Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

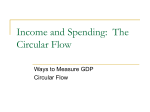

Productivity and Costs (Measure of Changes in Worker Efficiency) Web address: Revisions can be substantial Productivity – output of goods/services per labor hour. Measures how firms are using their employees and physical capital (land, materials, equipment). Most important determinant of economy’s long-term health and prosperity. Higher productivity keeps inflation, DP/P, in check. Track non-farm business sector productivity for best reading on Y. (75% of GDP) Productivity Growth and a Virtuous Cycle: productivity (Y/L) => economic growth (DY/Y) without inflation (DP/P). Falling ULC => exports (X), household wages/income, corporate profits, dividends, => business investment spending, => (Y/L) The Business Cycle and Productivity Swings (cyclical productivity growth, %D(Y/L)) Economic slowdown: spending => production (Y) => (Y/L) Recession: labor (L) => (Y/L) Recovery: production (Y) => (Y/L) Expansion: labor (L) => (Y/L) The Productivity/Unemployment Relationship: (Y/L) => profits => Investments => new business => employment 3 Major Components: %D W = %D (Y/L) + %D (WL)Y 1. Output Per Hour (Y/L): Productivity measures labor efficiency. Labor productivity is a leading indicator of inflation (DP/P). Productivity growth helps determine economic speed limit. Maximum sustainable economic growth rate = productivity growth + labor force growth 2. Compensation Per Hour (W): average hourly compensation rate. Provides clues on emerging wage pressures. Compensation = wages, salaries, bonuses, commissions, value of employment paid benefits (health costs, social security funds, private pensions). Compare compensation growth to productivity growth. 3. Unit Labor Costs (WL/Y): Labor costs to produce a single unit of output. Excellent indicator of business labor costs. Link between compensation per hour and output per hour. W = Y/L x (WL)/Y. Labor costs equal 2/3 of all business expenses. Close statistical relationship between ULC and CPI. ULC => DP/P and profits. P = PY –WL. P/Y = P – (WL)/Y If productivity growth > compensation growth => ULC => profits, inflation, wages, stock prices, living standards If compensation growth > productivity growth => ULC => DP/P ------------------------------------------------------------------------------------------------------------------------------------------------------------------ Market Analysis: Bonds: %D(Y/L) and DW/W => (DP/P)Et+1=> DBonds => iBonds Stocks: (Y/L) => (WL)/Y, (ULC) => profits => PStocks Dollar: Y/L => U.S. global competitive position => [DP/P U.S./DP/PROW] => X, M =>dollar Labor Productivity, Compensation and Costs (Nonfarm Business) (% chg from year ago) 9% 9% 4th Quarter 2012 (SAAR) 2.4% = 4.5% + = -2.1 Compensation = Labor Costs per Output + Output per Hour 8% 7% 8% 7% 6.1% 5.6% 6% 5.0% 4.9% 4.7% 4.6% 5% 4.5% 4.3% 4.2% 3.6% 3.7% 3.5% 3.4% 4% 3.2% 3.1% 3.1% 3.0% 2.9% 2.9% 2.7% 2.6% 2.5% 2.5% 3% 2.3% 2.2% 1.9% 1.9% 1.9% 1.8% 1.8% 1.6% 1.6%1.5% 1.5% 1.7% 2% 1.3%1.1% 1.1% 1.2% 1.1% 1.0% 0.9% 0.8%0.9% 0.7% 0.6% 0.6% 1% 0.4% 0.2% 0.1%0.2% 0% -1% 6% 5% 4% 3% 2% 1% 0% 00 01 02 03 04 05 -4% Source: Bureau of Labor Statistics 07 08 09 -1.1% -2% -3% 06 Productivity Hourly Compensation Unit Labor Costs 10 11 12 13 -1% -2% -3% -4% P = PY – wL Productivity = Y/L Y/L => P P => P Wage Growth Rate Analysis DW/W = %D (Y/L) + (DP/P) 2002-2003, U.R. > 5% 4% = 4% + 0% Wage growth compensated for productivity but not the 2.2% inflation 2005-2006, U.R. < 5% 4.5% = 2.5% + 2% Wage growth compensated for productivity, and part of 3.5% inflation Circular-Flow Diagram Government purchases of goods and services Government borrowing Government Consumer spending Government transfers Taxes Private savings Households Wages, profit, interest, rent Factor Markets Wages, profit, interest, rent GDP Investment Firms Borrowing and stock issues by firms Foreign borrowing and sales of stock Exports Rest of the world Imports Foreign lending and purchases of stock Financial Markets Interest Rates and Recessions 1988-2012 10 10 9 9 8 8 7 7 6 6 5 5 4 4 3 3 2 2 1 1 0 0 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 Recession Baa Fed Funds 10-yr Treas Inflation Expectations 2003-2012 6 6 Inflation Expectations 10-yr Treas TIPS (10-Yr) 5 5 4 4 3 3 2 2 1 1 0 0 03 04 05 06 07 08 09 10 -1 11 12 13 -1 Source: Federal Reserve Business Fixed Investment (Nonresidential Structures) 40 28 24 30 22 19 18 16 20 -10 -20 11 7 2 0 21 10 8 0 0 Q 1 0 1Q 1 2 0 0 2 Q 1 0 3 Q 1- 10 - 24- 2Q 1 -4 -6 - 11 9 8 5 4 12 30 13 13 10 40 35 1 0 5Q - 21 0 6 Q 1 0 7Q 1 -8 9 1 20 13 11 10 10 0 8 Q1 0 9 Q1 -4 10 Q 1 11Q 1 -2 12 Q 1 0 -1 -10 - 10 -20 - 17 - 2- 02 0 -30 -33 -23 -27 -29 - 3-13 1 -30 -28 -40 -40 -50 -50 Annualized Quarter Growth Rate % Change From Quarter One Year Ago 7 Housing Starts & Building Permits (Measure of Current and Future Housing Construction) Web: www.census.gov/const/www/newresconstindex.html Housing starts has revisiosn for preceding 2 months, permits for preceding one month. Seasonal adjustment changes made in April for past 2 years. Housing starts and permits are very effective and reliable leading indicators of future economic activity. Both are useful forecasting tools. Census Bureau surveys builders in 19,000 localities across the county during the first 2 weeks of each month. Housing starts are seasonally adjusted but extreme weather conditions can make data extremely volatile. So monitor data over 3-4 month period to detect underlying trend. Housing starts are a function of interest rates, real personal income growth, consumer confidence, and tax legislation (builder tax breaks, mortgage interest payment deductions) Housing is a very interest rate sensitive market. interest rates => housing demand => housing starts interest rates => builders demand for construction loans Housing has a large “multiplier effect” on the economy and is a major swing industry. housing construction => many other sectors ( steel, wood, electricity, glass, plastic, wiring, piping, concrete). House ground breaking to completion typically takes 6 months. A vibrant home selling market => sales of furniture, carpets, home electronics and appliances. 3 Housing Starts Categories: Single Family homes – 75% of total home building (reliable economic indicator) 2-4 unit apartments – 5% of market (townhouse or small condos) > 5 unit structures – 25% of residential housing starts (apartment buildings) 50 unit apartment = 50 starts Housing starts > 2 million may lead to shortages of supplies and skilled workers Housing starts between 1.5-2 million indicates healthy home construction industry Housing starts < 1 million leads to an economic slowdown Housing permits – Builders in most U.S. localities must file a permit and receive authorization in advance of construction. Permits lead housing starts by 1-3 months and is one of the 10 components of the Index of Leading Economic Indicators ------------------------------------------------------------------------------------------------------------------------------------------------ Market Analysis: Bonds: If housing starts & Y > YPot => DP/P => DBonds => iBonds Stocks: If housing starts => DY/Y => profits => PStocks Dollar: Housing starts => DY/Y => profits and iBonds => dollar Single Family Housing Starts & Building Pe rmits 2000 2000 1800 1800 1600 1600 1400 1400 1200 1200 1000 1000 800 800 600 600 400 400 200 200 95 96 97 98 99 00 01 Thousands Thousands (seasonally adjusted annual rate) 02 03 04 05 06 07 08 09 10 11 12 13 Starts Re ce ssi on Bui l di ng Pe rmi ts