Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

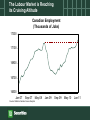

North American Outlook: Turning The Corner in 2011 February 2011 David Tulk, CFA Chief Canada Macro Strategist North American Outlook in a Nutshell • Global economy transitioning from a sugar high to a sustainable expansion. • Fiscal stimulus in the United States will ensure abovetrend growth in 2011 while the underlying economy continues to heal. • Canadian growth will slow, but become more balanced in 2011. US Economy Has Reached an Inflection Point ISM Composite and New Orders Index (Diffusion Index) 65 80 60 70 55 60 50 50 45 40 40 35 Composite Index (LHS) 30 New Orders Index (RHS) 30 Jan-05 Nov-05 Sep-06 Source: ISM/Haver Analytics 20 Jul-07 May-08 Mar-09 Jan-10 Nov-10 Fiscal Stimulus to Underpin 2011 Impact of Fiscal Stimulus on US Real GDP Growth (Percent) 1.0 0.6 0.2 -0.2 -0.6 Q4 Q1F 2010 Source: BEA / TD Economics Q2F Q3F 2011 Q4F Q1F Q2F 2012 Q3F Q4F Key Headwind to the Economic Recovery is the Labour Market US Job Losses by Recession (Millions of Jobs) 2 0 -2 -4 1960 1981 1990 2001 Current -6 -8 Census Hiring -10 0 5 10 15 20 25 30 Months Following Start of Recession Source: BLS/Haver Analytics 35 40 45 Canada is Not an Island ISM and Canadian GDP and Overnight Rate 8 Q/Q GDP Growth (green) / 2-qtr change in BoC rate (yellow) Canadian GDP Change in BoC Rate* 6 4 2 0 -2 -4 30 35 40 45 50 U.S. ISM (Index) *Change in following 2 qtrs; Source: Statscan, BEA, Bloomberg Source: BEA, Federal Reserve, Statistics Canada/Haver Analytics 55 60 65 International Backdrop has Taken a Bite Out of Canadian Growth Composition of Canadian Real GDP Growth (Percent) 12 8 4 0 -4 -8 -12 Sep-07 Domestic Demand Including Inventories Net Exports Real GDP Growth Jun-08 Source: Statistics Canada/Haver Analytics Mar-09 Dec-09 Sep-10 Stronger US Growth Will Rekindle Demand for Exports US Activity Index and Canadian Exports (Index) 115 Forecast 110 105 100 95 90 85 US Activity Canadian Exports 80 2001 2003 2005 Source: Bank of Canada / Haver Analytics 2007 2009 2011 Housing Market Coasting Towards a Soft Landing… Canadian Resale Activity and Sales-to-New Listings (3 Month Average Percent Change, Ratio) 10 0.8 8 Sales (3M MA, LHS) 6 Sales-to-Listings (RHS) 0.7 4 2 0.6 0 -2 0.5 -4 -6 0.4 -8 -10 Feb-08 0.3 Aug-08 Source: CREA Feb-09 Aug-09 Feb-10 Aug-10 … Due in Large Part to the Fall in Global Bond Yields Spread of 5 Year Conventional Mortgage Rate over Target Overnight Rate (Percent) 6.3 5.8 5.3 4.8 4.3 3.8 Jun-08 Oct-08 Feb-09 Jun-09 Oct-09 Feb-10 Jun-10 Oct-10 Source: Bank of Canada / Haver Analytics Consumer Spending Straining Under the Weight of Leverage Household Debt to Income Ratio (Percent of Personal Disposable Income) 180 Canada United States 160 140 120 100 80 1990 1993 1996 1999 2002 2005 2008 The Labour Market is Reaching its Cruising Altitude Canadian Employment (Thousands of Jobs) 17300 17100 16900 16700 16500 Jan-07 Sep-07 May-08 Source: Statistics Canada / Haver Analytics Jan-09 Sep-09 May-10 Jan-11 On Balance, the Canadian Economy Still Has Significant Spare Capacity 3 Measures of Canadian Capacity (Standardized Distribution) Output Gap 2 Difficulty Meeting Demand 1 0 -1 -2 -3 Sep-99 Mar-01 Sep-02 Mar-04 Sep-05 Mar-07 Sep-08 Mar-10 Source: Bank of Canada /Haver Analytics Bank of Canada to Balance Domestic Momentum with Global Risks Bank of Canada Overnight Interest Rate (Percent) 5 4 3 2 1 0 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Forecast as at December 2010; Source: Bank of Canada / TD Securities Canadian Dollar: Stuck in a Range With You Canadian Dollar 1.05 1.00 0.95 0.90 0.85 0.80 0.75 Aug-08 Nov-08 Mar-09 Jul-09 Nov-09 Mar-10 Jul-10 Nov-10 Source: Bloomberg Off Consensus Call for CAD USDCAD Forecast* Bloomberg Consensus TD Securities 2010Q1 2010Q2 2010Q3 2010Q4 2011Q1 2011Q2 2011Q3 2011Q4 1.02 1.06 1.03 1.00 0.99 0.98 0.98 1.00 1.02 1.06 1.03 1.00 1.02 1.09 1.06 1.03 *Forecast as of February 17, 2011; Source: Bloomberg, TD Securities CAD Less Impacted by Europe, but Risks Remain… USDCAD and Spain 5-Year CDS Spread 400 350 Spain CDS Spread (LHS, Basis Points) 1.33 USDCAD (RHS) 300 250 200 1.28 1.23 1.18 150 1.13 100 1.08 50 1.03 0 Jan-08 May-08 Oct-08 Mar-09 Aug-09 Jan-10 Jun-10 Nov-10 Source: Bloomberg, TD Securities 0.98 … and CAD is Vulnerable to Volatility and Risky Assets 1 Month Rolling CAD Correlations 1.0 0.5 0.0 S&P500 WTI 2Y Rate Spread Relative Eco Surprise -0.5 Oct-10 Nov-10 Source: Bloomberg, TD Securities Dec-10 Jan-11 Feb-11 Longer-Term Fundamentals More Supportive from International Investors… Net Financial Flows into Canada (6 Month Moving Average, Billions CAD) 12 8 Bonds Equities Money Market 4 0 -4 -8 1988 1991 1994 1997 Source: Statistics Canada / Haver Analytics 2000 2003 2006 2009 … And Foreign Central Banks "Other Currecy" Share of Total Allocated Reserves* (Percent) 5 4 3 2 1 1999 2001 2003 * Other than USD, GBP, EUR, JPY, CHF. Source: IMF COFER database 2005 2007 2009 Financial Market Implications • Considerable uncertainty means that volatility is the watchword of the day. • We have seen the cyclical trough in interest rates. Yields will continue to rise in tandem with the economic recovery. • USD will retain its safe-haven status in the event of financial market turmoil. Concluding Thoughts… • Recoveries from financial crises are typically subdued and take a long time. Except when stimulus has a role to play. • The inevitable hand off from public to private drivers of growth has been delayed but not avoided. • Canada is expected to become more balanced. David Tulk, CFA Chief Canada Macro Strategist 416 – 982 – 0445 [email protected]