Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

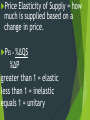

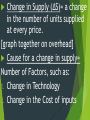

CH. 7 Section 1 Supply People produce g/s to gain benefits, whether it is money income or psychic income. Supply is from the PRODUCERS prospective! Suppliers want to sell their products for the most money possible in order to get the highest profit possible. Supply = the quantities of a product or service that a firm is willing and able to produce for sale at different prices. http://www.mcdonalds.com/us/en/supplierstories.html#/Lettuce [Demand is from the buyers perspective] [Supply is from the sellers perspective] Supply Schedule = a table that shows the relationship between P and QS of a g/s. P Q $1 100 $2 200 $3 300 $4 400 Supply Curve = graphic illustration of a supply schedule (EX: on overhead—include in notes) Market Supply = the total quantity of a product or service that all firms in a mkt. will make available for sale at various prices =add up all quantities that each firm in the mkt would supply at each price (overhead for ex. include in your notes) Law of Supply = the quantities of goods supplied will be greater at higher prices than will be supplied at lower prices. P S ↓P ↓ S Producers want to make the most money possible! It cost the same to produce a good so want to sell it at that highest price possible for more profit! Change in QS = change in the # of goods available due to a PRICE CHANGE. Reason for a ΔQS: Change in Price (ΔP) EX: McDonald’s increases the price of a large pop from $1 to $1.89 (graph on overhead) Price Elasticity of Supply = how much is supplied based on a change in price. PES = %ΔQS %ΔP greater than 1 = elastic less than 1 = inelastic equals 1 = unitary Change in Supply (ΔS)= a change in the number of units supplied at every price. [graph together on overhead] Cause for a change in supply= Number of Factors, such as: 1. Change in Technology 2. Change in the Cost of inputs EX: technology changes and there is a more efficient way to produce cars. This can increase productivity and lower the cost, which may allow GM to sell 650 cars at $20,000 instead of 600. A change in the cost of inputs may cause a loss for the firm. If the cost of labor goes up, or raw materials, or higher energy costs=all increase cost of production.