Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Financialization wikipedia , lookup

Expenditures in the United States federal budget wikipedia , lookup

Debt settlement wikipedia , lookup

Debt collection wikipedia , lookup

First Report on the Public Credit wikipedia , lookup

Gross domestic product wikipedia , lookup

Debtors Anonymous wikipedia , lookup

Debt bondage wikipedia , lookup

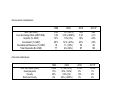

Eighth UNCTAD Debt Management Conference Geneva, 14 - 16 November 2011 Principles for Promoting Responsible Sovereign Lending and Borrowing by H.E. Mr. Hernán Lorenzino Secretary of Finance the Argentine Republic The views expressed are those of the author and do not necessarily reflect the views of UNCTAD VIII Debt Management Conference PRINCIPLES FOR PROMOTING RESPONSIBLE SOVEREIGN LENDING AND BORROWING The Argentinean perspective Hernán Lorenzino Secretary of Finance of the Republic of Argentina Geneva, November 2011 The Argentinean experience • Situation that led to the default – Spiraling debt burden and default over USD 82 Bn of bonded debt Gross Public Debt of GDP ) Gross Public Debt (%(%GDP) 160 140 % of GDP using 2004's Real FX from 1990 on 120 % of GDP with actual Nominal FX 100 80 60 Currency Board Period 40 20 0 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 • During the currency board regime (’91-’01), the “debt problem” was hidden by full access to debt markets and an artificially low FX. The Argentinean experience • Situation that led to the default – Maturities concentrated in the short term Debt maturity profile prior to the default 20 8% 18 T-notes 16 Loans 14 Bonded debt % GDP US$ Bn (capital, Mn US$, % GDP2001) Debt composition by currency prior to the default US$ 128 Bn 6% "Services to GDP" 12 AR Peso, 4% Other currencies, 7% 10 4% Euro, 20% 8 6 2% 4 US Dollar, 68% 2 0 0% 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 • Half of debt maturing within 3 years. • 88% of debt services (k+i) maturing in 5 years. • A decade of BoP structural deficit. • Financial markets closed for new Argentine financing. • 96% of total debt denominated in foreign currency. • 93% of total debt held by private creditors and IFIs. NO ACCESS TO NEW FUNDING + DEEP ECONOMIC RECESSION = INEVITABLE DEFAULT The Argentinean experience • Economic indicators GDP (Bn USD) Ave. Exchange Rate (ARP/US$) Imports (% GDP) Investment (% GDP) International Reserves (% GDP) Total Deposits (Bn USD) 1998 2002 2010 2011P 299 1,00 13% 20% 18 77 101 (-66%) 3,09 (+209%) 13% (0%) 12% (-40%) 11 (-39%) 26 (-64%) 369 3,91 18% 23% 50 87 429 4,13 20% 22% 48 103 • Social indicators GDP per capita (USD) Unemployment Poverty Extreme Poverty 1998 8.300 13% 25% 6% 2002 2.700 (-67%) 20% (+54%) 52% (0%) 24% (+300%) 2010 9.100 8% 12% 3% 2011P 10.500 7% 8% 2% The Argentinean experience - Debt exchanges 2005 2010 • Par • Discount • Cuasi-Par • GDP warrants • Par • Discount • GDP warrants Payment of PDI* In cash to all holders In cash for the Par option and Global 17 for the Discount option Commissions Charged to the Republic Charged to the holder Marketability of the issuance New instruments Liquid secondary market Macroeconomic context Recovering from the crisis High & stable 7-year growth track-record Securities Offered *Recognized from 12/31/2003 The Argentinean experience Gross Debt, Net Debt, External Debt & International Reserves (all as % of GDP) 166% 160% 164% Public debt / GDP 140% Net debt / GDP 120% 100% External debt / GDP 95% IR / GDP 80% 60% 46.3% 40% 20% 23% 17% 14% 11% 0% Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Mar-11 • Sustained downward trend in external debt as a consequence of a sustained GDP growth and a significant improvement in the debt composition. THANK YOU