Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

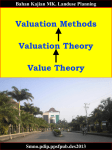

Er. Gurbakshish Singh Antal Lect Civil Engg. Property valuation Valuation Methods Need of Valuation Value Theory Valuation is both a Science and an Art! Valuation is both a Science and an Art! Valuation includes components and knowledge of: -mathematics -statistics -physical (land) planning -urban planning -rural planning/agriculture Valuation components › -building construction › -sociology/human behaviour › -common sense/feeling Valuation is the technique of estimating and determining the fair price or value of a property such as a building, a factory or other engineering structures of various types, land etc. Valuation of a building depends on •type of the building, •building structure and durability, •on the situation, •Size of building, •Shape of building, •Frontage of building, width of roadways, the quality of materials used in the construction present day prices of materials The valuation of a building is determined on working out its cost of construction at present day rate and allowing a suitable depreciation. 1.Buying or Selling Property When it is required to buy or sell a property, its valuation is required. 2.Taxation To assess the tax of a property, its valuation is required. Taxes may be municipal tax, wealth tax, Property tax etc, and all the taxes are fixed on the valuation of the property. 3.Rent Function In order to determine the rent of a property, valuation is required. Rent is usually fixed on the certain percentage of the amount of valuation which is 6% to 10% of valuation. 4.Security of loans or Mortgage When loans are taken against the security of the property, its valuation is required. 5.Compulsory acquisition Whenever a property is acquired by law; compensation is paid to the owner. To determine the amount of compensation, valuation of the property is required. 6.Insurance,Betterment charges, speculations Valuation of a property is also required for Insurance,Betterment charges, speculations etc. Information needed • Information about the property: – Land use – Land area – Building: size, age, standard etc. – Yearly costs and incomes – Other special conditions Information needed • Information about the purchase Seller : Mr A Buyer : Mrs B Date: 04-09-15 Price: 1 200 000 etc. – Price – Date of sale – Seller – Buyer • Information about the real property – – – – Land use Land area Building: size, age, standard etc. Other special conditions Information needed • General information – Average replacement costs – Depreciation - time and percent – Average value of land • Information about the real property – Land use – Land area – Building: size, age, standard etc. – Other special conditions The cost approach SEK/ USD Replacement costs Depreciation 3.5 %/year Cost of land 0 Cost value Age (years) 10 Replacement costs Depreciation 10 years 3,5 % Cost of land Cost value 1 000 - 350 200 850 Market value Scrap value Salvage value Liquidation value Insurable value Book Value The market value of a property is the amount which can be obtained at any particular time from the open market if the property is put for sale. The market value will differ from time to time according to demand and supply. The market value also changes from time to time for various miscellaneous reasons such as changes in industry, changes in fashions, means of transport, cost of materials and labour etc. Scrap value may be defined as the value of materials of dismantle buildings. After the completion of utility period the dismantled materials such as Steel, timber ,bricks and furniture will fetch a certain amount which is called scrap value of building. Scrap value of building is about 10 % of its total cost of construction. - The value of building at the end of utility period without being dismantled is called the Salvage Value. Another example is a machine after the completion of its usual span of life , may be sold or purchased by some one for other use. The sale value of that machine is called Salvage value. Salvage value of a property or an asset may be positive, zero or negative. For example the salvage value of RCC structures is negative ,because dismantling and removal will be costly. Scrap value of machine is Positive because it will be used for other purpose. Liquidation Value Book value is the amount shown in the account book after allowing necessary depreciations. The book value of a property at a particular year is the original cost minus the amount of depreciation allowed per year and will be gradually reduced year to year and at the end of the utility period of the property, the book value will be only scrap value. Sinking Fund may be defined as the fund which is gradually accumulated by way of periodic on account deposit for the replacement of building or structure at the end of its useful life. Main function of creating Sinking fund is to accumulate sufficient to meet the cost of construction or maintenance or replacement of structure after its utility period. Depreciation is the gradual exhaustion of the usefulness of a property. This may be defined as the decrease or loss in the value of a property due to structural deterioration, life wear and tear, decay and obsolescence. HKSSAP defines depreciation as the ‘allocation of the depreciable amount of an asset over its estimated life’. Rateable Value is net annual letting value of a property , which is obtainable after deducting the amount of yearly repairs from gross income. Municipal and other taxes are charged at a certain percentage on the rateable value. Obsolescence is defined as the overall decrease in the value of property or structure due to becoming outdate in style, in structure or in design. i.e an old dated building with massive walls, arrangement of rooms not suited in present days becomes obsolete even iif it is well maintained. Progress in Art New invention Change in Fashion Improvement in Design Change in planning idea New trends in Market Inadequate Space Annuity is the annual periodic payments for repayment of the capital amount invested by the party. These payments are either paid at the end of year or at the start of year. Capital cost is the total cost of construction including land, or the original total amount required to possess a property. It is the original cost and does not change while the value of the property is the present cost which may be calculated by methods of Valuation. The capitalized value of a property is the amount of money whose annual interest at the highest prevailing rate of interest will be equal to the net income from the property. To determine the capitalized value of a property, it is required to know the net income from the property and the highest prevailing rate of interest. Capitalized Value = Net income x year’s purchase Year’s purchase is defined as the capital sum required to be invested in order to receive a net receive a net annual income as an annuity of rupee one at a fixed rate of interest. The capital sum should be 1×100/rate of interest. Thus to gain an annual income of Rs x at a fixed rate of interest, the capital sum should be x(100/rate of interest). But (100/rate of interest) is termed as Year’s Purchase. Area where Property Situated Present Cost of Material Heritage value of Building Condition of scrap Land value Gross income On situation Road width frontage He must know the deep knowledge of the concerned field or subject area. He must posses Analytical and Computer Skills. He should know the tolerances for wastage incurred during construction. He should be know the Present rates of material used. He should be well experienced He should know the bye laws of that area. He should posses the leadership and soft skills. He must know the deep knowledge about the latest materials and their cost. Rental Method of Valuation Direct comparison with the capital Value Valuation based on profit Valuation based on cost Depreciation Method In this method, the net income by way of rent is found out by deducting all outgoing from the gross rent. A suitable rate of interest as prevailing in the market is assumed and Year’s purchase is calculated. This net income multiplied by Year’s Purchase gives the capitalized value or valuation of the property. This method is applicable only when the rent is known or probable rent is determined by enquiries. This method may be adopted when the rental value is not available from the property concerned, but there are evidences of sale price of properties as a whole. In such cases, the capitalized value of the property is fixed by direct comparison with capitalized value of similar property in the locality. This method of Valuation is suitable for buildings like hotels, cinemas, theatres etc for which the capitalized value depends on the profit. In such cases, the net income is worked out after deducting gross income; all possible working expense, outgoings, interest on the capital invested etc. The net profit is multiplied by Year’s Purchase to get the capitalized value. In such cases, the valuation may work out to be high in comparison with the cost of construction. In this method, the actual cost incurred in constructing the building or in possessing the property is taken as basis to determine the value of property. In such cases, necessary depreciation should be allowed and the points of obsolescence should also be considered. Walls Roofs Floors Doors and Windows And the cost of each part should first be worked out on the present day rates by detailed measurements. The present value of land and water supply, electric and sanitary fittings etc should be added to the valuation of the building to arrive at total valuation of the property. [email protected]