Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

PROFESSOR AHMADI

PORTFOLIO THEORY

E X E R C I SE SE T

R E V I E W O F BA S I C

C O M PU TE R WO R K

CALIFORNIA STATE UNIVERSITY, SACRAMENTO

College of Business Administration

Write program in Excel to solve the following problems.

Use Excel built-in functions to solve the following problems

1. For the 10-year period, the holding period yields of stock (X) and the Stock Market are provided

below:

Year

Stock X

1

Stock Market

20.2

3.5

15.8

34.6

51.5

7.3

30.6

37.7

26.9

33.5

2

3

4

5

6

7

8

9

10

23.6

-7.2

6.4

18.2

31.5

14.8

20.4

22.5

26.0

27.9

a. Estimate the beta.

b. Write the equation of the Characteristic Line.

2. Suppose that you observe the returns to Stock J and to the market portfolio over 5 months and

that you see this:

Month

1

2

3

4

5

Stock J

Market Portfolio

2

3

6

-4

8

4

-2

8

-4

4

a. Find the beta for Stock J

b. Write the equation of the Characteristic Line

c. Find the variance of the estimated line (residual variance).

4. The following is the rate of return on the market, and the rate of return on the IBM

Find the “beta” of IBM and the standard deviation of IBM’s beta.

Sum:

Markets

IBM

11%

9

10

12

42

10%

10

12

14

46

stock.

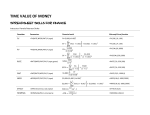

a. Practice Present Value with “Built-in Functions” in Excel

b. Find the corresponding “Financial Equation” for each “Function”

=PV(rate, nper, pmt, fv, type)

rate= interest rate per period; nper= total number of payment periods in an annuity

pmt= payment made each period; fv= present value

Type = 0 if payments are due the beginning of each period (can omit the 0 or enter) or 1 if payment is

due at the end of each period

Example 1: If you wanted to start a savings account that earns 6% annual interest, compounded

annually. How much would you have to deposit today (in a lump sum ), to have $5,000 in 5 years?

=PV(0.06, 5, 0, 5000)

($3,736.29)

If it is compounded semiannually the syntax will be:

=PV(0.06/2, 10, 0, 5000)

($3,720.47)

Example 2: (Present Value Annuity) How much is a bond that yields 8%, pays $90 for the next 14

years and $1,000 at the end of 14 years?

=PV(0.08, 14, 90, , 0)+PV(0.08, 14, , 1000)

($1,082.44)

TRY FUTURE VALUE FUNCTIONS AS WELL:

E.g.

. =FV(0.1,3,100)

=PMT(rate,nper,pv,fv,type)

rate=interest rate for the loan; nper=the total number of payments for the loan

pv=present value; fv=future value

type=0 indicates payments are due at the end of the period and 1 indicates payments are due at the

beginning of the period

Example 3: You take out a loan for $100,000 to buy a house. Mortgage rate is 12% a year, 30 years

fixed. What would monthly payments be?

=PMT(0.12/12, 30*12, 100000)

($1,028.61)

PPMT: Returns the payment on the principal for a given period

"=PPMT(rate, per, nper, pv, fv, type)"

rate=interest rate per period; per=specifies the period and must be in the range 1 to nper

nper= number of payment periods; pv=the present value; fv=the future value

type=0 if payment is at the end of each period(you can omit the 0 or enter it) or 1 if payment is at the

beginning of each period

Example 4: Use the PMT example above and find out the principal payment for the 1st period

"=PPMT(0.12/12, 1, 30*12, 100000)"

($28.61)

IPMT: Returns the interest payment for a given period for an investment

IPMT(rate, per, nper, pv, fv, type)

Example 5: Use the PMT example above and find the interest payment for the 1st period

"=IPMT(0.12/12, 1, 30*21, 100000)"

($1,000.00)

RATE

=RATE(nper, pmt, pv, fv, type, guess)

nper=the total number of pyment periods; pmt=the payment made each period

pv=the present value; fv=the future value

type=0 if payments are made at the end of each period or 1 if payments are made at the beginning of

each period.

Guess = is your guess for what the rate will be. If omitted guess will be assumed to be 10%

Example 6: You put $3,500 in a savings that is compounded semiannually and in 20 years you have

$11,417.13. What is the interest rate on that savings?

"=RATE(20*2, 0, -3500, 11417.13)"

3%

The annual interest rate will then be 3% X 2=6% since this account is compounded twice a year.

MIRR: Returns the Modified Internal Rate of Return for a series of periodic cash flows.

=MIRR(values, finance rate, reinvest rate)

values =an array of cells that contains the series of payments and incomes

finance rate =the interest rate you pay on the money used in the cash flows

reinvest rate =the interest rate you receive on the cash flows as you reinvest them

Example 7: Six months ago you opened a small hot dog stand by borrowing $8,000 at 10%. Each

month you manage to bring the following figures in profit and reinvest them in an account that earns

12% interest. What is your MIRR?

A

B

248

249

250

251

252

253

254

255

Month

0

1

2

3

4

5

6

Profit

-$8,000.00

$2,500.00

$3,500.00

$3,600.00

$4,200.00

$4,400.00

$5,000.00

=MIRR(B249:B255, 0.10, 0.12)

25%

IRR: Returns the internal rate of return for a series of cash flows

=IRR(values, guess)

values = an array of cells that contains the cash flows

guess = is your guess of what the IRR is (most of the time it can be omitted)

Example 8: Use the example for MIRR to find the IRR after the 4th month

"=IRR(B249:B253)"

24%

NPER: Returns the number of periods for an investment

=NPER(rate, pmt, pv, fv, type)

rate=the interest rate per period; pmt=the payment made each period

pv=the present value; fv=the future value

type=0 if payments are made at the end of each period or 1 if payments are made at the beginning of

each period

Example 9: If you decide to put $1,000 a month in an account that earns 12% interest a year, how

many periods will it take to earn $81,670?

=NPER(0.12/12, -1000, , 81670)

60.00018263

It will take approximately 60 periods or 60/12=5 years

NPV: Returns the net present value of an investment by using a discount rate and a series of

future payments and income.

"=NPV(rate, value1, value 2, ...)

rate=the rate of discount over the length of one period;

value 1, value 2, =represents payments and incomes

Example: Using the same example used for MIRR find the NPV

=NPV(0.10/12, 2500, 3500, 3600, 4200, 4400, 5000)+(-8000)

$14,474.37

DB: Returns the depreciation of an asset for a specified period

"=DB(cost, salvage, life, period, month)

cost=initial cost of the asset; salvage=value at the end of the depreciation

life= the number of periods over which the asset is being depreciated

period=period for which you want to calculate the depreciation

month=number of months in the first year

Example 10: A company buys a dump truck at $130,000 and in 10 years it is salvaged at $20,000. Show

the depreciation for the first 5 years

"=DB(130000, 20000, 10, 1, 12)" $22,230.00

"=DB(130000, 20000, 10, 2, 12)" $18,428.67

"=DB(130000, 20000, 10, 3, 12)" $15,277.37

"=DB(130000, 20000, 10, 4, 12)" $12,664.94

"=DB(130000, 20000, 10, 5, 12)" $10,499.23

DDB: Returns the depreciation of an asset for a specified period using the double-declining

balance method

=DDB(cost, salvage, life, period, factor)

cost=the initial cost of the asset

salvage=the value at the end of the depreciation

life=the number of periods over which the asset is being depreciated

period=the period for which you want to calculate the depreciation

factor=the rate at which the balance declines. 2 is for the double declining balance method

Example 11: Using the same example as the one used for DB, find the depreciation for the 1st month

and the first year

=DDB(130000, 20000, 120, 1, 2)

=DDB(130000, 20000, 10, 1, 2)"

$2,166.67

$26,000.00

SLN: Returns the straight line depreciation of an asset

=SLN(cost, salvage, life)

cost=the initial cost of an asset; salvage=the value at the end of the depreciation

life=the number of periods for which the asset is being depreciated

Example 12: Again using the example used in DB, find the depreciation allowance for each year.

=SLN(130000, 20000, 10)

$11,000.00

Find the depreciation allowance for each month

=SLN(130000, 20000, 120)

$916.67

POWER: Returns the result of a number raised to a power

=POWER(number, power)

Example 13: Find 1.08 raised to the power of 60

=POWER(1.08, 60)

101.2570637

PRODUCT: Multiplies numbers given

=PRODUCT(number 1, number 2, ...)

number 1, number 2=numbers you want to multiply

Example 14: Multiply the following numbers:

20, 30, 33, 44, 21

=PRODUCT(20, 30, 33, 44, 21) or =PRODUCT(A392:A396)

18295200

SQRT: Returns a positive square root

=SQRT(number)

or

=SQRT(A23)

Example 15: The standard deviation is equal to the square root of a variance. If the variance is 55 find

the standard variation using the SQRT function

=SQRT(55)

7.416198487

Average

"=Average(Number 1, Number 2....)

Example: Find the average of the following AT&T stock prices

49

51

58

49

56

"=Average(49,51,58,49,56)" or

"=Average(B55:B59)"

52.6

Note: Recognize that there is a difference between leaving a cell blank and entering a "0". If a cell is

left blank, it will be ignored. If a 0 is entered, it will be counted as a zero value.

Variance

=Var(Number 1,Number 2...)

Example: Find the variance to the AT&T stock prices listed above

"=Var(49,51,58,49,36)"

17.3

*Covariance

=Covar(array1, array2)

Example: Find the Covariance of IBM and AT&T using their stock prices listed below

IBM AT&T

100

49

95

51

98

58

113

49

115

56

"=Covar( {100,95,98,113,115}, {49,51,58,49,56} )" or

"=Covar(b82:b86, c82:c86)"

0.28

Standard Deviation

"=STDEV(number1,number2,....)"

Example: Use the numbers for AT&T above and find the standard deviation

"=STDEV(49,51,58,49,56)"or

"=STDEV(C82:C86)"

4.159326869

MMULT

=MMULT(Array 1,Array2)

Note: The number of columns in array 1 must be the same as the number of rows in array 2

Example: Multiply the two matrices below

B

C

D

E

F

108 0.1

-0.1

0.0

2 0

109 -0.1

0.4

0.3

0 2

110

0.0

0.3

0.7

0

G H

0

0

0 2

=MMULT(B108:D110,F108:H110)

and instead of pressing return press CTRL+SHIFT+RETURN

0.20

-0.2

0

-0.2

0.8

0.6

0

0.6

1.4

Make sure you highlight the complete array where the answers will show up. The result is an array with

the same number of rows as array 1 and the same number of columns as array 2

MINVERSE

=MINVERSE(Array)"

Example: Find the inverse Matrix of the matrix below:

0.2

-0.2

0

1

0.05

-0.2

0.8

0.6

1

0.07

0

0.6

1.4

1

0.3

1

1

1

0

0

0.05

0.07

0.3

0

0

Make sure you higlight a complete array with the same number of columns and rows when entering the

function

"=MINVERSE(B123:F127)" CTRL+SHIFT+RETURN

0.676990018

-0.735858715

0.058868697

0.789096493

-1.433324802

-0.735858715

0.799846429

-0.063987714

0.446634246

-2.789864346

0.058868697

-0.063987714

0.005119017

-0.23573074

4.223189148

0.789096493

0.446634246

-0.23573074

-0.094599437

0.522139749

-1.433324802

-2.789864346

4.223189148

0.522139749

-15.86895316

TRANSPOSE

This function changes rows into columns and the reverse

=Transpose(array)

then press CTRL+SHIFT+RETURN

Example: Change the following column of numbers to a row of numbers

Make sure you highlight the complete array when entering functions

"=Transpose(B145:B149)" then press CTRL+SHIFT+RETURN

1

2

3

4

5

1

2

3

4

5

Logarithms

=Ln(number)

Example: You start with $100, the rate is 8% and at the end of so many periods we get $158.69. How

many periods did it take to get $158.69?

$100(1+8%)to the power of n=$158.69

100(1.08)to the power of n=158.69

(1.08) to the power of n=1.5869

log(1.08) to the power of n=log (1.5869)

n log (1.08)=log (1.5869)

n=log(1.5869)/log(1.08)

"=ln(1.5869)/ln(1.08)"

6.000210246

It took 6 periods to get $158.69