Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

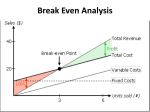

Break-Even Analysis Defined: Break-even analysis examines the cost tradeoffs associated with demand volume. Overview: Break-Even Analysis • • • • Benefits Defining Page Getting Started Break-even Analysis – Break-even point – Comparing variables • Algebraic Approach • Graphical Approach Benefits and Uses: • The evaluation to determine necessary levels of service or production to avoid loss. • Comparing different variables to determine best case scenario. Defining Page: • USP = Unit Selling Price • UVC = Unit Variable costs • FC = Fixed Costs • Q = Quantity of output units sold (and manufactured) Defining Page: Cont. • OI = Operating Income • TR = Total Revenue • TC = Total Cost • USP = Unit Selling Price Getting Started: • Determination of which equation method to use: – Basic equation – Contribution margin equation – Graphical display Break-even analysis: Break-even point • John sells a product for $10 and it cost $5 to produce (UVC) and has fixed cost (FC) of $25,000 per year • How much will he need to sell to break-even? • How much will he need to sell to make $1000? Algebraic approach: Basic equation Revenues – Variable cost – Fixed cost = OI (USP x Q) – (UVC x Q) – FC = OI $10Q - $5Q – $25,000 = $ 0.00 $5Q = $25,000 Q = 5,000 What quantity demand will earn $1,000? $10Q - $5Q - $25,000 = $ 1,000 $5Q = $26,000 Q = 5,200 Algebraic approach: Contribution Margin equation (USP – UVC) x Q = FC + OI Q= FC + OI UMC Q= $25,000 + 0 $5 Q= 5,000 What quantity needs sold to make $1,000? Q = $25,000 + $1,000 $5 Q = 5,200 Graphical analysis: Dollars 70,000 60,000 Total Cost Line 50,000 40,000 30,000 20,000 Total Revenue 10,000 Break-even point Line 0 1000 2000 3000 4000 5000 6000 Quantity Graphical analysis: Cont. Dollars 70,000 60,000 Total Cost Line 50,000 40,000 30,000 20,000 Total Revenue 10,000 Break-even point Line 0 1000 2000 3000 4000 5000 6000 Quantity Scenario 1: Break-even Analysis Simplified • When total revenue is equal to total cost the process is at the break-even point. TC = TR Break-even Analysis: Comparing different variables • Company XYZ has to choose between two machines to purchase. The selling price is $10 per unit. • Machine A: annual cost of $3000 with per unit cost (VC) of $5. • Machine B: annual cost of $8000 with per unit cost (VC) of $2. Break-even analysis: Comparative analysis Part 1 • Determine break-even point for Machine A and Machine B. • Where: V = FC SP - VC Break-even analysis: Part 1, Cont. Machine A: v = $3,000 $10 - $5 = 600 units Machine B: v = $8,000 $10 - $2 = 1000 units Part 1: Comparison • Compare the two results to determine minimum quantity sold. • Part 1 shows: – 600 units are the minimum. – Demand of 600 you would choose Machine A. Part 2: Comparison Finding point of indifference between Machine A and Machine B will give the quantity demand required to select Machine B over Machine A. Machine A FC + VC $3,000 + $5 Q $3Q Q = Machine B = FC + VC = $8,000 + $2Q = $5,000 = 1667 Part 2: Comparison Cont. • Knowing the point of indifference we will choose: • Machine A when quantity demanded is between 600 and 1667. • Machine B when quantity demanded exceeds 1667. Part 2: Comparison Graphically displayed Dollars 21,000 18,000 Machine A 15,000 12,000 9,000 Machine B 6,000 3,000 0 500 1000 1500 2000 2500 3000 Quantity Part 2: Comparison Graphically displayed Cont. Dollars 21,000 18,000 Machine A 15,000 12,000 9,000 Machine B 6,000 3,000 Point of indifference 0 500 1000 1500 2000 2500 3000 Quantity Exercise 1: • Company ABC sell widgets for $30 a unit. • Their fixed cost is$100,000 • Their variable cost is $10 per unit. • What is the break-even point using the basic algebraic approach? Exercise 1: Answer Revenues – Variable cost - Fixed cost = OI (USP x Q) – (UVC x Q) – FC $30Q - $10Q – $100,00 $20Q Q = = = = OI $ 0.00 $100,000 5,000 Exercise 2: • Company DEF has a choice of two machines to purchase. They both make the same product which sells for $10. • Machine A has FC of $5,000 and a per unit cost of $5. • Machine B has FC of $15,000 and a per unit cost of $1. • Under what conditions would you select Machine A? Exercise 2: Answer Step 1: Break-even analysis on both options. Machine A: v = $5,000 $10 - $5 = 1000 units Machine B: v = $15,000 $10 - $1 = 1667 units Exercise 2: Answer Cont. Machine A FC + VC $5,000 + $5 Q $4Q Q = Machine B = FC + VC = $15,000 + $1Q = $10,000 = 2500 • Machine A should be purchased if expected demand is between 1000 and 2500 units per year. Summary: • Break-even analysis can be an effective tool in determining the cost effectiveness of a product. • Required quantities to avoid loss. • Use as a comparison tool for making a decision. Bibliography: Russel, Roberta S., and Bernard W. Taylor III. Operations Management. Upper Saddle River, NJ: Pentice-Hall, 2000. Horngren, Charles T., George Foster, and Srikant M. Datar. Cost Account. 10th ed. Upper Saddle River, NJ: Pentice-Hall, 2000. EXERCISE • The company QUEENS is producing 5 different products(A,B, C,D, E). The total estimated revenues are given for A, B, C, D, E 180000, 200000, 395000, 500000,140000 TL respectively. The total estimated fixed costs are 538000 TL. • Unit prices and VC for products A, B, C, D and E are : PRODUCT Unit Price (TL) UVC(TL) A 235 120 B 150 63 C 425 195 D 175 68 E 420 210 •A)Calculate the percentage sales rate for each product • B) Calculate the ratio of UVC to the unit price for each product • C) Calculate the Break-even quantities and revenues for each product • D) If the income tax rate= 23%, and net income= 200000 TL, what should be the gross income and break even revenue Product Revenues S.Ratio (%) Unit Price UVC UVC/P Weighed % A 180.000 12.7 235 120 0.511 0.065 B 200.000 14.1 150 63 0.42 0.059 C 395.000 27.9 425 195 0.459 0.128 D 500.000 35.4 175 68 0.389 0.138 E 140.000 9.9 420 210 0.50 0.050 SUM 1.415.000 100.0 0.44 • BER= FC/ (1-UVC/P) • BER= 538.000/(1-0.44)=960.714 TL PRODU CT Sales percent Sales revenue Unit Price BEQ= R/P A 12,7 122.011 235 519 B 14,1 135.461 150 903 C 27,9 268.039 425 631 D 35,4 340.093 175 1943 E 9,9 95.110 420 226 • D) Tax rate=23% • Gross income= Net income/ (10.23)= 259.740 TL • BER for the company= (538.000 + 259.740)/ (1-0.44)=1.424.535 TL