Capital Flows, Interest Rates and Precautionary Behaviour: a model of

... • Cost of Reserves: term premium. 1.5% • Miller and Zhang: “excess” saving and insurance premium ...

... • Cost of Reserves: term premium. 1.5% • Miller and Zhang: “excess” saving and insurance premium ...

naic blanks (e) working group - National Association of Insurance

... believes that this definition captures a CDA’s basic design structure. The definition was adopted by the Life Insurance and Annuities (A) Committee. NAIC STAFF COMMENTS Comment on Effective Reporting Date: Other Comments: ...

... believes that this definition captures a CDA’s basic design structure. The definition was adopted by the Life Insurance and Annuities (A) Committee. NAIC STAFF COMMENTS Comment on Effective Reporting Date: Other Comments: ...

Slide 1

... number of exposure units so that the law of large numbers can operate to provide a substantially accurate prediction of future losses. ...

... number of exposure units so that the law of large numbers can operate to provide a substantially accurate prediction of future losses. ...

Financial Policy It is our goal to provide high quality dental care to all

... you with treatment options that best meet your needs, not try to match your care with your insurance plan limitations. Dental insurance plans do not correspond to individual patient needs, and as such, many routine and necessary dental services are not covered even though you may need those services ...

... you with treatment options that best meet your needs, not try to match your care with your insurance plan limitations. Dental insurance plans do not correspond to individual patient needs, and as such, many routine and necessary dental services are not covered even though you may need those services ...

Insurance Requirements

... Auto liability insurance is required if vehicles are used for other than normal and standard commute purposes. If applicable, this coverage is required for owned, nonowned, leased or hired vehicles with a minimum coverage limit of $500,000 The City of Fort Collins does not facilitate Special Event I ...

... Auto liability insurance is required if vehicles are used for other than normal and standard commute purposes. If applicable, this coverage is required for owned, nonowned, leased or hired vehicles with a minimum coverage limit of $500,000 The City of Fort Collins does not facilitate Special Event I ...

Liability Regimes

... – Inadequate understanding of the insurance function: every system needs to be controlled, guaranteed, and financially protected when it fails. – Underestimation of the importance of insurance for the development of a modern society and ...

... – Inadequate understanding of the insurance function: every system needs to be controlled, guaranteed, and financially protected when it fails. – Underestimation of the importance of insurance for the development of a modern society and ...

Credit Life and Disability Insurance

... -The insurance company pays benefits when you are totally disabled due to a covered illness or injury. -The insurance company pays benefits even if you are at home under a doctor’s care. Hospitalization is not required. -The insurance company continues benefits until your doctor releases you from yo ...

... -The insurance company pays benefits when you are totally disabled due to a covered illness or injury. -The insurance company pays benefits even if you are at home under a doctor’s care. Hospitalization is not required. -The insurance company continues benefits until your doctor releases you from yo ...

Slide 1 - Miami Beach Senior High School

... Which of the following is a major factor in nearly a third of all business bankruptcies? a. b. c. ...

... Which of the following is a major factor in nearly a third of all business bankruptcies? a. b. c. ...

FINANCIAL POLICY • CO-PAYS ARE DUE AT THE TIME OF

... It is our policy to bill your insurance company for you. However, we need your assistance in keeping us updated regarding any changes to your insurance information. Your policy is a contract between you and your insurance company. You will be responsible for any charges that are not covered by your ...

... It is our policy to bill your insurance company for you. However, we need your assistance in keeping us updated regarding any changes to your insurance information. Your policy is a contract between you and your insurance company. You will be responsible for any charges that are not covered by your ...

The Upside of Pooling Regulation

... Three years of premium and loss information and; Explanation of rate-making procedures; including at least one: • A description of any statistical and actuarial methods used • A statement of facts which explain judgements used • A statement as to how the rates of the filing company compare with thos ...

... Three years of premium and loss information and; Explanation of rate-making procedures; including at least one: • A description of any statistical and actuarial methods used • A statement of facts which explain judgements used • A statement as to how the rates of the filing company compare with thos ...

BUSINESS SUCCESSION PLANNING * Measuring the Opportunities

... PRIVILEGE RIDER (QPEP) HOW IT WORKS • Participant surrenders policy for its cash surrender value and retains the proceeds under the plan or rollover to an IRA. • New policy issued outside of plan for Net Amount at Risk (Face Amount – CV) without any medical evidence, regardless of health, at current ...

... PRIVILEGE RIDER (QPEP) HOW IT WORKS • Participant surrenders policy for its cash surrender value and retains the proceeds under the plan or rollover to an IRA. • New policy issued outside of plan for Net Amount at Risk (Face Amount – CV) without any medical evidence, regardless of health, at current ...

Are you working without the knowledge of your legal responsibilities?

... Financial Failure Insurance. Whilst the Trust Account route may sound favourable it is somewhat cumbersome in that there is a detrimental impact on your cash flow as all monies must be paid in to the Trust Account and can’t be released until the trip has returned home. This in effect means payments ...

... Financial Failure Insurance. Whilst the Trust Account route may sound favourable it is somewhat cumbersome in that there is a detrimental impact on your cash flow as all monies must be paid in to the Trust Account and can’t be released until the trip has returned home. This in effect means payments ...

Do Internal Fees in Life Insurance Make a Difference?

... getting in the performance of invested assets underlying policy cash values. Given findings from independent studies2 indicating there can be as much as a 80% swing between best-available rates and terms and poorly-priced products, the opportunity to bring reduced policy expenses and/or improved per ...

... getting in the performance of invested assets underlying policy cash values. Given findings from independent studies2 indicating there can be as much as a 80% swing between best-available rates and terms and poorly-priced products, the opportunity to bring reduced policy expenses and/or improved per ...

Overview of Insurance Companies

... In 1988: 2,300 life insurance companies with aggregate assets of $1.12 trillion. In early 2000s: 1,500 companies / $3.4 trillion (2003). 5 largest wrote 21% of new premium business Demutualization Adverse selection Insured have higher risk than general population Alleviated by grouping of ...

... In 1988: 2,300 life insurance companies with aggregate assets of $1.12 trillion. In early 2000s: 1,500 companies / $3.4 trillion (2003). 5 largest wrote 21% of new premium business Demutualization Adverse selection Insured have higher risk than general population Alleviated by grouping of ...

Increase Collections from Insurance Companies

... Prairie Ridge Addiction Treatment Services in Mason City, Iowa increased fee-for-service revenues from $627,193 to $1,008,367 in two years by targeting their marketing efforts on the 40 percent of their business that was fee-for-service, including third party insurance, Medicaid, and self-pay client ...

... Prairie Ridge Addiction Treatment Services in Mason City, Iowa increased fee-for-service revenues from $627,193 to $1,008,367 in two years by targeting their marketing efforts on the 40 percent of their business that was fee-for-service, including third party insurance, Medicaid, and self-pay client ...

Why You Need Title Insurance

... lenders who package and sell their loans in the secondary mortgage market. For the homeowner to be covered, he or she must have an owner’s policy in addition to the required lender or mortgagee policy. A separate owner’s policy is the best policy. Owner’s title insurance lasts as long as the policyh ...

... lenders who package and sell their loans in the secondary mortgage market. For the homeowner to be covered, he or she must have an owner’s policy in addition to the required lender or mortgagee policy. A separate owner’s policy is the best policy. Owner’s title insurance lasts as long as the policyh ...

Office_Policies_

... insurance coverage. I agree to pay my account in accordance with the regular rates and terms of this office. If my account is referred for collection, I agree to reimburse the fees of any collection agency, which may be based on a percentage at a maximum of 55% of the debt, and all costs and expense ...

... insurance coverage. I agree to pay my account in accordance with the regular rates and terms of this office. If my account is referred for collection, I agree to reimburse the fees of any collection agency, which may be based on a percentage at a maximum of 55% of the debt, and all costs and expense ...

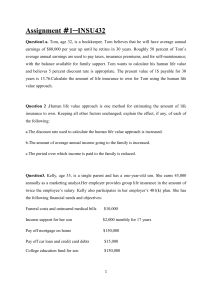

Assignment #1 File

... Question 2 .Human life value approach is one method for estimating the amount of life insurance to own. Keeping all other factors unchanged; explain the effect, if any, of each of the following: a.The discount rate used to calculate the human life value approach is increased. b.The amount of average ...

... Question 2 .Human life value approach is one method for estimating the amount of life insurance to own. Keeping all other factors unchanged; explain the effect, if any, of each of the following: a.The discount rate used to calculate the human life value approach is increased. b.The amount of average ...

On Regulation of Financial Institutions – 07/11/97

... WHEREAS, GLBA provides for functional regulation of financial institutions and specifically reaffirms state regulation of insurance and specifically provides that no person may sell insurance without being properly licensed by the states; and WHEREAS, state laws contain comprehensive provisions for ...

... WHEREAS, GLBA provides for functional regulation of financial institutions and specifically reaffirms state regulation of insurance and specifically provides that no person may sell insurance without being properly licensed by the states; and WHEREAS, state laws contain comprehensive provisions for ...

Law for Business

... What is a Insurance? Protection against financial loss Insurance companies share risk and charge a premium which represents their estimate of average losses plus a competitive profit The contract outlining payments between you and the insurance company is known as a policy ...

... What is a Insurance? Protection against financial loss Insurance companies share risk and charge a premium which represents their estimate of average losses plus a competitive profit The contract outlining payments between you and the insurance company is known as a policy ...

COMMERCIAL AUTO PLUS ENDORSEMENT CA 81 68 HIGHLIGHTS

... This coverage enhancement endorsement offers broadened coverages under your client company’s commercial auto policy. Cancellation Condition broadened to 60 days notice (except for non-payment of premium) Broadened definition of “Insured”: - any legally incorporated subsidiary the client company has ...

... This coverage enhancement endorsement offers broadened coverages under your client company’s commercial auto policy. Cancellation Condition broadened to 60 days notice (except for non-payment of premium) Broadened definition of “Insured”: - any legally incorporated subsidiary the client company has ...

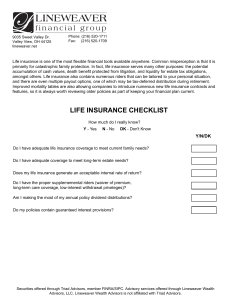

life insurance checklist - Lineweaver Financial Group

... primarily for catastrophic family protection. In fact, life insurance serves many other purposes: the potential accumulation of cash values, death benefit protected from litigation, and liquidity for estate tax obligations, amongst others. Life insurance also contains numerous riders that can be tai ...

... primarily for catastrophic family protection. In fact, life insurance serves many other purposes: the potential accumulation of cash values, death benefit protected from litigation, and liquidity for estate tax obligations, amongst others. Life insurance also contains numerous riders that can be tai ...

Insurance

... Insurance • Insurance: an arrangement where a company or government agency provides guaranteed compensation in case of a certain event for a premium (payment). • This provides you with a certain financial protection. • Types of insurance: – Car, health, renters, life, liability (lawsuits), travel, d ...

... Insurance • Insurance: an arrangement where a company or government agency provides guaranteed compensation in case of a certain event for a premium (payment). • This provides you with a certain financial protection. • Types of insurance: – Car, health, renters, life, liability (lawsuits), travel, d ...

Insurance

Insurance is the equitable transfer of the risk of a loss, from one entity to another in exchange for money. It is a form of risk management primarily used to hedge against the risk of a contingent, uncertain loss. An insurer, or insurance carrier, is selling the insurance; the insured, or policyholder, is the person or entity buying the insurance policy. The amount of money to be charged for a certain amount of insurance coverage is called the premium. Risk management, the practice of appraising and controlling risk, has evolved as a discrete field of study and practice.The transaction involves the insured assuming a guaranteed and known relatively small loss in the form of payment to the insurer in exchange for the insurer's promise to compensate (indemnity) the insured in the case of a financial (personal) loss. The insured receives a contract, called the insurance policy, which details the conditions and circumstances under which the insured will be financially compensated.