Recent Developments in Transferring Risk - mynl.com

... Retro guarantees crediting rate Retro earns spread: actual earnings over crediting rate LOC issues for non-admitted paper ...

... Retro guarantees crediting rate Retro earns spread: actual earnings over crediting rate LOC issues for non-admitted paper ...

I`m HIV positive, can I still purchase life insurance

... life insurer would never knowingly issue an individual life insurance policy to anyone who was HIV positive. Now, however, significant advances in the treatment of the virus make it possible for people who are HIV positive to obtain individual life insurance protection. While the opportunities for p ...

... life insurer would never knowingly issue an individual life insurance policy to anyone who was HIV positive. Now, however, significant advances in the treatment of the virus make it possible for people who are HIV positive to obtain individual life insurance protection. While the opportunities for p ...

LCQ1: Travel insurance agents

... Hong Kong, the main reason for some people to have passed the Travel Insurance Agents Examination but have not registered as travel insurance agents is that some experienced practitioners could not satisfy the requirement of having attained Form 5 education. In view of this, the Insurance Intermedia ...

... Hong Kong, the main reason for some people to have passed the Travel Insurance Agents Examination but have not registered as travel insurance agents is that some experienced practitioners could not satisfy the requirement of having attained Form 5 education. In view of this, the Insurance Intermedia ...

Novant Health, Inc. Basic Life Insurance

... If you are diagnosed as terminally ill with a 12 month life expectancy, you may be eligible to receive payment of a portion of your life insurance. The remaining amount of your life insurance would be paid to your beneficiary when you die. ...

... If you are diagnosed as terminally ill with a 12 month life expectancy, you may be eligible to receive payment of a portion of your life insurance. The remaining amount of your life insurance would be paid to your beneficiary when you die. ...

Equine-related Business Insurance

... To protect your equine business against the perils associated with the equine industry, we can provide you with tailored and competitively priced cover. For more information, please speak with one of our Equine Insurance Specialists on: ...

... To protect your equine business against the perils associated with the equine industry, we can provide you with tailored and competitively priced cover. For more information, please speak with one of our Equine Insurance Specialists on: ...

THE IMPACT OF NATURAL CATASTROPHES ... ON INSURERS

... transactions. Better risk sharing - which is critical - can be accomplished only through better risk transfer. On the other hand, contingent risk financing can be accomplished in a number of ways. For example, the ability to perform straight financing operations (through debt, equity, or any other i ...

... transactions. Better risk sharing - which is critical - can be accomplished only through better risk transfer. On the other hand, contingent risk financing can be accomplished in a number of ways. For example, the ability to perform straight financing operations (through debt, equity, or any other i ...

The Case For Tenant`s Insurance It is estimated

... In reality, tenant’s insurance is not very expensive. According to the Independent Insurance Agents and Brokers of America (IIABA), the average premium is $12 per month for $30,000 in property coverage, $6,000 in loss of use coverage, and $100,000 in liability coverage. Doesn’t the landlord cover me ...

... In reality, tenant’s insurance is not very expensive. According to the Independent Insurance Agents and Brokers of America (IIABA), the average premium is $12 per month for $30,000 in property coverage, $6,000 in loss of use coverage, and $100,000 in liability coverage. Doesn’t the landlord cover me ...

Life insurance: Ownership and investment considerations

... After a certain period of time, the income derived from these investments is sufficient to underwrite the premiums for the term insurance. As a result, the policy becomes self-funding. No additional premiums are paid in cash by the insured. The policy is effective for the entire life of the individu ...

... After a certain period of time, the income derived from these investments is sufficient to underwrite the premiums for the term insurance. As a result, the policy becomes self-funding. No additional premiums are paid in cash by the insured. The policy is effective for the entire life of the individu ...

Whole Life Insurance

... Term Insurance Advantages It is a low-cost option to provide for future insurability for a person whose future insurance needs may change. It allows people with lower incomes to purchase adequate amounts of immediate protection ...

... Term Insurance Advantages It is a low-cost option to provide for future insurability for a person whose future insurance needs may change. It allows people with lower incomes to purchase adequate amounts of immediate protection ...

The Essential Uninsured and Underinsured Motorist Coverage

... automobile insurance coverage. This means that if you are in an accident, there is a 25% chance that the other driver will have no insurance. To make matters worse, studies have shown that is economic downturns, many people let their auto insurance lapse, often by failing to pay the premiums. Theref ...

... automobile insurance coverage. This means that if you are in an accident, there is a 25% chance that the other driver will have no insurance. To make matters worse, studies have shown that is economic downturns, many people let their auto insurance lapse, often by failing to pay the premiums. Theref ...

Institute of Actuaries of India Subject CA3 – Communications INDICATIVE SOLUTION

... The above simulations need to capture how the various factors relate to each other with for example the rate at which policyholders are assumed to surrender often being linked to the prevailing economic conditions. It is very important to have this linkage in the case of policies which offer guarant ...

... The above simulations need to capture how the various factors relate to each other with for example the rate at which policyholders are assumed to surrender often being linked to the prevailing economic conditions. It is very important to have this linkage in the case of policies which offer guarant ...

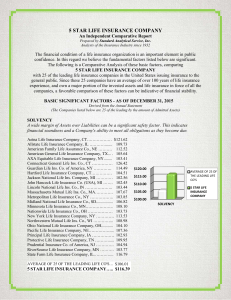

5 STAR LIFE INSURANCE COMPANY

... Standard Analytical Service, Inc. is independent of any insurance company or companies, and we do not sell any kind of insurance. Our financial reports and comparisons, reprints of which are paid for by the companies, are based on statutory financial statements filed with the state insurance departm ...

... Standard Analytical Service, Inc. is independent of any insurance company or companies, and we do not sell any kind of insurance. Our financial reports and comparisons, reprints of which are paid for by the companies, are based on statutory financial statements filed with the state insurance departm ...

history of insurance

... - Developed overtime by developments of England and other countries. CHRONOLOGICAL SEQUENCE OF EVENTS IN INDIAN INSURANCE SCENARIO 1818 – Oriental Life Insurance Company in Calcutta 1829 – Madras Equitable in Madras Presidency (life insurance) 1850 – Triton Insurance Company Ltd in Calcutta (G ...

... - Developed overtime by developments of England and other countries. CHRONOLOGICAL SEQUENCE OF EVENTS IN INDIAN INSURANCE SCENARIO 1818 – Oriental Life Insurance Company in Calcutta 1829 – Madras Equitable in Madras Presidency (life insurance) 1850 – Triton Insurance Company Ltd in Calcutta (G ...

Rising Awareness on NatCat - A Global Underwriter`s View

... Financial Analysis Module: Estimates of insured losses are then computed by applying policy conditions (eg, deductibles, limits) to the total loss estimates. ...

... Financial Analysis Module: Estimates of insured losses are then computed by applying policy conditions (eg, deductibles, limits) to the total loss estimates. ...

PROFIT REPORTING SEASON

... This information is directed and available to and for the benefit of Australian residents only and is not a recommendation or forecast. This information has been prepared without taking account of the objectives, needs, financial and taxation situation of any particular individual. For this reason, ...

... This information is directed and available to and for the benefit of Australian residents only and is not a recommendation or forecast. This information has been prepared without taking account of the objectives, needs, financial and taxation situation of any particular individual. For this reason, ...

11.07.2008 - Erste Bank Analysts: Outlook for insurance markets in

... addition, this cost will vary from region to region and European insurers should not be significantly hit, other than in the banking sector, where European banks are carrying some 52% of the total losses, amounting to USD 387. The main reason for this can be seen in the need for insurers to cover eu ...

... addition, this cost will vary from region to region and European insurers should not be significantly hit, other than in the banking sector, where European banks are carrying some 52% of the total losses, amounting to USD 387. The main reason for this can be seen in the need for insurers to cover eu ...

Homeowner`s Insurance Slideshow

... You may need to purchase additional coverage. This additional coverage is known as an endorsement Government may be able to provide coverage or emergency relief (FEMA) ...

... You may need to purchase additional coverage. This additional coverage is known as an endorsement Government may be able to provide coverage or emergency relief (FEMA) ...

fundamental principles of russian insurance contract law

... RUSSIAN LAW (dislosure of information) Requirement of disclosure of information on risks applied, but, as well as all over the world, courts are becoming more reluctant to view it as a must duty of the insurer the insured will only experience adverse effects if he intentionally concealed impor ...

... RUSSIAN LAW (dislosure of information) Requirement of disclosure of information on risks applied, but, as well as all over the world, courts are becoming more reluctant to view it as a must duty of the insurer the insured will only experience adverse effects if he intentionally concealed impor ...

Slide 0

... If history has proven one thing, it is that the insurance industry is extremely good at raising new capital after a crisis. In the 15 months following Hurricane Katrina, the insurance industry raised $33.7 billion in capital. When you consider that 60% of capital was raised over the first half of 20 ...

... If history has proven one thing, it is that the insurance industry is extremely good at raising new capital after a crisis. In the 15 months following Hurricane Katrina, the insurance industry raised $33.7 billion in capital. When you consider that 60% of capital was raised over the first half of 20 ...

An Overview to Client name - The University of the West Indies at

... ©Copyright 2007 Willis Limited all rights reserved. ...

... ©Copyright 2007 Willis Limited all rights reserved. ...

CPA Financial Literacy Mobilization Toolkit for Marriage

... • Discussed financial goals? • Who will handle money management? • Know partner’s money personality? ...

... • Discussed financial goals? • Who will handle money management? • Know partner’s money personality? ...

Global insurance regulation and systemic risk

... Financial crises of the 1990s (Mexico 1995, Asia 1997, LTCM 1998) marked turning point away from banks as sole causes of systemic risk ...

... Financial crises of the 1990s (Mexico 1995, Asia 1997, LTCM 1998) marked turning point away from banks as sole causes of systemic risk ...

FINA 406 ASSGN 1 ANSWERS

... Explain the difference between pure and speculative risk. Pure risk refers to possibilities that can result only in either loss or no change. Speculative risk refers to those exposures to price change that may result in either gain or loss. ...

... Explain the difference between pure and speculative risk. Pure risk refers to possibilities that can result only in either loss or no change. Speculative risk refers to those exposures to price change that may result in either gain or loss. ...

Title Insurance

... those so-called "non-record" defects that could not be discovered in the record, even with the most complete search. • Not only protects the insured owner, but also their heirs for as long as they hold title to the property, and even after they sell by warranty deed. • Not only satisfy any valid cla ...

... those so-called "non-record" defects that could not be discovered in the record, even with the most complete search. • Not only protects the insured owner, but also their heirs for as long as they hold title to the property, and even after they sell by warranty deed. • Not only satisfy any valid cla ...

Insurance

Insurance is the equitable transfer of the risk of a loss, from one entity to another in exchange for money. It is a form of risk management primarily used to hedge against the risk of a contingent, uncertain loss. An insurer, or insurance carrier, is selling the insurance; the insured, or policyholder, is the person or entity buying the insurance policy. The amount of money to be charged for a certain amount of insurance coverage is called the premium. Risk management, the practice of appraising and controlling risk, has evolved as a discrete field of study and practice.The transaction involves the insured assuming a guaranteed and known relatively small loss in the form of payment to the insurer in exchange for the insurer's promise to compensate (indemnity) the insured in the case of a financial (personal) loss. The insured receives a contract, called the insurance policy, which details the conditions and circumstances under which the insured will be financially compensated.