Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

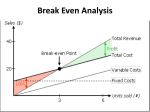

IB Business Management UNIT: 5.3 – Break-even Analysis pg. 642 Understand/practice break-even analysis & margin of safety Fixed or Variable? Direct or Indirect? • • • • • • • Rent Wages Salaries Materials Insurance Commission Utilities Breaking Even Business can be in one of the following financial situations: • Loss: costs exceeds revenue • Break-Even: costs equal revenue • Profit: revenue exceeds costs Breaking Even • Break-even point exists where a business makes neither profit nor loss • This occurs at the level of output where total costs equal total revenue • Typically a goal of new firms Contribution What is the purpose of calculating contribution? Unit contribution = P - AVC Any product w/ a positive contribution will help pay some of the FC of the company Contribution analysis gives 3 ways profits can be improved: Increase sales revenue Reduce VC Reduce FC Meaning of Break-Even Point • Total Costs = Total Revenue when output reaches the break-even point • Any sales above the break-even quantity will generate a profit • Sales below the break-even level will yield a loss Break-even Analysis A business can only survive in the long run if revenue > costs New firms especially want to determine the level of sales needed to generate a profit Break-Even Analysis Two purposes for conducting a breakeven analysis, which helps determine: • If its financially worthwhile to produce a particular good or service (such as introducing a new product) • Amount of profit that business is likely to earn if things go according to plan Break-Even Analysis Example • Jeans retailer has fixed costs of $2,500 per month • Each pair of jeans sells for $30 • $10 in variable costs per pair of jeans • What is the break-even point? Calculating Break-Even Point Method 1 Identify where total costs equal total revenue on a break-even chart • The break-even point is the position where the total cost line intersects the total revenue line (TC=TR) Calculating Break-Even Point Method 2 Using the TC = TR rule: • TFC + TVC = Price x Quantity • 2500 + 10(Q) = 30Q • 2500 = 20Q • 125 = Q (pairs of jeans) Calculating Break-Even Point Method 3 Unit contribution is difference between a product’s price and variable cost • Contribution = Price – VC • Break-Even Point = TFC / Unit Contribution $2500 = 125 pairs $30-10 Break-Even Example Use the unit contribution method to calculate the break-even quantity for a firm that has the following financials: • TFC = $200,000 • AVC = $5 • Price = $30 P - AVC = unit contribution Break-even = fixed costs unit contribution Margin of Safety Measures difference between firm’s current sales quantity & break-even point • Positive margin means that firm is making a profit • Always shown in units, not dollars! Safety margin = level of demand – breakeven qty. Margin of Safety Example • • • • Demand for jeans is 200 pairs per month Break-even point is 125 pairs per month Safety margin is 75 units (200-125 = 75) This means the business can sell 75 fewer pairs of jeans before losing money. Constructing a Break-even Chart Rules to follow when constructing BE chart: Draw/label TFC line Draw/label TC line. Q = 0; TC start at ??? Draw/label TR line. Q = 0; TR starts at ??? X-axis is labeled as “Output” or units Y-axis is labeled as “Costs, Revenues, Profit” $$$