Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

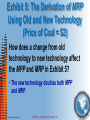

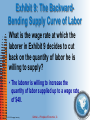

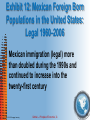

Chapter 15 WAGE RATES IN COMPETITIVE LABOR MARKETS © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 1 Economic Principles Marginal physical product of labor Marginal revenue product The law of diminishing returns Marginal labor cost The profit-maximizing level of employment © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 2 Economic Principles Firm and industry demand for labor The supply of labor The backward-bending supply curve of labor Wage differentials Minimum wage laws © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 3 You Load Sixteen Tons and What Do You Get? Marginal physical product (MPP) • The change in output that results from adding one more unit of a resource, such as labor, to production. MPP is expressed in physical units, such as tons of coal, bushels of wheat, or number of automobiles. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 4 You Load Sixteen Tons and What Do You Get? Marginal physical product (MPP) • MPP = change in output (Q) divided by change in the number of people employed (L). © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 5 You Load Sixteen Tons and What Do You Get? Marginal physical product (MPP) • Any change in MPP is attributed to the hiring of one additional employee. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 6 EXHIBIT 1A OUTPUT AND MARGINAL PHYSICAL PRODUCT CURVES © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 7 EXHIBIT 1B OUTPUT AND MARGINAL PHYSICAL PRODUCT CURVES © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 8 Exhibit 1: Output and Marginal Physical Product Curves 1. How can the shape of the total output curve in panel a of Exhibit 1 be described? • The total output curve is upward sloping, increasing by large amounts until three miners are employed, then increasing by smaller and smaller amounts when more than three miners are employed. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 9 Exhibit 1: Output and Marginal Physical Product Curves 2. Why does the MPP curve in panel b climb to a peak and then fall? • The MPP curve maps the increases noted in the total output curve. The MPP increases for the first three miners, then falls as more miners are added to production. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 10 You Load Sixteen Tons and What Do You Get? Law of diminishing returns • As more and more units of one factor of production are added to the production process while other factors remain unchanged, output will increase, but by smaller and smaller increments. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 11 You Load Sixteen Tons and What Do You Get? Law of diminishing returns • Adding more labor to a given stock of physical capital must eventually create a less-thanefficient match of labor to capital. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 12 You Load Sixteen Tons and What Do You Get? Law of diminishing returns • The law is demonstrated in the eventual flattening of the total output curve and the negative slope of the MPP curve. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 13 You Load Sixteen Tons and What Do You Get? Marginal revenue product (MRP) • The change in total revenue that results from adding one more unit of a resource, such as labor, to production. MRP, which is expressed in dollars, is equal to MPP multiplied by the price of the good. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 14 You Load Sixteen Tons and What Do You Get? Marginal revenue product • MRP = MPP × price or • MRP = change in total revenue (TR) divided by change in labor (L) © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 15 Deriving the Firm’s Demand for Labor The quantity of labor demanded depends on price. If the price of labor falls, the quantity demanded of labor increases. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 16 Deriving the Firm’s Demand for Labor Wage rate • The price of labor. Typically, the wage rate is calculated in dollars per hour. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 17 Deriving the Firm’s Demand for Labor Total labor cost (TLC) • Quantity of labor employed (L) multiplied by the wage rate (W). • TLC = L × W © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 18 Deriving the Firm’s Demand for Labor Marginal labor cost (MLC) • The change in a firm’s total cost that results from adding one more worker to production. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 19 Deriving the Firm’s Demand for Labor Marginal labor cost (MLC) • MLC = change in TLC divided by change in L. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 20 EXHIBIT 2A DERIVING THE MARGINAL LABOR COST CURVE © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 21 EXHIBIT 2B DERIVING THE MARGINAL LABOR COST CURVE © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 22 Exhibit 2: Deriving the Marginal Labor Cost Curve What causes the MLC curve to be horizontal in panel b of Exhibit 2? • The labor market is perfectly competitive. Individual firms cannot influence the wage rate. The firm can hire as many workers as it wants at the prevailing wage rate. MLC is equal to the wage rate. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 23 Deriving the Firm’s Demand for Labor The hiring rule for firms: • Compare marginal revenue product and wage rate and hire laborers until MRP = W. • If MRP > W, hire more laborers. • If MRP < W, don’t hire. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 24 EXHIBIT 3 © 2013 Cengage Learning THE DEMAND FOR LABOR Gottheil — Principles of Economics, 7e 25 Exhibit 3: The Demand for Labor Why is a firm’s demand for labor equal to marginal revenue product (MRP)? • MRP reflects the maximum a firm is willing to pay for an additional unit of labor. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 26 Exhibit 3: The Demand for Labor Why is a firm’s demand for labor equal to marginal revenue product (MRP)? • When the price of labor falls, firms can afford to hire more labor, even though MRP declines. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 27 Deriving the Firm’s Demand for Labor Changes in the price of a good and improvements in technology shift the demand curve for labor to the right. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 28 EXHIBIT 4 © 2013 Cengage Learning SHIFT IN THEA DEMAND CURVE FOR LABOR CAUSED BY AN INCREASE IN THE PRICE OF THE GOOD Gottheil — Principles of Economics, 7e 29 Exhibit 4: Shift in the Demand Curve for Labor Caused by an Increase in the Price of the Good How does an increase in the price of coal affect the number of miners hired at a wage rate of $24? • When the price of coal is $2, seven miners are hired at a wage rate of $24. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 30 Exhibit 4: Shift in the Demand Curve for Labor Caused by an Increase in the Price of the Good How does an increase in the price of coal affect the number of miners hired at a wage rate of $24? • When the price of coal increases to $3, the demand curve for miners shifts to the right. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 31 Exhibit 4: Shift in the Demand Curve for Labor Caused by an Increase in the Price of the Good How does an increase in the price of coal affect the number of miners hired at a wage rate of $24? • At the new coal price, nine miners are demanded at the wage rate of $24. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 32 EXHIBIT 5 © 2013 Cengage Learning THE DERIVATION OF MRP USING OLD AND NEW TECHNOLOGY (PRICE OF COAL = $2) Gottheil — Principles of Economics, 7e 33 Exhibit 5: The Derivation of MRP Using Old and New Technology (Price of Coal = $2) How does a change from old technology to new technology affect the MPP and MRP in Exhibit 5? • With new technology the same miner is able to produce twice as much coal. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 34 Exhibit 5: The Derivation of MRP Using Old and New Technology (Price of Coal = $2) How does a change from old technology to new technology affect the MPP and MRP in Exhibit 5? • The new technology doubles both MPP and MRP. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 35 Industry Demand for Labor If all of the firms in an industry have essentially the same quality resources, use the same technology, and compete for the same laborers in the same labor market, then the industry’s demand curve for labor is the same as the individual firm’s demand curve for labor, magnified by the number of firms in the industry. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 36 EXHIBIT 6 © 2013 Cengage Learning INDUSTRY DEMAND FOR LABOR Gottheil — Principles of Economics, 7e 37 Exhibit 6: Industry Demand for Labor What is the firm’s demand for labor at a wage rate of $20 compared to the industry’s demand for labor at the same wage rate? • The firm’s demand for labor is 8 at a wage rate of $20. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 38 Exhibit 6: Industry Demand for Labor What is the firm’s demand for labor at a wage rate of $20 compared to the industry’s demand for labor at the same wage rate? • With 1,000 firms in the industry, the industry’s demand for labor at $20 = (8 × 1,000) = 8,000 laborers. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 39 The Supply of Labor The opportunity cost of working —the value a laborer places on the next best alternative to working—is different for different people. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 40 The Supply of Labor Opportunity cost determines how many people are willing to work at differing wage rates. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 41 EXHIBIT 7 © 2013 Cengage Learning THE SUPPLY CURVE OF LABOR Gottheil — Principles of Economics, 7e 42 Exhibit 7: The Supply Curve of Labor Why does the labor supply curve slope up in Exhibit 7? • The curve is upward sloping because the higher the wage rate, the more willing are workers to supply greater quantities of labor. Their opportunity costs are met at higher wage rates. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 43 The Supply of Labor Three factors affect workers’ willingness to supply their labor at different wage rates: changes in alternative employment opportunities, changes in population size, and changes in wealth. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 44 The Supply of Labor: Changes in Alternative Employment Opportunities • When new industries willing to pay higher wage rates enter a market, fewer laborers are willing to work for the older industry at the lower wage rate. • The supply curve for labor in the older industry shifts to the left. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 45 The Supply of Labor: Changes in Population Size • When the population of a region declines, the number of workers willing to work at any wage rate declines. • The supply curve for labor shifts to the left. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 46 The Supply of Labor: Changes in Wealth • When people have more wealth, they choose more leisure time and less work. • The supply curve for labor shifts to the left. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 47 EXHIBIT 8 © 2013 Cengage Learning CHANGES IN THE SUPPLY CURVE OF LABOR Gottheil — Principles of Economics, 7e 48 Exhibit 8: Changes in the Supply Curve of Labor What happens to the quantity of labor supplied at a wage rate of $20 when the supply curve shifts from S to S ? 1 • The quantity of labor supplied drops from 8,000 to 6,000. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 49 The Supply of Labor An increase in the wage rate typically induces workers to increase the quantity of labor supplied, but only up to a certain point. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 50 The Supply of Labor After that point, an increase in the wage rate results in less, not more, labor supplied. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 51 EXHIBIT 9 © 2013 Cengage Learning THE BACKWARD-BENDING SUPPLY CURVE OF LABOR Gottheil — Principles of Economics, 7e 52 Exhibit 9: The BackwardBending Supply Curve of Labor What is the wage rate at which the laborer in Exhibit 9 decides to cut back on the quantity of labor he is willing to supply? • The laborer is willing to increase the quantity of labor supplied up to a wage rate of $40. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 53 Exhibit 9: The BackwardBending Supply Curve of Labor What is the wage rate at which the laborer in Exhibit 9 decides to cut back on the quantity of labor he is willing to supply? • Above $40, the laborer cuts back on hours worked per week and gains more leisure time. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 54 Exhibit 9: The BackwardBending Supply Curve of Labor What is the wage rate at which the laborer in Exhibit 9 decides to cut back on the quantity of labor he is willing to supply? • To the laborer, the value of the leisure time is greater than the extra income he could have earned by working more hours. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 55 Deriving Equilibrium Wage Rates Combining the industry demand curve for labor and the industry supply curve for labor allows the industry equilibrium wage rate to be derived. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 56 Deriving Equilibrium Wage Rates • Individual firms within the industry have no influence on the market wage rate. • Firms must accept the market wage rate and face a horizontal supply curve for labor. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 57 EXHIBIT 10 THE LABOR MARKET © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 58 Exhibit 10: The Labor Market How is the level of the horizontal labor supply curve for the firm in panel b of Exhibit 10 determined? • The level of the labor supply curve is equal to the equilibrium wage rate of the industry (W = $20). © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 59 Explaining Wage Rate Differentials How different opportunity costs of laborers affect the supply curve of labor and how differences in technology and the price of goods produced by labor affect MRP help explain why different wage rates exist in different labor markets. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 60 EXHIBIT 11 © 2013 Cengage Learning U.S.- MEXICO WAGE RATE DIFFERENTIALS Gottheil — Principles of Economics, 7e 61 Exhibit 11: U.S.- Mexico Wage Rate Differentials What are the factors that caused the wage rate to decline in Texas in Exhibit 11? • Immigration from Chihuahua to Texas increased the pool of laborers and thus shifted Texas’ labor supply curve to the right. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 62 Exhibit 11: U.S.- Mexico Wage Rate Differentials What are the factors that caused the wage rate to decline in Texas in Exhibit 11? • At the same time, relocation of factories from Texas to the Chihuahua shifted Texas’ demand curve for labor to the left. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 63 Exhibit 11: U.S.- Mexico Wage Rate Differentials What are the factors that caused the wage rate to decline in Texas in Exhibit 11? • An increase in the supply of labor and a decrease in the demand for labor caused the wage rate to decline in Texas. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 64 EXHIBIT 12 MEXICAN FOREIGN BORN POPULATIONS IN THE UNITED STATES: LEGAL 1960–2006 POPULATION) Source: U.S. Census Bureau, Working Paper No. 29, Historical Census Statistics on the Foreign-Born Population of the United States: 1850–1900, US Government Printing Office, Washington, DC, 1999. Data for 2000 and 2006 are from US Bureau’s Census 2000 and American Community Survey 2006. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 65 Exhibit 12: Mexican Foreign Born Populations in the United States: Legal 1960–2006 Mexican immigration (legal) more than doubled during the 1990s and continued to increase into the twenty-first century © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 66 Explaining Wage Rate Differentials The supply curve of labor is affected not only by the supply conditions in the labor market, but also by the government’s immigration policy. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 67 EXHIBIT 13 MEDIAN HOURLY PAY FOR SELECT EU COUNTRIES: PRIVATE SECTOR (AS PERCENT OF HOURLY PAY IN DENMARK) Source: FedEE Pay in Europe 2006 Report, shown in http://www.finfacts.com/Private/isl/PayinEurope.htm © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 68 Exhibit 13: Median Hourly Pay for Select EU Countries: Private Sector Substantial migrant flows from East Europe to West Europe because of: • Basic EU policy of free movement of population within the EU • Considerable East-West wage differentials within the EU © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 69 EXHIBIT 14 MIGRANT POPULATIONS AND PERCENT OF TOTAL WORLD POPULATION: 2005 (THOUSANDS AND PERCENT) Source: International Migration, 2006, United Nations, Department of Economic and Social Affairs, Population Division, 2006 © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 70 Exhibit 14: Migrant Populations and Percent of Total World Population: 2005 In 2005, an estimated 191 million people representing three percent of the world’s population lived outside their country of birth. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 71 Exhibit 14: Migrant Populations and Percent of Total World Population: 2005 1.4 percent of the total population in the less developed countries migrated in 2005. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 72 Persisting Wage Differentials Noncompeting labor markets • Markets whose requirement for specific skills necessarily excludes workers who do not have the required skills. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 73 Persisting Wage Differentials Specific talents, limited to small numbers of people, create unique labor markets that allow relatively high wage rates and protect wage rates against erosion. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 74 The Economics of Minimum Wage Rates The problem with persistent wage differentials is not so much that a few people make millions, but that some people are unable to compete successfully in any occupation that provides an adequate standard of living. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 75 The Economics of Minimum Wage Rates In an effort to remedy the problem, government can outlaw low wage rates by implementing a minimum wage law. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 76 The Economics of Minimum Wage Rates • The problem with mandated minimum wage rates is that employers cannot be expected to hire workers whose MRP is below the legislated minimum wage rate. • Thus some workers are left with no job at all. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 77 The Economics of Minimum Wage Rates The impact of minimum-wage legislation on low-wage-rate-earning people depends on the price elasticities of demand and supply for labor. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 78 EXHIBIT 15 THE EFFECTS OF MINIMUM WAGE RATES © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 79 Exhibit 15: The Effects of Minimum Wage Rates 1. How many people lose their job when minimum wage rates are implemented under the price elasticities of supply and demand for labor in panel a? • 1,000 workers were employed at $3 per hour. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 80 Exhibit 15: The Effects of Minimum Wage Rates 1. How many people lose their job when minimum wage rates are implemented under the price elasticities of supply and demand for labor in panel a? • Only 300 workers are employed at $5.15. Thus 700 workers lose their jobs. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 81 Exhibit 15: The Effects of Minimum Wage Rates 2. How many people lose their job when minimum wage rates are implemented under the price elasticities of supply and demand for labor in panel b? • 1,000 laborers were employed at $3 per hour. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 82 Exhibit 15: The Effects of Minimum Wage Rates 2. How many people lose their job when minimum wage rates are implemented under the price elasticities of supply and demand for labor in panel b? • 9,000 laborers are employed at $5.15 per hour. Thus only 100 lose their job. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 83 The Ethics of w = MRP • Most economists accept marketdetermined wage rates as ethically defensible. • The ethic is expressed as “From each according to his or her contribution, to each according to his or her contribution.” © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 84 The Efficiency Wages Theory Efficiency wages • A wage higher than the market’s equilibrium rate; a firm will pay this wage in the expectation that the higher wage will reduce the firm’s labor turnover and increase labor productivity. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 85 The Efficiency Wages Theory There are several reasons why a firm may choose to pay efficiency wages: • Efficiency wages increase workers’ morale and motivation on the job. • Efficiency wages allow the firm to select more qualified workers. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 86 The Efficiency Wages Theory There are several reasons why a firm may choose to pay efficiency wages: • Reduce labor turnover. • Deter workers from joining unions. • Fairness—if the firm is making a profit, it should share some with its workforce. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 87 The Principal-Agent Problem Principal-agent problem • A problem that arises when either demander or supplier in a labor market exercises an undisclosed personal interest or motive that undermines the efficacy of the market. © 2013 Cengage Learning Gottheil — Principles of Economics, 7e 88