Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

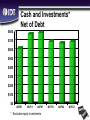

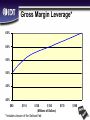

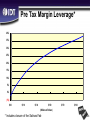

Solutions for Intelligent Bandwidth Forward-looking statements in this presentation involve a number of risks and uncertainties which are detailed in IDT’s SEC filings. Actual results may differ materially from the Company’s projections. 2 IDT is… • A global semiconductor solutions provider to leading-edge communications companies • Generating approximately 75% of revenues from communications and SAN markets • Financially strong and well-positioned as the market stabilizes and begins to grow 3 Prepared for Growth Resized the organization Dramatic reduction in discretionary spending Capital spending reduced Manufacturing consolidation announced $6-8 million savings per quarter RESULTS: 50% gross margin at $90 million in revenue Pro forma break-even at $90 million in revenue Cash flow break-even at $80 million in revenue High fall-through to profits with revenue growth 4 Serving The Communications Infrastructure Revenue Across All Products Calendar Q4 2001 Communications 19% Enterprise/Carrier-Class Wireless/Mobile Broadband Access Storage Area Networks 8% 3% 6% 46% 18% Personal Computing Miscellaneous 5 Leading Communications Customers • • • • • • Alcatel Cisco EMC Ericsson Fujitsu IBM • • • • • • Lucent Motorola NEC Nokia Nortel Siemens 6 The Changing Global Network Core Routing Voice Entridia Wireless Metro Router Enterprise OC-48c / 192c Metro Transport IP Broadband Access Core Metro ATM ATM Edge Router Core Router EDGE Metro Transport Metro Transport Metro Transport Edge Router ATM Core Switch OC-48c / 192c / 768 Web Switch SAN Fibre Channel Edge Aggregation 7 Key Growth Segments Application Segment Wireless Broadband Access Growth Rate High Core Routers Moderate Metro Edge Routers Moderate Multi-Service Access Switches Very High LAN Switch Ports Moderate VPN Equipment Moderate Web Switches Moderate Fibre Channel SAN High Source: Gartner Dataquest & IDT, December 2001 8 Intelligent Bandwidth Throughput OC-768 40 Gbps Major performance increase needed to service wire-speed throughput and deeper classification 10 Mbit Layer 3 Classification Layer 3-7 9 Key Market Drivers • Faster, more intelligent packet processing • The convergence of data and voice • Distributed intelligence throughout the network 10 IDT’s Increasing Integration Integrated System Technology Integration of Memory & Logic Blocks of Intellectual Property Development Platforms 11 Strengthening Solutions Focus • Residential gateway reference designs • Alcatel, Wind River (high-end), Jungo (low-end) • Managed LAN switch reference design • Broadcom, Wind River • Voice access solution • Intersil • High performance packet processing/classification • AMCC – integrated interface to NPU • Solidum – classification processing solution • Xelerated Packet Devices – joint solution 12 Products for Communications Communications ASSPs IP Co-Processors Integrated Processors Telecom Products FIFOs Multi-Ports Clock Management Digital Logic SRAMs 13 Product Execution • 2001 – Most prolific year for new products in IDT history • Continued to deliver leadership products in traditional businesses • New business opportunities represent over $1 billion in new TAM • Strong design activity mitigated by: – Timing of new system ramps – Competing/cancelled projects 14 Our Communications Foundation #1 Market Share – FIFOs #1 Market Share – Multi-ports #1 Market Share – FCT Digital Logic #1 Market Share – Bus Switches #2 Market share – ALVC/LVC Digital Logic A growing portfolio of clock generators, clock distribution and clock buffering products. These products represent more than 60% of IDT’s revenues Source: Insite/Onsite & IDT estimates 15 IP Co-Processors • Faster, more intelligent packet processing required for >OC-48 emerging market segment • Accelerates deep packet classification and highspeed packet forwarding, working with ASICs or NPUs • Integration of CAM (content addressable memory) with high-performance logic – core competence of IDT 16 IP Co-Processor Benefits • High performance – Portfolio of 2 Mbit to 18 Mbit devices – Up to 4 million entries at 200 MSPS* – Wide-width searches - up to 576 bits • Advanced database support – Multiple databases allowing for integration of services • Significant power savings – Up to 60% savings over traditional approaches • Quick time to market – Software driver support – Pin-compatible family (2 Mbit - 9 Mbit) • Strategic partnerships for easier integration * MSPS – millions of searches per second 17 IP Co-Processor Update • Cisco-specific IP co-processor ramping – Inventory depleted – New programs beginning to ramp • Major announcements for commercial products – Shipping fastest, full-featured products in production – Roadmap to 200 MSPS, 1 million entry – 2nd half CY02 – Roadmap to integrated IP co-processors for major NPUs – summer CY02 • Current design activity will drive late CY02 revenue for commercial products 18 Telecom Products • Address the convergence of data and voice • Industry-leading position in TSI switching, voice processing, transport, roadmap to HDLC control – The addition of mixed-signal/voice expertise complements IDT competencies in data systems – June 2001 - introduced the industry’s first octal CODEC, capable of 8 voice channels – November 2001 - introduced octal T1/E1/J1 line interface unit (LIU) and octal T1/E1/J1 framer • IDT’s goal is to be the broadest provider of telecom semiconductors in the market by 2005 19 Integrated Processors • Provide distributed intelligence across network • Blend industry-standard IP modules with differentiated, value-added proprietary IP • Utilize MIPS architecture CPU core • Partner to supply complementary hardware and software technology for complete solutions to specific applications • 3 out of top 5 managed LAN switch vendors use IDT RC32332 integrated processor 20 Financials Revenue From Operations $300 $250 $269 $279 $ Millions $213 $200 $150 $116 $97 $80 $100 $50 $0 Q2F01 Q3F01 Q4F01 Q1F02 Q2F02 Q3F02 22 Earnings Per Share $1.00 $0.90 $0.80 $0.70 $0.60 $0.50 $0.40 $0.30 $0.20 $0.10 $0.00 -$0.10 $0.87 (Excludes special items) $0.77 $0.51 Q2F01 Q3F01 Q4F01 $0.00 -$0.05 Q1F02 Q2F02 $-0.11 Q3F02 23 Cash and Investments* Net of Debt $800 $700 $600 $500 $400 $300 $200 $100 $0 Q2F01 Q3F01 Q4F01 * Excludes equity investments Q1F02 Q2F02 Q3F02 24 Gross Margin Leverage* 65% 60% 55% 50% 45% 40% $90 $110 $130 $150 (Millions of Dollars) * Includes closure of the Salinas Fab $170 $190 25 Pre Tax Margin Leverage* 40% 35% 30% 25% 20% 15% 10% 5% 0% (5%) $90 $110 $130 $150 $170 $190 (Millions of Dollars) * Includes closure of the Salinas Fab 26 IDT Delivers Value • IDT delivers innovative communications IC solutions to maximize the use of bandwidth in the converging global network – A strong foundation of products for communications – A growing portfolio of leadership products for • Packet classification – IP co-processors • Voice/data convergence – telecom products • Distributed Intelligence – integrated processors • IDT has held costs in check while continuing to execute new products during the downturn • IDT has a business model that is poised to perform well as the market recovers 27 Thank You