “high” and “high” level of government spending, gh.

At t = 0 government decides to reduce from h to

s < h.

At the same time, government announces its intention

to reduce permanently public expenditure from gh to gs

in the future, at period T or some time after T.

73

New level of spending gs is common knowledge.

Public does not entirely believe the policy

announcement, and attributes only a given probability

0 < < 1 that reduction in g will be implemented.

: measure of the degree of credibility of the fiscal

component of the stabilization program.

When close to unity, agents are almost certain that

policy reform will eventually be carried out.

Level of spending that is expected to prevail after T is

equal to gs + (1-)gh.

Agénor (1998b): solution of the dynamic system yields a

“quasi” steady state, since it is associated with a policy

shock that may or may not occur at T or afterward.

Once T is reached, the policy is either implemented or

agents start believing it will never be.

74

Uncertainty eventually disappears, and becomes unity

or zero.

Thus, there would be a jump in all variables at some

moment after T, after which the economy begins

converging to its “final” steady state.

Solution of the model during the adjustment period 0 < t

< T is such that the transition that takes place at T is

perfectly anticipated.

Consider the two polar cases: close to zero and

positive.

is close to zero:

Case of a permanent, unanticipated reduction in

only at t = 0.

Announcement of a future fiscal adjustment that

carries little credibility implies that r is likely to fall.75

is close to unity and if initial reduction in is not too

large, r rate will rise.

The larger is, the larger will be the increase in r.

As long as is positive, behavior of r is indeterminate.

r may rise or fall depending on

degree of confidence in fiscal reform;

degree of intertemporal substitution;

size of the initial exchange-rate adjustment;

likely reduction in public spending.

Result: even when the exchange-rate policy component

of stabilization program is fully credible, large

fluctuations in r may be observed in adjustment process

if degree of confidence in the fiscal policy component

varies over time.

76

Disinflation and Real Wages

Wage policy used in stabilization programs:

Argentina's Austral Plan of June 1985:

Preceded by 22% increase in wages and subsequent

freeze.

When prices kept rising, nominal wages are raised by

8.5% by the end of the year and then adopted

quarterly wage adjustments.

Israel's stabilization plan of July 1985:

Granted 50% compensation for that month's inflation.

Then froze wages for 3 months in agreement

between government, entrepreneurs' association,

and workers' federation, the Histadrut.

77

Subsequent adjustments provided partial

compensation for previous inflation of 4% or more.

Bolivia's August 1985 plan:

Granted bonuses and then froze wages.

Later, it reduced restrictions on laying off workers,

eliminated wage indexation, and set a very low

minimum wage.

Brazil's Cruzado plan of February 1986:

Initial bonus of 8% of wages for all workers.

Minimum wage was increased by 16%.

Nominal wages were not frozen, and annual wage

negotiations were restored.

Wages were to be automatically adjusted when

inflation reached 20%.

78

Mexico's stabilization program implemented in end

1987-early 1988 relied on a collective agreement

between labor, employers, and the government.

Figures 12.5 and 12.6: behavior of real wages and

inflation during the tablita experiments and the

heterodox experiments of the 1980s in Israel and

Mexico.

Agénor (1998):

Long-term effects of stabilization policy may depend on

the nature of wage contracts.

Reduction in the rate of nominal devaluation may lead in

the long run to

contraction in output of tradables with backwardlooking nominal wage contracts;

79

expansion in activity with forward-looking contracts.

F

i

g

u

r

e

1

2

.

5

S

t

e

a

d

y

S

t

a

t

e

E

q

u

i

l

i

b

r

i

u

m

w

i

t

h

B

a

c

k

w

a

r

d

L

o

o

k

i

n

g

C

o

n

t

r

a

c

t

s

.

=

0

~

A

E

.

=

0

s

y

y

~

y

~

=

4

5

º

~

c

B

c

S

o

u

r

c

e

:

A

g

é

n

o

r

a

n

d

H

o

f

f

m

a

i

s

t

e

r

(

1

9

9

7

)

.

80

F

i

g

u

r

e

1

2

.

6

S

t

e

a

d

y

S

t

a

t

e

E

q

u

i

l

i

b

r

i

u

m

w

i

t

h

F

o

r

w

a

r

d

L

o

o

k

i

n

g

C

o

n

t

r

a

c

t

s

.

=

0

.

=

0

S

~

A

E

S

s

y

y

~

y

~

=

4

5

º

~

c

B

c

81

Short-run dynamics of real wages also depend on

nature of wage contracts.

Backward-looking nominal wage contracts:

Reduction in would lead at first to an increase in the

real wage followed by a gradual reduction over time, as

contracts begin to reflect the lower .

Experience of several Latin American countries in the

early 1980s: stabilization programs combining a fixed

nominal exchange rate with backward-looking wage

indexation leads to inflation inertia and results in

accelerating real appreciation of the exchange rate;

unsustainable widening of the current account deficit;

culminating in a balance of payments crisis;

exchange rate collapse.

82

Forward-looking nominal wage contracts:

Anticipated future reduction in inflation that carries full

credibility may lead either to an immediate fall in the real

wage or a temporary increase in the real wage.

If price and wage setters do not believe that the future

reduction in prices will take place, nominal wages will

not adjust, and real wage may show little response.

Model with backward- and forward-looking wage

contracts:

Economy produces a nonstorable good, which is an

imperfect substitute to the foreign good.

83

Domestic output y is inversely related to the real product

wage, = w/P, where w denotes nominal wage and P

price of the domestic good:

y = y(),

y’ < 0.

(29)

Consumption c depends

positively on income;

negatively on the expected long-run value of the

relative price of domestic good, z*:

_

+

c = c(y, z*),

0 < cy < 1.

(30)

84

z* must be consistent with relative price for which the

market for domestic goods clears in the long run:

~

~

c[y(),

z*] = y(),

from which we have, using (29):

~

~

z* = cz*(1 - cy)y’ = (),

-1

’ > 0.

Increase in the long-run value of , by increasing

excess demand for the domestic good leads to an

increase in the long-run expected relative price.

85

Changes in the inflation rate depend on excess

demand for goods and rate of depreciation of the real

exchange rate:

.

= (c - y) + ( - ),

, > 0.

Nominal wage w is set under two alternative contract

mechanisms.

When wage contracts are backward-looking and

depend only on past levels of prices:

w=

-

t

e-(t-k)Pkdk,

: discount rate.

86

Differentiating this with respect to time:

.

w = (w - P).

When nominal wage contracts are forward-looking and

to depend on future prices:

w=

t

e(t-k)Pkdk,

implying that

.

w = (P - w).

87

Real wage rate of change over time under backwardlooking contracts:

.

/ = -[1 - (1/)] - .

Under forward-looking wage contracts:

.

/ = [1 - (1/)] - .

.

.

Steady-state solution is characterized by = = 0 and

goods market equilibrium.

Under both types of contracts, inflation and the rate of

growth of nominal wages must be equal to the

devaluation in the long-run equilibrium.

88

Taking a linear approximation around the steady state

yields, with backward-looking contracts:

.

.

-/~

=

-~

(1-cy)y’ -

~

0

-

+

-

cz*z* +

(35)

~ = (1 + /)-1: steady-state level of the real wage.

With forward-looking contracts:

.

.

=

~

/

~

-

(1-cy)y’ -

~

0

-

+

-

cz*z* +

~ = (1 - /)-1: steady-state level of the real wage.

(36)

89

Stability of (35) with backward-looking contracts

requires that the determinant of the matrix A of

coefficients be positive, and that its trace be negative:

~

~

det A = / - (1 - cy)y’ > 0,

~

tr A = -( + /)

< 0.

These conditions are always satisfied here.

In (36) with forward-looking contracts, since real wage is

now a jump variable, saddlepath stability requires that

the determinant of the matrix of coefficients be negative:

det A = -/ - (1 - cy)y’ < 0.

~

~

This condition is interpreted graphically below.

90

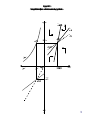

Figure 12.5: long-run equilibrium of the model under

backward-looking contracts.

.

[ = 0]: combinations of and for which does not

change over time.

.

[ = 0]: combinations of and for which does not

change.

Curve ys: inverse relationship between output and .

Consumption function [Equation (30)] is represented in

south-west panel.

Long-run equilibrium values of and are obtained at

E, with output determined at point A and consumption

determined at point B.

91

Figure 12.6: long-run equilibrium under forward-looking

contracts.

.

[ = 0] : upward-sloping in the north-east quadrant.

.

Saddlepath stability requires that the curve [ = 0] be

.

steeper than the curve [ = 0].

SS: saddlepath and it has a positive slope.

Consider the effect of a disinflation program that takes

the form of a permanent, unanticipated reduction in the

devaluation rate, from h to s < h.

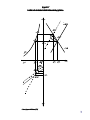

Figure 12.7: dynamics under backward-looking

contracts.

.

Curve [ = 0] shifts to the left.

Neither nor changes on impact.

92

F

i

g

u

r

e

1

2

.

7

R

e

d

u

c

t

i

o

n

i

n

t

h

e

D

e

v

a

l

u

a

t

i

o

n

R

a

t

e

w

i

t

h

B

a

c

k

w

a

r

d

L

o

o

k

i

n

g

C

o

n

t

r

a

c

t

s

.

=

0

E

'

A

'

D

E

A

~

.

=

0

s

y

y

~

s

h

4

5

º

y

B

'

'

B

'

~

B

c

c

S

o

u

r

c

e

:

A

g

é

n

o

r

a

n

d

H

o

f

f

m

a

i

s

t

e

r

(

1

9

9

7

)

.

93

rises monotonically throughout adjustment process.

may either fall continuously or may fall at first and

increase in a second stage.

Mimicking of , output falls continuously from point A to

A’ in the north-west quadrant.

Expected long-run relative price z* falls immediately to

reflect long-run increase in , thereby shifting downward

consumption function.

Equilibrium of the market for domestic goods is

maintained in the long run (point B’’).

Fall in consumption on impact (from B to point B’), with

output unchanged at its initial steady-state value, tends

to create excess supply of domestic goods.

This increases downward pressure on resulting from

94

reduction in .

Figure 12.8: forward-looking contracts.

Agents discount future reduction in back to the

present.

jumps downward immediately to a point such as A on

the new saddlepath S’S’ and continues to fall towards

its lower steady-state level, which is also reached at E’.

always falls continuously.

Mimicking , output increases from point A to A’ in the

north-west quadrant, and continues to increase until it

reaches point A’’.

Expected long-run relative price z* increases to reflect

long-run reduction in , thereby shifting upward the

consumption function and ensuring that goods market

equilibrium holds in the long run (point B’’).

95

F

i

g

u

r

e

1

2

.

8

R

e

d

u

c

t

i

o

n

i

n

t

h

e

D

e

v

a

l

u

a

t

i

o

n

R

a

t

e

w

i

t

h

F

o

r

w

a

r

d

L

o

o

k

i

n

g

C

o

n

t

r

a

c

t

s

A

.

=

0.

=

0

S

~

E

S

'

A

'

D

S

A

'

'

S

'

E

'

s

y

y

s

~

5

º

y4

h

~

c

B

B

'

B

'

'

c

96

Since both consumption and output rise, net effect on

excess demand cannot be determined a priori.

Agénor and Hoffmaister (1997): if the sensitivity of c to

the expected long-run z is sufficiently small, net effect is

negative, thereby reinforcing deflationary effect of

reduction in .

Result:

Adjustment process to a cut in leads to gradual

increase in with backward-looking contracts.

It leads to initial downward jump followed by a

continuous fall in with forward-looking contracts.

Evidence on evolution of real wages:

Figures 12.9 and 12.10: the tablita experiments of the

late 1970s in Latin America and the heterodox

experiments of the mid-1980s in Israel and Mexico. 97

F

i

g

u

r

e

1

2

.

9

a

I

n

f

l

a

t

i

o

n

a

n

d

R

e

a

l

W

a

g

e

s

i

n

t

h

e

T

a

b

l

i

t

a

E

x

p

e

r

i

m

e

n

t

s

R

e

a

l

w

a

g

e

i

n

d

e

x

(

1

9

7

8

=

1

0

0

,

l

e

f

t

s

c

a

l

e

)

I

n

f

l

a

t

i

o

n

r

a

t

e

(

i

n

p

e

r

c

e

n

t

,

r

i

g

h

t

s

c

a

l

e

)

1

3

0

A

r

g

e

n

t

i

n

a

4

0

0

1

2

5

3

5

0

1

2

0

3

0

0

1

1

5

2

5

0

1

1

0

2

0

0

1

0

5

1

5

0

1

0

0

1

0

0

9

5

1

9

7

8

1

9

7

9

1

9

8

0

1

9

8

1

5

0

1

9

8

2

S

o

u

r

c

e

:

V

é

g

h

(

1

9

9

2

)

.

N

o

t

e

:

S

h

a

d

e

d

a

r

e

a

s

i

n

d

i

c

a

t

e

p

e

r

i

o

d

s

d

u

r

i

n

g

w

h

i

c

h

t

h

e

p

r

o

g

r

a

m

s

w

e

r

e

i

n

p

l

a

c

e

.

98

F

i

g

u

r

e

1

2

.

9

b

I

n

f

l

a

t

i

o

n

a

n

d

R

e

a

l

W

a

g

e

s

i

n

t

h

e

T

a

b

l

i

t

a

E

x

p

e

r

i

m

e

n

t

s

R

e

a

l

w

a

g

e

i

n

d

e

x

(

1

9

7

8

=

1

0

0

,

l

e

f

t

s

c

a

l

e

)

I

n

f

l

a

t

i

o

n

r

a

t

e

(

i

n

p

e

r

c

e

n

t

,

r

i

g

h

t

s

c

a

l

e

)

1

3

5

C

h

i

l

e

6

0

1

3

0

5

0

1

2

5

4

0

1

2

0

1

1

5

3

0

1

1

0

2

0

1

0

5

1

0

1

0

0

9

5

1

9

7

7

1

9

7

8

1

9

7

9

1

9

8

0

1

9

8

1

1

9

8

2

0

1

9

8

3

S

o

u

r

c

e

:

V

é

g

h

(

1

9

9

2

)

.

N

o

t

e

:

S

h

a

d

e

d

a

r

e

a

s

i

n

d

i

c

a

t

e

p

e

r

i

o

d

s

d

u

r

i

n

g

w

h

i

c

h

t

h

e

p

r

o

g

r

a

m

s

w

e

r

e

i

n

p

l

a

c

e

.

99

F

i

g

u

r

e

1

2

.

9

c

I

n

f

l

a

t

i

o

n

a

n

d

R

e

a

l

W

a

g

e

s

i

n

t

h

e

T

a

b

l

i

t

a

E

x

p

e

r

i

m

e

n

t

s

R

e

a

l

w

a

g

e

i

n

d

e

x

(

1

9

7

8

=

1

0

0

,

l

e

f

t

s

c

a

l

e

)

I

n

f

l

a

t

i

o

n

r

a

t

e

(

i

n

p

e

r

c

e

n

t

,

r

i

g

h

t

s

c

a

l

e

)

1

1

0

U

r

u

g

u

a

y

1

0

0

1

0

5

8

0

1

0

0

6

0

9

5

4

0

9

0

2

0

8

5

8

0

1

9

7

8

1

9

7

9

1

9

8

0

1

9

8

1

1

9

8

2

0

1

9

8

3

S

o

u

r

c

e

:

V

é

g

h

(

1

9

9

2

)

.

N

o

t

e

:

S

h

a

d

e

d

a

r

e

a

s

i

n

d

i

c

a

t

e

p

e

r

i

o

d

s

d

u

r

i

n

g

w

h

i

c

h

t

h

e

p

r

o

g

r

a

m

s

w

e

r

e

i

n

p

l

a

c

e

.

100

F

i

g

u

r

e

1

2

.

1

0

a

I

n

f

l

a

t

i

o

n

a

n

d

R

e

a

l

W

a

g

e

s

i

n

H

e

t

e

r

o

d

o

x

E

x

p

e

r

i

m

e

n

t

s

6

0

I

s

r

a

e

l

1

1

0

R

e

a

l

w

a

g

e

i

n

d

e

x

(

r

i

g

h

t

s

c

a

l

e

,

1

9

8

5

=

1

0

0

)

5

0

1

0

0

4

0

9

0

3

0

8

0

2

0

1

0

I

n

f

l

a

t

i

o

n

r

a

t

e

(

l

e

f

t

s

c

a

l

e

)

0

7

0

6

0

1

9

8

0

q

1 1

9

8

2

q

1 1

9

8

4

q

1 1

9

8

6

q

1 1

9

8

8

q

1 1

9

9

0

q

1 1

9

9

2

q

1 1

9

9

3

q

4

S

o

u

r

c

e

:

I

n

t

e

r

n

a

t

i

o

n

a

l

M

o

n

e

t

a

r

y

F

u

n

d

.

N

o

t

e

:

T

h

e

v

e

r

t

i

c

a

l

l

i

n

e

i

n

d

i

c

a

t

e

s

t

h

e

s

t

a

r

t

o

f

t

h

e

s

t

a

b

i

l

i

z

a

t

i

o

n

p

r

o

g

r

a

m