Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

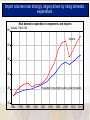

Perspectives on key economic issues Presentation to the Parliamentary Portfolio Committee on Finance by the South African Reserve Bank April 2013 Outline n Context: The global and domestic economy in a nutshell n Selected issues n Unsecured lending n The South African balance of payments n Monetary policy Context: The global and domestic economy in a nutshell Continued sluggishness in the world economy: Global real GDP growth slackened in the final quarter of 2012 as advanced economies registered a contraction 2,5% Recent global developments: a mixed bag n Events in Cyprus have again undermined confidence and cohesion in Europe n Aggressive expansionary policies adopted in Japan seem credible enough to have resulted in expectations of somewhat higher inflation expectations and improved growth n US fiscal dilemmas have been partly resolved but mostly postponed n Sub-Saharan African growth is buoyed by favourable prices of most export commodities, infrastructure spending, and new production facilities becoming operational n BRICS growth has slowed somewhat, particularly in Brazil, but remains brisk when compared with the advanced economies Global inflation pressures remain muted, especially in the advanced economies South Africa: Moderately better growth in the final quarter of 2012 as secondary sector picked up while primary sector contracted further 2,1% Growth in all the final domestic demand components slackened in the final quarter I : 4,3% G : -0,7% C : 2,4% Selected issues: Unsecured lending Banks’ general loans extended to the household sector rose strongly over the past three years D 19 However, there are tentative signs of moderation most recently, and the intention of some key lenders active in the market is to aim for slower growth in this business With unsecured lending constituting less than 15% of total lending to households, the household debt ratio inched lower in the final quarter of 2012 Selected issues: South Africa’s balance of payments Inflow of savings from ROW on the back of macro stability & stronger economic growth Balance on the financial account of the balance of payments 10 Percentage of GDP Surplus Financial sanctions Post-democratic normalisation 8 6 4 2 0 -2 -4 -6 Deficit 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 Movement from current-account surpluses in the sanctions era to sizeable deficits in recent years Balance on current account 8 Percentage of GDP Surplus 6 4 2 0 -2 -4 -6 Deficit -8 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 In recent years, widening current-account deficits reflect weak export volumes, largely due to structural impediments, while import volumes surged Volume of South Africa's imports and exports 280 Indices, 1994=100 Imports 240 200 160 Exports 120 80 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 Import volumes rose strongly, largely driven by rising domestic expenditure Real domestic expenditure components and imports 280 Indices: 1994=100 Imports 240 200 160 Household consumption and capital formation 120 80 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 And supported by growth in remuneration between 2008 and 2010 Digesting the current-account deficit A significant part of the deficit is attributable to imports of capital goods that are needed to address infrastructure backlogs, modernise the production structure and facilitate higher exports in future Real fixed capital formation by government and public corporations 160,000 Rm, 2005 prices 140,000 120,000 100,000 80,000 60,000 40,000 20,000 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 Reflected in part by rand weakness The South African rand has a floating exchange rate, so that deficits or surpluses deemed unsustainable by market participants result in exchange rate adjustment; there is an inbuilt shock absorber at play However, large exchange rate movements may have implications for inflation and necessitate policy adjustment Exchange rate trends vary across emerging markets and commodity producers South Africa has also become more robust in the face of possible external shocks through building up the country’s stock of international reserve assets Selected issues: Monetary policy Monetary policy has remained expansionary, with the nominal policy rate at its lowest level in more than three decades to support the economic recovery Inflation is inside the target range, and a trimmed mean measure of underlying inflation has been added Headline CPI Trimmed mean Market expectations are for short-term interest rates to increase moderately in 2014 This proxy for expected inflation has hovered slightly above 6 per cent for most of the past two years March MPC meeting: Inflation outlook has deteriorated slightly due to a more depreciated exchange rate and higher petrol prices, but is still projected to be within the target range over the effective policy time horizon 14 Targeted inflation Per cent Actual Forecast 12 10 2013Q3 6,3 8 6 2014Q4 5,2 4 Target range 2 50% Confidence interval 0 2006 75% Confidence interval 2007 Source: SARB core model 2008 2009 2010 2011 2012 2013 2014 An ongoing concern of the MPC is that administered price inflation remains well above the inflation target range; greater moderation and discipline are needed Conclusion n n n n n The global picture is one of sluggish growth, with the advanced economies registering a slight contraction in the final quarter of 2012 Domestic growth continued to be sluggish but less so than in the third quarter Capital inflows in various forms have been sufficient to fully finance the deficit on the current account Inflation remains inside the target range, and measures of underlying inflation are currently below the headline inflation rate Monetary policy is mindful of the need to support growth – to this end South Africa currently has the lowest nominal policy interest rate in 3 decades