Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

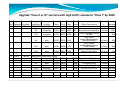

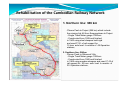

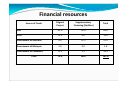

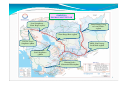

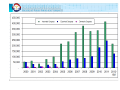

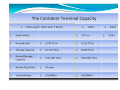

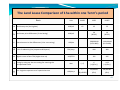

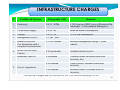

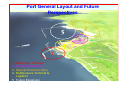

The Kingdom of Cambodia Ministry of Public Works and Transport Infrastructure Development and Transport Logistics Hong Sinara, DDG of Public Works /MPWT Suon Vanhong, DD of Transport/ MPWT 1 y Cambodia’s Economy y y y y y y Economic growth in Cambodia is slightly moderate in 2012, on the back of stronger garment and footwear exports, growing services and a more stable global economic outlook. The ADB paper showing that, the economic growth of Cambodia will moderate to 6.5% in 2012 from 6.8% in 2011, with a subsequent edging up to 7.0% in 2013. The projection assumes that the EU and the US economies – Cambodia’s main export markets – will continue their slow recovery, that the global outlook will not worsen significantly, and that the government of Cambodia will continue pursue policies that support growth. The expected slowdown in 2012 reflects falling industry exports with only slight increases in the growth of the services and agriculture sectors. Growth in industry driven by exports of garments and footwear to the US and the EU is projected to slow to 11.4% from 13.9% the year before. Services sector growth is expected to expand to 5.3% from 5.0%. Agriculture, which was disrupted by the flooding in late 2011, is forecast to grow by 3.8%, up from 3.3%, assuming favorable weather. But the picture looks brighter for 2013, with Cambodia tracking the expected upturn in the global economic outlook. In 2012, the fiscal deficit is targeted at 5.7% of GDP from 7.6% of GDP last year, to be achieved largely by an ambitious domestic revenue target of 13.7% of GDP. Government spending is budgeted at 19.4% of GDP in 2012. Due to the softening external demand, the current account deficit (excluding official transfers) is projected to widen to 7.6% of GDP in 2012, up from 7.1% of GDP in 2011, before narrowing a little in 2013 as the global economy picks up. Inflation in 2012 and 2013 is set to ease to about 5.0% on a year‐average basis, from 5.5% in 2011, assuming relatively low domestic financing of the budget deficit. However, rising global oil prices early in 2012 may put the inflation forecast at risk. (ADB, 11 April 2012) In October 10th,2012 the IMF raised its projection for Cambodia‘s GDP growth to 7.5 per cent in 2012. 2 I-CAMBODIA ROAD NETWORK Oddar Meanchey Ratanak Kiri Preah Vihear Banteay Meanchey Siem Reap Stung Treng Battambang Kampong Thom Pailin Pursat Kratie Kampong Chhnang Koh Kong Kampong Speu Kampong Cham Phnom Penh Kandal Takeo Sihanoukville Prey Veng Svay Rieng Kampot Kep 1-Digit Roads Mondul Kiri 2-Digit Roads Road density: 0.26km/km² Provincial Roads Rural roads Road Class Road Length (km) Paved road, km % 1-Digit Nationa l Road 2,258 2,115 94% 2-Digit Nationa l Road 3,342 1,868 56% 3&4Digit Provinci al Road 6,607 1,000 15% Rural Road 35,000 - - Total Length 47,207 4,983 11% Road Type Road length , km AC/DBST Pavement Percentage 1 Digit national roads: 1,2,3,4,5,6,7,8,9 2,258 2,115 94% 2 Digit national roads 3,342 1,868 56% Provincial roads 6,607 1,000 15% Rural roads 35,000 Total length 47,207 4,983 Road density : 0,26km/km² Gross Vehicle Weight: 25 T 4 5 Upgrade all “below Class III” sections of AH by 2012 Route No. Itinerary Total Length (Km) Poi Pet - Sisophon - Phnom Penh - Bavet Sihanoukville - Phnom Penh AH 11 -Kampong Cham - Stung Treng Trapeangkreal Cham Yeam - Koh Kong Phum Daung Bridge - Sre AH 123 Ambel AH 1 Chamkar Luong Total Length (Km) Primary Class I Class II 2008 2004 2008 2004 2008 2004 2008 2004 2008 2004 2008 2004 2008 575.0 573.0 - - - - - 573.0 575.0 - - - - - 770.0 762.8 - - - - 361.1 762.8 408.9 - - - - - 161.5 151 - - - - 10.5 - 11 151 140.1 - - - 1,506.5 0 1,486.80 - - - - 371.6 1,335.8 994.9 151.0 140.1 - - - Shares of the ASEAN Highways in Cambodia categorized by AH Design Standard in 2008 Class I Primary 0% 0% Primary 0% 0% Class I 0% Class II Below Class III Missing Links 2004 Shares of the ASEAN Highways in Cambodia categorized by AH Design Standard in 2004 Missing Links BelowIIIClass Class III Class III Below Class III 10% 0% Missing Links 25% 0% 9% Class III Class II 66% 90% Southern Corridor Improvement Projects Southern Corridor AH1 NR5 Upgrading Phnom Penh NR1 Improvement PP Ring Roads Expansion AH1 Neak Loeung Bridge Construction Upgrade “Class II or III” sections with high traffic volume to “Class I” by 2020 No. Highway Strategy length(Km) Activity Start 1 AH1 575km NR1(167km),NR5(408km) 2 AH11 30 on‐going 2012 2015 PRC NR5 337 on‐going 2011 2013 JICA NR5 68 plan 2013 2016 JICA 130 plan 2015 2018 JICA 139 plan 2014 2017 JICA 782km NR4(214km),NR6,NR7(570km) 40 on‐going 2012 2014 35 3 AH123 Resour rd.nu End ces mber 297km TOTAL: plan 2013 plan 2014 124 on‐going 2012 NR48(157km),NR3,33(40km) 1,486.8km 2016 2017 2015 Origin‐Destination No.lans e Remarks PhnomPenh‐PrekKdam 4 lanes study and construction of NR5 NR5‐north section(Battambang‐ 2‐4 lanes SereySophoan) NR5‐middle section(Battambang‐ 2‐4 lanes Thlea Maam) NR5‐south section(thlea 2‐4 lanes Maam‐Prek Kdam) PRC JICA JICA JICA JICA NR6 PhnomPenh‐Thnalkeng 4 lanes 32.30% (NB‐4km and PRC‐36km) NR6 Thnalkeng‐Skun 4 lanes NR7 Troeung‐TrapeingPlong NR4 PhnomPenh‐S'ville 3 lanessections Contents II‐Railway Development in Cambodia General Information y The Technical Assistance started in January 2006 and has been extended until January 31, 2011. y The Ministry of Public Works and Transport signed the contract of consultants’ services with CANARAIL Consultants Inc. to develop and strengthen the capacity of Railway Department. The consultants’ services are in progress. Rehabilitation of the Cambodian Railway Network 1. Northern line: 386 km -Phnom Penh to Poipet (386 km) which include the missing link 48 from Sereysophoan to Poipet. - Single Track Meter gauge 1000mm - Constructed from 1929 and finished in 1942 using steel sleepers bold rigid and used P 30 of rail support for 15 tons axle load. it consists of 49 Operation stations, 2. Southern line: 264km - Phnom Penh to Sihanouk Ville - Single Track Meter gauge 1000mm - Constructed from 1960 and finished in 1969 using wooden sleepers and used P 43 of rail support for 20 tons axle load. it consists of 29 Operation stations, ‐ ‐ ‐ ‐ On 18 February 2008, the Royal Government of Cambodia started to rehabilitate its railway networks in the total length of 650 km TSO (France) was a successful bidder for Rehabilitation Contraction. NIPPON KOEI ( Japan ) was a successful bidder of consultant for Construction supervision. The Project rehabilitation is to be completed in 2015 Ground breaking ceremony Financial resources Original Project Supplementary Financing ($million) Total ADB 42.0 42.0 84.0 OFID 13.0 0.0 13.0 Government of Australia 0.0 21.5 21.5 Government of Malaysia 2.8 0.0 2.8 Government of Cambodia 15.2 5.1 20.3 73.0 68.6 141.6 Source of Funds Total Rehabilitation Working Southern Line Southern Line 264 km (Phnom Penh – Sihanouk Ville) - Phase 1 : Phnom Penh – Touk Meas Station 120 km. This section was completed within September 2010. The rehabilitation is to be completed by end of December 2015 Railway Restructuring The Royal Government of Cambodia has Privatized and Signed Concession Agreement of 30 years with Toll Holding Co., Ltd. on 12, June 2009. The Royal Railway of Cambodia (RRC) was the state enterprise and terminated by sub decree of Royal government of Cambodia No.164 dated 01 October 2009. II- Railway Restructuring Toll Royal Railway In October 2010, the Toll Group and The Royal Group(Toll Royal Railway) has formed a joint venture to be responsible for Railway Concession. Toll Royal Railway began train operations on Southern line from Phnom Penh to Touk Meas station in length of 120 km on October 1, 2010. TRR has rehabilitated 10 French Alstom Locomotives and two Czech locomotives, with a further two Chinese locomotives currently available to meet operating requirements. Railway Development Plan in Cambodia Present Development Plan 1- SKRL Project 257 km from Bat Doeung – Vietnam Border 2- New Link from Serei Soaphoan - Siem Reap 105 Km. The feasibility study is undertaking by Yooshin Engineering Corporation Korea - Track Gauge : 1000 mm - Design Speed : 120 km/h 3- Master Plan for Railway Network Development in Cambodia is undertaking 3 years project by KOICA (Korea) 2011-2013. 4- New link from Preah Vihea Province to Kompot Province will be built by Chinese company. Now it is under study. CAMBODIA RAILWAY MASTER PLAN Serei Saophoan – Siem Reap: 105 km Snuol‐Stung Treng to Laos Border. 273km Siem Reap‐Skun 239km Poi Pet– Serei Saophoan 48km SKRL /Bat Doeng‐ Loch Ninh 257km Phnom Penh – Serei Saophoan 338km Phnom Penh – Sihanouk Ville 264km 19 III‐ Major Ports in Cambodia The main international ports in Cambodia are: 1. Phnom Penh Port on the Mekong river 2. Sihanouk ville Port on the Gulf of Thailand 20 Phnom Penh Port-SEZ (PPP-project) This Project is under Preparatory Survey by JICA. JICA shows strong support for conducting a Feasibility Study in 2013. Construction will start 2014. Location: at PK 30 along NR1, opposite side of current New Container Terminal. Area: approximately 250ha NR1 Present services y Container Terminal(Quay): 20m x 300m y Domestic Port: Phnom Penh, Kampong Cham, Siem Reap… y Passenger Terminal y ICD: 92, 000m2 y Warehouses: 70m x 50m = 3500m2 50m x 30m = 1500m2 Go to KAMSAB Phnom Penh Autonomous Port New Phnom Penh Port 23 River and Maritime Corridor Sihanoukville Port PPenh Port Cai Mep‐Thi Vai Port, VN Cargo throughput -PPAP (2000-2012,T) New Container Terminal of Phnom Penh Port - Location 25 km from PPenh in the lower Mekong river. Total cost 28 M USD (Chinese loan) Capacity:120,000 TEUs/Year, Max. capacity: 300,000 TEUs/year Berth : 22m x 300m Area: 12 ha Start operation 2012 Distance to Gateway Sea Ports from Phnom Penh Ho Chi Minh (Cai Mep – Thi Vai) Sihanoukville Laem Chabang 246 km Road No.1 430 km Inland Waterway 335 km Road No.1 380 km Inland Waterway 230 km Road No.4 690 km Road No.5 (410 km to Poipet) International Container Transportation Route Route 1: Sihanoukville Port (including surrounding private ports) Route 2: Phnom Penh Port (via the Mekong River and Ho Chi Minh Ports) Route 3: Vietnamese Border (Bavet) (via Ho Chi Minh Ports) Route 4: Thai Border (Poipet) (via Laem Chabang Port) Geographical Location of Sihanouk Ville Port • Sihanoukville Autonomous Port (PAS) is the sole international and commercial deep seaport of the Kingdom of Cambodia. • PAS is located at the bay of Kampong Som, Gulf of Thailand, South China Sea. • At present, the total operational land area is around 129.6 ha. 28 1. Navigational service MAIN SERVICES Quay Gantry Crane 2. Handling Service 3. Storage and Warehousing services 4. Security services 5. Special Economic Zone 6. Logistics Supply Base for offshore Oil exploration Tug boat Rubber Tired Gantry Crane Truck Reach Stacker S hore Crane 29 FACILITIES Equipment Capacity Units 30.50t 02 60t 02 35.5t 07 ‐ Super Stacker 45t 08 ‐ Empty Stacker 7.5t 01 ‐ Chassis/Trailer 20'‐40’ 33 ‐ Shore Crane 10‐50t 9 ‐ Truck for general cargo 10‐20t 08 ‐ Forklift 2‐25t 17 ‐ Quay Gantry Crane ‐ Mobile Harbor Crane ‐ RTG Navigational Facilities Tugboat 800 HP x 2 & 800 HP 03 & 02 Pilot boat 390 HP 01 Mooring boat 175 HP 01 210 HP x 2 01 Patrol boat Handling Productivities Container movement 25 boxes/hr‐QC General cargo 5 000 tons/day‐ berth 65.7 % ( 70%~) Average occupancy rate at new CT/week Average vessel’s dwell 25 hrs time at berth Vessel Capacity Called ~ 2 000 TEUs (<20 000 tons) 30 SECURITY EQUIPMENT - Vessel Traffic Management System (VTMS) - X- Ray Scanner - Patrol Boat 100HP - Oil Fence with 440 m long - Oil Skimmer - Oil Barge 100m³ - CCTV Cameras to be equipped with Alarms - ID PAS’s Card Entering System - Security Station Radiation Detector 1 set 1 set 1 Unit 1 set 1 Unit 1 Unit 25 Sets 5 Sets 2 Places 31 TRANSPORT NETWORKS : SEA,LAND&AIR CONNECTIONS TO PAS Sihanouk Ville Port is multi‐transport network connects to Hinterlands/ Consumption/Distribu tion Centre and to Neighboring Countries. 32 REGULAR SHIPPING LINES SCHEDULES AND CALLING PORT ROTATION Lines Calling Schedule Frequency RCL (3 calls/week) MAERSK (2 calls/week) 1. Wed 08:00 – Thu 16:00 2. Thu 14:00 – Fri 22:00 3. Fri 20:00 – Sat 23:59 1 call/week 1 call/week 1 call/week 1. Tue 15:00 – Wed 07:00 1 call/ week 2. Fri 1 call/ week 22:00 – Sun 00:01 Rotation Ports 1. SIN-SHV-SGZ-SIN 2. HKG-SHV-SGZ-HKG-(HPH-TXGKEL) 3. KUN-SHV-SGZ-SIN-KUN 1. SGN-SHV-LZP-TPP-SIN-BTG-MNLKAO-YAT-HKG-SGN 2. SIN-SHV-TPP-SIN SITC (BEN LINE) ( 1 call/week) Sun 09:00 – 23:00 1 call/week HCM-SHV-BKK-LZP-HCM-NSA-NBOSGH-OSA-KOB-BUS-SGH-HGK-HCM ITL (ACL) (1 call/week) Sat 06:00 – Sun 08:00 1 call/week SGZ-SHV-SIN-SGZ APL (1 call/week) Fri 08:00 – 1 call/week SIN-SHV-SIN Sun 06:00 COTS (1 call/2weeks) Remark s Total BKK : BangKok, Thailand KUN : Kuantan,Malaysia BUS : Busan, South Korea KEL BTG : Bantagas, Philippine LZP HKG : HongKong MNL : Keelung,Taiwan LaemChabang,Thailan : d : Manila, Philippine HPH : Hai Phong, Vietnam Ho Chi Minh, : Vietnam : Kobe Japan NSA NB O OSA HCM KOB 1 call/2 weeks (~3 Call / month) Mon 08:00 – 13:00 BKK-SHV-BKK- (LZP) Sihanoukville 9 Calls / week Port, SHV : Cambodia SGN : Saigon,Vietnam SIN : Singapore SGH : Shanghai, China : Nansha, China SGZ : Songkhla,Thailand : Ningbo, China TXG : Taichung,Taiwan : Osaka Japan TPP : Tanjung Pelepas Malaysia YA T : Yantian,China 33 Passenger Terminal Cruise Ships Year Vessel No. Passenger No. 2009 17 20,217 2010 17 24,261 2011 15 7,958 2012 (8 m.) 21 16,287 Cargo Statistics 110.02% 106.73% 106.73% 107.42% 109.37% 35 Cargo Statistics (Cont’) The Average Growth of the last three years (2009‐2011): ‐Gross Throughput 14.09%, and ‐Container Throughput 7% . BThe 2012 Prognoses: ‐Gross Throughput 2,850,000 tons, and ‐Container Throughput 260,000 TEUs. IMPORTS : Fuel, GC, Fabric, Steam coal, Constr. materials, Machinery, Clothing, Car, Cigarette, Vehicle. EXPORTS : Garment&Shoes, Rice, GC, Wood Processing, Cigarette, Rubber, Machinery, Aluminum, SeaFood, Medicine, Beer. 36 37 DEVELOPMENT PHASES 38 SEZ in Cambodia Poipet O’neag SEZ MDS THMORDA SEZ Thary K.Cham SEZ Neang Kok K.K SEZ Kirisakor Koh Kong SEZ Dragon King SEZ Oknha Mong SEZ Kompong Som SEZ in operation Sihanoukville SEZ1 under construction Sihanoukville SEZ2 Stung Hao SEZ S.N.C SEZ Sihanoukville Port SEZ Kampot SEZ no construction / 39 activity Comparison of Logistics Cost and Time Item Unit SPSEZ SSEZ PPSEZ Distance from PAS Km 1‐2 13 230 Trucking fee, 20ft USD 35 80 200 Customs clearance fee, 20ft USD 170 250 250 Total fees of 20ft USD 205 330 450 Total fee differences (Seal fee included) USD +125 +245 Number of day taken (Imp.) Day 1‐ 2 2‐5 Difference of day taken Day ½‐1 1 ½ ‐4 ½‐1 (5 days free storage imports) 40 The Land Lease Comparison of 1ha within one Term’s period Item Unit SPSEZ SSEZ PPSEZ 65 35 55 10 (65‐55) a Land lease price (the highest) USD/m2 b Land Lease price differences ( Price Saving) USD/m2 30 (65‐35) c _lease Amount in 1ha differences (1 ha cost saving) USD/ha 300,000.00 (b*10 000) d If Ann. Productivity/ ha (Imports and Exports) TEU/ha‐yr 400 400 e Logistics costs of one TEU (higher than us) USD/TEU 125 245 f Timing by using up the cost saving for covering the transportation costs g Ann. Logistics expenses as of a particular time 100,000.00 (b*10 000) Year (~ f) 6 ( c/(d*e) ) 1.02 ( c/(d*e) ) USD/ha‐yr f ~ Æ(+SPSEZ) 50,000.00 (d*e) 98,000.00 (d*e) 41 Rental Factory Site 6,731m2 42 LAND LEASE CONDITIONS Lease fee is a variable depending on lease space and period factors. *The prices range from USD 40/ m2 up to USD 65/ m2 20-year 30-year 40-year 50-year 10ha US$40 US$45 US$51 US$55 5ha US$44 US$49 US$56 US$61 2ha US$47 US$52 US$59 US$64 ~1ha US$48 US$53 US$60 US$65 Period (Land lease period is complied with new Civil Code of Royal Government of Cambodia that has taken effect on December 20, 2011) * The above fees are not inclusive of 10% withholding TAX . 43 INFRASTRUCTURE CHARGES Nº Facilities & Services Chargeable, USD Remarks 1 Electricity $ 0.33 / KWh A 10% top up of EDC prices (Electricite Du Cambodge – a Government Enterprise) 2 Clean water supply $ 0.30 / m3 Based on actual consumption 3 Sewage $ 0.35 / m3 80% of the consumption 4 Management service $ 1/ m2 / year 5 Rental Factory fee (An Estimation until a completed construction) $ 3.5/m2/month Included management charge, 2 years contract. 6 Office for rent (SEZ Centre) $ 15/m2/month Excluded electricity fees 7 Dormitory rent fee $ 60/month 6 workers/room, excluded water and electricity fees. $ 450/month Terrace House, excluded water and electricity $ 850/month Detached House, excluded water & electricity 8 Service Apartment * The above charges are not inclusive of VAT 10%, and withholding TAX 10% 44 Port General Layout and Future Perspectives 3 5 4 2 1 1. 2. 3. 4. Passenger Terminal Container Terminal Special Economic Zone Multipurpose Terminal & Logistics 5 Future Expansion 45 Thank You