Actuarially Consistent Valuation in an Integrated Market

... to the filtration (Ft )0≤t≤T which is a natural requirement. As asset price processes are not a priori assumed to be semimartingales stochastic integrals that reflect achievable gains from continuous trading strategies are not well-defined. To circumvent this problem, the set of trading strategies i ...

... to the filtration (Ft )0≤t≤T which is a natural requirement. As asset price processes are not a priori assumed to be semimartingales stochastic integrals that reflect achievable gains from continuous trading strategies are not well-defined. To circumvent this problem, the set of trading strategies i ...

Taisei Fire and Marine Insurance Co.

... reinsurer, which was owned by the principals and close family of Fortress executives. Carolina Re subsequently became insolvent with $350 million in liabilities and was liquidated by a Bermuda court in late 2001. How did it happen ‐ the unforeseen nature of claims The ...

... reinsurer, which was owned by the principals and close family of Fortress executives. Carolina Re subsequently became insolvent with $350 million in liabilities and was liquidated by a Bermuda court in late 2001. How did it happen ‐ the unforeseen nature of claims The ...

A New Player: Contract Litigation Insurance

... CLI may also become an important consideration for litigation decision makers who are fiduciaries or otherwise acting in representative capacities. For example, an ERISA fiduciary or bankruptcy trustee bringing or defending a contract claim may become concerned about the possibilities of future cri ...

... CLI may also become an important consideration for litigation decision makers who are fiduciaries or otherwise acting in representative capacities. For example, an ERISA fiduciary or bankruptcy trustee bringing or defending a contract claim may become concerned about the possibilities of future cri ...

namic-030415 - Insurance Information Institute

... Flat to modest premium growth in 2015 Rate environment suggests flat-to-slightly negative renewals in late 2014/early 2015, but results vary Economic strengthening, stronger jobs market are pluses and should drive new exposures Construction, manufacturing have been growth areas but cooled in ...

... Flat to modest premium growth in 2015 Rate environment suggests flat-to-slightly negative renewals in late 2014/early 2015, but results vary Economic strengthening, stronger jobs market are pluses and should drive new exposures Construction, manufacturing have been growth areas but cooled in ...

italian insurance in figures

... In 2015, the shareholders’ funds were equal to 66.1 billion and increased by 2.7%. They amounted to 9% of the total liabilities. The overall technical provisions (direct and indirect, domestic and foreign business) were equal to 647 billion, increasing by 9.4% compared to 2014; life provisions, acco ...

... In 2015, the shareholders’ funds were equal to 66.1 billion and increased by 2.7%. They amounted to 9% of the total liabilities. The overall technical provisions (direct and indirect, domestic and foreign business) were equal to 647 billion, increasing by 9.4% compared to 2014; life provisions, acco ...

The Intersection of Finance and Insurance - mynl.com

... hedge market risk associated with approximately 19.3 million of the 36.1 million shares of Global Crossing owned by the Company. These option agreements were structured as collars in which the Company purchased put options and sold call options on Global Crossing common stock. The average exercise p ...

... hedge market risk associated with approximately 19.3 million of the 36.1 million shares of Global Crossing owned by the Company. These option agreements were structured as collars in which the Company purchased put options and sold call options on Global Crossing common stock. The average exercise p ...

IOSR Journal of Business and Management (IOSR-JBM) e-ISSN: 2278-487X.

... incentive to collect and analyze information about loss exposures, since the more precisely they measure the cost of risk, the more they can expand. As a result, the insurance market generates price signals to the entire economy, helping to allocate resources to more productive uses. Insurers also h ...

... incentive to collect and analyze information about loss exposures, since the more precisely they measure the cost of risk, the more they can expand. As a result, the insurance market generates price signals to the entire economy, helping to allocate resources to more productive uses. Insurers also h ...

1 Anti-Money Laundering Program and Suspicious Activity

... financing risks as they apply to the insurance industry. We do not expect that this program can prevent all potential money laundering. What is expected is that your business will take prudent steps, with the same kind of thought and care that you take to guard against other crimes, such as theft or ...

... financing risks as they apply to the insurance industry. We do not expect that this program can prevent all potential money laundering. What is expected is that your business will take prudent steps, with the same kind of thought and care that you take to guard against other crimes, such as theft or ...

A two-period model of an insurer with catastrophic loss and capacity

... will follow capital shocks, such as those caused by a large natural disaster or a significant macroeconomic event. This is, in part, due to relatively high capital adjustment costs1. In the property-liability insurance market, the mismatch between an unexpected catastrophe loss and limited capital c ...

... will follow capital shocks, such as those caused by a large natural disaster or a significant macroeconomic event. This is, in part, due to relatively high capital adjustment costs1. In the property-liability insurance market, the mismatch between an unexpected catastrophe loss and limited capital c ...

Denmark

... owner of a mortgaged property is obliged to maintain fire insurance for the full value of the property. Likewise, a standard form bill of sale creating a mortgage on moveable property includes a provision to the effect that the owner of the mortgaged property is obliged to maintain fire insurance fo ...

... owner of a mortgaged property is obliged to maintain fire insurance for the full value of the property. Likewise, a standard form bill of sale creating a mortgage on moveable property includes a provision to the effect that the owner of the mortgaged property is obliged to maintain fire insurance fo ...

Bulletin Reserve Bank of New Zealand The insurance sector and

... The Reserve Bank is responsible for promoting the maintenance of a sound and efficient financial system. The New Zealand insurance sector forms a key part of the financial system, and makes an important contribution to economic growth and development. Disruption to the insurance sector and the servi ...

... The Reserve Bank is responsible for promoting the maintenance of a sound and efficient financial system. The New Zealand insurance sector forms a key part of the financial system, and makes an important contribution to economic growth and development. Disruption to the insurance sector and the servi ...

the role of the marketing mix in the improvement of

... Taking into account all the aforementioned specifics of agriculture, the paper analyzes the so called pull factors that can essentially assist popularization of insurance. As an important institution of the economic system, insurance should facilitate both efficient and effective functioning of agri ...

... Taking into account all the aforementioned specifics of agriculture, the paper analyzes the so called pull factors that can essentially assist popularization of insurance. As an important institution of the economic system, insurance should facilitate both efficient and effective functioning of agri ...

Insurer solvency standards - Reserve Bank of New Zealand

... Significant earthquakes in Christchurch have brought the need for stability in the New Zealand insurance market into sharp focus. The ability of insurance companies to meet claims as they fall due has tremendous potential impact in such circumstances and the need for insurers to hold sufficient capi ...

... Significant earthquakes in Christchurch have brought the need for stability in the New Zealand insurance market into sharp focus. The ability of insurance companies to meet claims as they fall due has tremendous potential impact in such circumstances and the need for insurers to hold sufficient capi ...

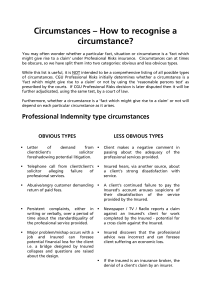

Circumstances – How to recognise a circumstance

... Circumstances – How to recognise a circumstance? You may often wonder whether a particular fact, situation or circumstance is a ‘fact which might give rise to a claim’ under Professional Risks insurance. Circumstances can at times be obscure, so we have split them into two categories: obvious and le ...

... Circumstances – How to recognise a circumstance? You may often wonder whether a particular fact, situation or circumstance is a ‘fact which might give rise to a claim’ under Professional Risks insurance. Circumstances can at times be obscure, so we have split them into two categories: obvious and le ...

Ethical Behaviour and Operating Performance of Insurance Broker

... plays a role of “market maker”, helping buyers to identify their coverage and risk management needs and matching buyers with appropriate insurers. In this case, although price is important, it is only one of several factors that clients consider when choosing which insurer(s) will provide their cove ...

... plays a role of “market maker”, helping buyers to identify their coverage and risk management needs and matching buyers with appropriate insurers. In this case, although price is important, it is only one of several factors that clients consider when choosing which insurer(s) will provide their cove ...

PDF

... and Coble,1997; Skees, Black and Barnett,1997; Goodwin and Smith,1995). To deal with these problems, a Group Risk Plan (GRP) was introduced in 1994, which pays a farmer an indemnity only when the realized average yield of his county falls below the pre-selected coverage level. Evaluation of county y ...

... and Coble,1997; Skees, Black and Barnett,1997; Goodwin and Smith,1995). To deal with these problems, a Group Risk Plan (GRP) was introduced in 1994, which pays a farmer an indemnity only when the realized average yield of his county falls below the pre-selected coverage level. Evaluation of county y ...

M05_REJDA_6117643_11_RMI_C05

... no stockholders, and the insurer does not issue assessable policies • An assessment mutual has the right to assess policyowners an additional amount if the insurer’s financial operations are unfavorable • A fraternal insurer is a mutual insurer that provides life and health insurance to members of a ...

... no stockholders, and the insurer does not issue assessable policies • An assessment mutual has the right to assess policyowners an additional amount if the insurer’s financial operations are unfavorable • A fraternal insurer is a mutual insurer that provides life and health insurance to members of a ...

ISSUE BRIEF - Partnership for New York City

... The 9/11 attack was another blow to an already struggling insurance industry. For the first time, annual net income for the U.S. property and casualty insurance industry fell below zero, a loss of $7.9 billion in 2001 (Hartwig, 2002a). Reinsurers, companies that assume a part of a risk policy from ...

... The 9/11 attack was another blow to an already struggling insurance industry. For the first time, annual net income for the U.S. property and casualty insurance industry fell below zero, a loss of $7.9 billion in 2001 (Hartwig, 2002a). Reinsurers, companies that assume a part of a risk policy from ...

INSURANCE

... In New York State, ambulance providers are mandatory first-responders. These emergency responders are often unaware if an individual has insurance coverage for emergency transport services or if they have the ability to pay out-of-pocket. Ambulance providers may inquire into the extent of insurance ...

... In New York State, ambulance providers are mandatory first-responders. These emergency responders are often unaware if an individual has insurance coverage for emergency transport services or if they have the ability to pay out-of-pocket. Ambulance providers may inquire into the extent of insurance ...

P6466 - iii Template

... of the Insurance Industry to U.S. GDP. In times of healthier economic growth, the industry contributes between 2.5% and 2.75% of U.S. GDP Sources: U.S. Department of Commerce, Bureau of Economic Analysis; Insurance Information Institute. ...

... of the Insurance Industry to U.S. GDP. In times of healthier economic growth, the industry contributes between 2.5% and 2.75% of U.S. GDP Sources: U.S. Department of Commerce, Bureau of Economic Analysis; Insurance Information Institute. ...

The role of insurance in Latin America | Zurich Government and

... fact, in 2010, the losses from natural disasters in Latin America relative to GDP exceeded the loss ratios in any other part of the world.9 The economic losses from natural disasters will most likely further increase in years to come, as a growing population and urbanization as well as growing wealt ...

... fact, in 2010, the losses from natural disasters in Latin America relative to GDP exceeded the loss ratios in any other part of the world.9 The economic losses from natural disasters will most likely further increase in years to come, as a growing population and urbanization as well as growing wealt ...

Advanced Topics in Risk Management

... Pure risks: handled by the risk manager through risk retention, risk transfer, and loss control. Speculative risks: handled by the finance division through contractual provisions and capital market instruments. Integrated risk program: a risk treatment technique that combines coverage for pure and s ...

... Pure risks: handled by the risk manager through risk retention, risk transfer, and loss control. Speculative risks: handled by the finance division through contractual provisions and capital market instruments. Integrated risk program: a risk treatment technique that combines coverage for pure and s ...

ImplementIng the natIonal Flood Insurance reForm act about the authors Howard Kunreuther, PhD

... Many communities in the U.S. have suffered recently from a series of disasters that have caused extensive damage and have been extremely costly. Following these catastrophes, insurance payments were historically high, as was the relief provided by the national government to state and municipal gover ...

... Many communities in the U.S. have suffered recently from a series of disasters that have caused extensive damage and have been extremely costly. Following these catastrophes, insurance payments were historically high, as was the relief provided by the national government to state and municipal gover ...

AIG - Rajeev Dhawan

... performance outpaces all major market indices and almost every major category of mutual fund. 66% of the industry’s invested assets are in bonds ...

... performance outpaces all major market indices and almost every major category of mutual fund. 66% of the industry’s invested assets are in bonds ...

uwio-101816 - Insurance Information Institute

... (40 of the 60 Years Before 1980 Had Combined Ratios Below 100) – But Then They Vanished. Not a Single Underwriting Profit Was Recorded in the 25 Years from 1979 Through 2003 * 2009 combined ratio excl. mort. and finl. guaranty insurers was 99.3, which would bring the 2000s total to 4 years with an u ...

... (40 of the 60 Years Before 1980 Had Combined Ratios Below 100) – But Then They Vanished. Not a Single Underwriting Profit Was Recorded in the 25 Years from 1979 Through 2003 * 2009 combined ratio excl. mort. and finl. guaranty insurers was 99.3, which would bring the 2000s total to 4 years with an u ...

Insurance

Insurance is the equitable transfer of the risk of a loss, from one entity to another in exchange for money. It is a form of risk management primarily used to hedge against the risk of a contingent, uncertain loss. An insurer, or insurance carrier, is selling the insurance; the insured, or policyholder, is the person or entity buying the insurance policy. The amount of money to be charged for a certain amount of insurance coverage is called the premium. Risk management, the practice of appraising and controlling risk, has evolved as a discrete field of study and practice.The transaction involves the insured assuming a guaranteed and known relatively small loss in the form of payment to the insurer in exchange for the insurer's promise to compensate (indemnity) the insured in the case of a financial (personal) loss. The insured receives a contract, called the insurance policy, which details the conditions and circumstances under which the insured will be financially compensated.