Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

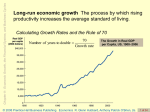

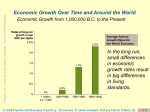

CHAPTER 10 Economic Growth, the Financial System, and Business Cycles Chapter Outline and Learning Objectives 10.1 Long-Run Economic Growth 10.2 Saving, Investment, and the Financial System 10.3 The Business Cycle ©© 2013 Pearson Education,Hall Inc. Publishing as Prentice Hall 2008 Prentice Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 1 of 40 33 Long-Run Economic Growth 10.1 LEARNING OBJECTIVE Discuss the importance of long-run economic growth. ©© 2013 Pearson Education,Hall Inc. Publishing as Prentice Hall 2008 Prentice Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 2 of 40 33 Chapter 21: Economic Growth, the Financial System, and Business Cycles Learning Objective 10.1 Long-Run Economic Growth Long-run economic growth The process by which rising productivity increases the average standard of living. FIGURE 10.1 The Growth in Real GDP per Capita, 1900–2006 © 2008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 3 of 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Learning Objective 10.1 Making the Connection The Connection between Economic Prosperity and Health © 2008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 4 of 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Annual Percent Change Year Real GDP Potential GDP 1999 $ 9,470 $ 9,281 2000 $ 9,817 $ 9,634 2001 $ 9,891 $ 9,991 2002 $10,049 $10,342 2003 $10,321 $10,677 Annual Percent Change in Real GDP: ((Current value – Prior Year Value) / Prior Year Value) x 100 Example: Annual Percent Change for real GDP from 1999 to 2000: Average Percent Change from 1999 to 2003: © 2008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 5 of 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Learning Objective 10.1 Long-Run Economic Growth Calculating Growth Rates and the Rule of 70 Number of years to double 70 Growth rate What Determines the Rate of Long-Run Growth? Labor productivity The quantity of goods and services that can be produced by one worker or by one hour of work. © 2008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 6 of 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles What determines the rate of long-run growth? Increases in real GDP per capita rely on increases in labor productivity: the quantity of goods and services that can be produced by one worker or by one hour of work. Why can the average American consume eight times as many goods and services now, as in 1900? Because the average American produces eight times as many goods and services in an hour now, as in 1900. So most of the answer to “what determines the rate of long-run growth” is the same as the answer to “what determines labor productivity growth?” © 2008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 7 of 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Factors affecting labor productivity growth Increases in capital per hour worked Capital is manufactured goods that are used to produce other goods and services. The more capital a worker has available to use (including human capital, the accumulated knowledge and skills workers possess), the more productive he or she will be. Technological change Improvements in capital or methods to combine inputs into outputs (i.e. new technologies) allow workers to produce more in a given period of time. The role of entrepreneurs here is critical, in pioneering new ways to bring together the factors of production to produce better or lower-cost products. © 2008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 8 of 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Learning Objective 10.1 Long-Run Economic Growth Potential Real GDP Potential GDP The level of GDP attained when all firms are producing at capacity. Potential GDP rises when… The growth in potential GDP in the U.S. has been relatively steady at about 3.3%; that is, the potential to produce final goods and services has been growing in the U.S. at about this rate over time. © 2008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 9 of 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Actual and potential GDP in the United States ©© 2013 Pearson Education,Hall Inc. Publishing as Prentice Hall 2008 Prentice Business Publishing Figure 10.2 Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 10 of 40 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Saving, Investment, and the Financial System 10.2 LEARNING OBJECTIVE Discuss the role of the financial system in facilitating long-run economic growth. ©© 2013 Pearson Education,Hall Inc. Publishing as Prentice Hall 2008 Prentice Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 11 of 40 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Learning Objective 10.2 Saving, Investment, and the Financial System Financial system The system of financial markets and financial intermediaries through which firms acquire funds from households. An Overview of the Financial System Financial markets Markets where financial securities, such as stocks and bonds, are bought and sold. Financial intermediaries Firms, such as banks, mutual funds, pension funds, and insurance companies, that borrow funds from savers and lend them to borrowers. © 2008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 12 of 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Three key services of the financial system The financial system provides three key services: Risk-sharing Liquidity Information © 2008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 13 of 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Learning Objective 10.2 Saving, Investment, and the Financial System The Macroeconomics of Saving and Investment Y = C + I + G + NX Y=C+I+G I=Y−C−G Sprivate = Y + TR − C − T Spublic= T − G − TR © 2008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 14 of 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Learning Objective 10.2 Saving, Investment, and the Financial System The Macroeconomics of Saving and Investment S = Sprivate + Spublic or S = (Y + TR − C − T) + (T − G − TR) or S=Y−C−G So, we can conclude that total saving must equal total investment: S=I © 2008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 15 of 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Learning Objective 10.2 Saving, Investment, and the Financial System The Market for Loanable Funds Market for loanable funds The interaction of borrowers and lenders that determines the market interest rate and the quantity of loanable funds exchanged. © 2008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 16 of 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Learning Objective 10.2 Making the Connection Ebenezer Scrooge: Accidental Promoter of Economic Growth? Who was better for economic growth: Scrooge the saver or Scrooge the spender? © 2008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 17 of 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles The Business Cycle 10.3 LEARNING OBJECTIVE Explain what happens during the business cycle. ©© 2013 Pearson Education,Hall Inc. Publishing as Prentice Hall 2008 Prentice Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 18 of 40 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Economic Growth, the Financial System, and Business Cycles Business cycle Alternating periods of economic expansion and economic recession. While real GDP per capita has risen about eight-fold since the start of the 20th century, it has not risen consistently every year. Since at least the early 19th century, the American economy has experienced alternating periods of expanding and contracting economic activity. © 2008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 19 of 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles The business cycle ©© 2013 Pearson Education,Hall Inc. Publishing as Prentice Hall 2008 Prentice Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 20 of 40 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles The business cycle, 2005-2011 This figure shows the movements in real GDP in the U.S. from 2005 to 2011. The period of recession starting in late 2007 and ending in mid 2009 was the longest and most severe since the Great Depression of the 1930s, prompting some to refer to it as the Great Recession. Real GDP growth after this recession has been slower than is typical at the start of a business cycle expansion. ©© 2013 Pearson Education,Hall Inc. Publishing as Prentice Hall 2008 Prentice Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 21 of 40 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles How do we known when the economy is in a recession? The federal government does not define when a recession starts or ends. The typical media definition of a recession is “two consecutive quarters of declining real GDP. However most economists defer to the judgment of the National Bureau of Economic Research: “A recession is a significant decline in activity spread across the economy, lasting more than a few months, visible in industrial production, employment, real income, and wholesale-retail trade.” ©© 2013 Pearson Education,Hall Inc. Publishing as Prentice Hall 2008 Prentice Business Publishing Table 10.1 NBER-defined recessions since 1950 Length of Peak Trough Recession July 1953 May 1954 10 months August 1957 April 1958 8 months April 1960 February 1961 10 months December 1969 November 1970 11 months November 1973 March 1975 16 months January 1980 July 1980 July 1981 November 1982 July 1990 March 1991 8 months March 2001 November 2001 8 months December 2007 June 2009 6 months 16 months 18 months Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 22 of 40 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Making the Connection Can a Recession Be a Good Time for a Business to Expand? Historically, recessions have generally been followed by periods of strong economic growth. Some firms take advantage of the low real interest rates that typically accompany a recession to make investments by expanding productive capacity, effectively betting that the growth will justify their investments. For example, computer chip maker Intel decided in early 2009 to proceed with a $7 billion expansion of its U.S. factories. Heavy equipment manufacturer Caterpillar acted similarly, expanding in order “to meet the expected increase in customer demand”. ©© 2013 Pearson Education,Hall Inc. Publishing as Prentice Hall 2008 Prentice Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 23 of 40 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles The effect of the business cycle on Boeing Boeing makes aircraft—very much a durable good. So we expect their sales to be strongly affected by recessions. The charts show this prediction to be accurate—though Boeing was less affected by the recession of 2007-2009 than we might have expected; overseas demand remained strong in this period. ©© 2013 Pearson Education,Hall Inc. Publishing as Prentice Hall 2008 Prentice Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 24 of 40 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles The effect of the business cycle on inflation—graph (red bars indicate recession) Notice that inflation tends to rise toward the end of an expansion, and fall over the course of each recession. ©© 2013 Pearson Education,Hall Inc. Publishing as Prentice Hall 2008 Prentice Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 25 of 40 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles The effect of the business cycle on unemployment As firms see their sales start to fall in a recession, they generally reduce production and lay off workers. (red bars indicate recession) Notice that unemployment often continues to rise, even after the end of each recession. © 2008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 26 of 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Fluctuations in real GDP: 1900-2010 Figure 10.10 Annual fluctuations in real GDP were typically greater before 1950 than after 1950. Economists refer to this as the “Great Moderation”. ©© 2013 Pearson Education,Hall Inc. Publishing as Prentice Hall 2008 Prentice Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 27 of 40 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Learning Objective 10.3 The Business Cycle What Happens during a Business Cycle? Recessions Have Been Milder and the Economy Has Been More Stable Since 1950 The Business Cycle Has Become Milder PERIOD AVERAGE LENGTH OF EXPANSIONS AVERAGE LENGTH OF RECESSIONS 1870-1900 26 months 26 months 1900-1950 25 months 19 months 1950-2001 61 months 9 months © 2008 Prentice Hall Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 28 of 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Explaining the Great Moderation Several factors help to explain the Great Moderation: The increasing importance of services Manufacturing (especially of durable goods) is more strongly affected by recessions. The economy is based more on services now, decreasing the effect of the business cycle on GDP. The establishment of unemployment insurance Before the 1930s, unemployment insurance and other government transfer programs like Social Security did not exist. These programs increase the ability of consumers to purchase goods and services during recessions. Active federal government stabilization policies Increased stability of the financial system ©© 2013 Pearson Education,Hall Inc. Publishing as Prentice Hall 2008 Prentice Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 29 of 40 34 Chapter 21: Economic Growth, the Financial System, and Business Cycles Explaining the Great Moderation Several factors help to explain the Great Moderation: The increasing importance of services The establishment of unemployment insurance Active federal government stabilization policies Many, though not all, economists believe that active government policies to lengthen expansions and minimize the effects of recessions have had the desired effect. The debate over the role of government in this way became particularly intense during the recession of 2007-2009. Increased stability of the financial system The severity of the Great Depression of the 1930s was in part caused by instability in the financial system; similar instability exacerbated the recession of 2007-2009. Returning to macroeconomic stability will require a stable financial system. ©© 2013 Pearson Education,Hall Inc. Publishing as Prentice Hall 2008 Prentice Business Publishing Economics R. Glenn Hubbard, Anthony Patrick O’Brien, 2e. 30 of 40 34