Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

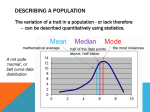

Chapter Outline 3.1 THE PERVASIVENESS OF RISK Risks Faced by an Automobile Manufacturer Risks Faced by Students 3.2 BASIC CONCEPTS FROM PROBABILITY AND STATISTICS Random Variables and Probability Distributions Characteristics of Probability Distributions Expected Value Variance and Standard Deviation Sample Mean and Sample Standard Deviation Skewness Correlation 3.3 RISK REDUCTION THROUGH POOLING INDEPENDENT LOSSES 3.4 POOLING ARRANGEMENTS WITH CORRELATED LOSSES Other Examples of Diversification 3.5 SUMMARY Appendix Outline APPENDIX: MORE ON RISK MEASUREMENT AND RISK REDUCTION The Concept of Covariance and More about Correlation Expected Value and Standard Deviation of Combinations of Random Variables Expected Value of a Constant times a Random Variable Standard Deviation and Variance of a Constant times a Random Variable Expected Value of a Sum of Random Variables Variance and Standard Deviation of the Average of Homogeneous Random Variables Probability Distributions Probability distributions – Listing of all possible outcomes and their associated probabilities – Sum of the probabilities must ________ – Two types of distributions: discrete continuous Presenting Probability Distributions Two ways of presenting discrete distributions: – Numerical listing of outcomes and probabilities – Graphically Two ways of presenting continuous distributions: – Density function (not used in this course) – Graphically Example of a Discrete Probability Distribution Random variable = damage from auto accidents Possible Outcomes for Damages $0 $200 $1,000 $5,000 $10,000 Probability Example of a Discrete Probability Distribution 1 Probability 0.8 0.6 0.4 0.2 0 0 200 1000 Dam ages 5000 10000 Example of a Continuous Probability Distribution Probability Probability Distribution for Auto Maker's Profits -20,000 0 20,000 Profits 40,000 Continuous Distributions Important characteristic – Area under the entire curve equals ____ – Area under the curve between ___ points gives the probability of outcomes falling within that given range Probabilities with Continuous Distributions Find the probability that the loss > $______ Find the probability that the loss < $______ Find the probability that $2,000 < loss < $5,000 Probability $2,000 $5,000 Possible Losses Expected Value – Formula for a discrete distribution: Expected Value = x1 p1 + x2 p2 + … + xM pM . – Example: Possible Outcomes for Damages $0 $200 $1,000 $5,000 $10,000 Expected Value = Probability Product Expected Value Comparing the Expected Values of Two Distributions Visually A Probability B 0 3000 6000 9000 12000 Outcomes 15000 18000 21000 Standard Deviation and Variance – Standard deviation indicates the expected magnitude of the error from using the expected value as a predictor of the outcome – Variance = – Standard deviation (variance) is higher when Standard Deviation and Variance – Comparing standard deviation for three discrete distributions Distribution 1 Distribution 2 Distribution 3 Outcome Prob $250 0.33 _____ ____ $750 0.33 Outcome Prob $0 0.33 _____ ____ $1000 0.33 Outcome Prob $0 0.4 _____ ___ $1000 0.4 Standard Deviation and Variance Comparing the Standard Deviations of two Distributions Probability A B 0 500 1000 1500 Outcomes 2000 2500 Sample Mean and Standard Deviation – Sample mean and standard deviation can and usually will differ from population expected value and standard deviation – Coin flipping example $1 if heads X= -$1 if tails Expected average gain from game = $0 Actual average gain from playing the game ___ times = Skewness Skewness measures the symmetry of the distribution – No skewness ==> symmetric – Most loss distributions exhibit ________ Loss Forecasting: Component Approach Estimating the Annual Claim Distribution Historical Claims Frequency Historical Claims Severity Loss Development Adjustment Inflation Adjustment Exposure Unit Adjustment Frequency Probability Distribution Severity Probability Distribution --------- Claim Distribution Annual Claims are shared: Firm Retains a Portion Transfers the Rest Firm’s Loss Forecast Premium for Losses Transferred Loss Payment Pattern Premium Payment Pattern Mean and Variance impact on e.p.s. Slip and Fall Claims at Well-Known Food Chain Exposure Base: $ or Footage Claims Cost Price Index: Adjusted No. Currrent of Claims Year = 100 Year Raw Claim Data by Size ($) Number of Claims 1988 - 0 1,000,000 0 32.60 1989 460.00 1 1,000,000 2 35.20 1990 590.00 2 1,000,000 4 37.90 0 1,000,000 0 40.80 1 1,000,000 2 44.00 520.00 1991 1992 200.00 1993 - 0 1,000,000 0 47.40 1994 - 0 2,000,000 0 51.10 1 2,000,000 1 55.00 0 2,000,000 0 59.30 3 2,000,000 3 63.90 0 2,000,000 0 68.90 1995 1996 1997 775.00 830.00 905.00 670.00 1998 - 1999 1,080.00 1 2,000,000 1 74.20 2000 590.00 2 2,000,000 2 79.90 340.00 2001 - 0 2,000,000 0 86.10 2002 - 0 2,000,000 0 100.00 Unadjusted Frequency Distribution Number of Claims 0 1 2 3 Probability of Claim .5333 _____ .1333 .0667 Cumulative Probability 1.0000 Unadjusted Frequency Distribution 0.6 Probability 0.5 0.4 0.3 0.2 0.1 0 0 1 2 Number of Claims 3 Unadjusted Severity Distribution Interval in Dollars 200-375 ___-___ 551-725 726-900 900-1100 Relative Frequency .1818 .1818 .2727 _____ .0910 Cumulative Probability 1.0000 Severity Distribution 0.3 Probability 0.25 0.2 0.15 0.1 0.05 0 200-375 376-550 551-725 726-900 901-1100 Annual Claim Distribution Combine the _______ and ______ distributions to obtain the annual claim distribution Sometimes this can be done mathematically Usually it must be done using “brute force” statistical procedures. An example of this follows. Frequency Distribution Number of Claims 0 1 2 3 Probability of Claim .1 .6 .25 .05 Severity Distribution Prob. Amount of Loss Midpoint of Loss $0 to 2,001 to 8,001 to 12,001 to 88,001 to GT 312,000 $2,000 $1,000 8,000 5,000 12,000 10,000 88,000 50,000 312,000 200,000 500,000 .2 ___ ___ .06 .03 .01 Cum. Prob. .2 ____ ____ .96 .99 1.00 Annual Claim Distribution Claim Amount 1 2,001 8,001 12,001 70,001 450,001 GT $0 to 2,000 to 8,000 to 12,000 to 70,000 to 450,000 to 511,000 511,000 Cumulative Probability .1 .13 _____ .2566 .17984 .038299 _______ .001241 .1 .23 _____ .7694 .94924 .987539 .998759 1.000000 ________ ________ Loss when applied to: – severity distribution – annual claim distribution Loss Forecasting Aggregate Approach Estimating the Annual Claim Distribution Annual Claims: Raw Figures Loss Development Adjustment Inflation Adjustment Exposure Unit Adjustment Annual Claim Distribution Loss Forecasting Aggregate Approach Annual Claims are shared: Firm Retains a Portion Transfers the Rest Firm’s Loss Forecast Premium for Losses Transferred Loss Payment Pattern Premium Payment Pattern Mean and Variance impact on e.p.s.