Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

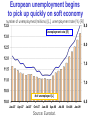

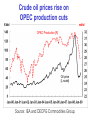

The External Environment for Developing Countries June 2009 The World Bank Development Economics Prospects Group Industrial countries Largest recipients of TARP funds Banks that borrowed funds under TARP Amount Borrowed ($bn) Citigroup Bank of America/Merrill Lynch JPMorgan Chase Wells Fargo 50 45 25 25 Goldman Sachs Morgan Stanley U.S. Bancorp Bank of New York Mellon Corp. 10 10 6.6 2.5 State Street Corp 2.5 Source: U.S. Treasury USA Retail sales in U.S. weaken after initial rebound U.S. retail sales values, index, Aug. 2009=100 Total retail sales Motor vehicles and parts Source: Thomson/Datastream, Commerce Department. Core inflation falling Japanese consumer prices, year-over-year percent change Headline inflation Core inflation Source: Thomson/Datastream, OECD. ECB interest rate and Inflation Eurozone consumer prices, year-over-year percent change ECB Interest rate Headline inflation Core inflation Source: Thomson/Datastream, OECD. Japanese exports to China In Billion Yen Exports to China (RHS) Total exports, excluding China (lhs) Source: Thomson/Datastream Unemployment close to 2003 Level Percentage of labor force 5.5 Unemployment rate 5.0 4.5 4.0 3.5 Jan-00 Jul-01 Jan-03 Jul-04 Source: Thomson/Datastream Jan-06 Jul-07 Jan-09 Euro Area Q1- Sharply lower as stock building turns negative growth of real GDP, and contributions to growth in percentage points Stocks Government Consumption Investment Net Exports Source: Eurostat Leading indicators for Europe lag those for the OECD OECD composite leading indicators OECD Germany Source: Thomson/Datastream, OECD. Retail sales in U.S. weaken after initial rebound U.S. retail sales values, index, Aug. 2009=100 Total retail sales Motor vehicles and parts Source: Thomson/Datastream, Commerce Department. Japanese Industrial Production Volume Index, 2005 = 100 120 Industrial Production 110 100 90 80 70 60 Jan-07 May-07 Sep-07 Jan-08 Source: Thomson/Datastream May-08 Sep-08 Jan-09 European unemployment begins to pick up quickly on soft economy number of unemploymed (millions) [L], unemployment rate (%) [R] Unemployment rate [R] # of unemployed [L] Source: Eurostat. German factory orders moving towards a bottom in February? factory orders, domestic and export, ch% saar domestic orders Total export orders Source: Bundesbank. Industrial production OECD industrial production down 34% in February (saar) industrial output, ch% (3m/3m saar) Developing countries High-income OECD countries Source: Thomson/Datastream, DECPG. Continued declines across emerging markets (EAP an exception) industrial production ch% (3m/3m saar) East Asia Latin America South Asia Europe and Central Asia Source: Thomson/Datastream, DECPG. NIEs and Thailand record positve monthly IP gains industrial production ch% (m/m seasonally adjusted) Korea Thailand Hong Kong (SAR, China) Source: Thomson/Datastream, DECPG. International trade Pace of decline in trade is easing on a momentum basis goods exports, nominal, qtr/qtr ch% (saar) Developing Countries Source: Thomson/Datastream Oil prices Crude oil prices rise on OPEC production cuts $/bbl mb/d OPEC Production [R] Oil price [L scale] Source: IEA and DECPG Commodities Group. World Oil Consumption Growth (mb/d y/y) OECD Non-OECD Source: IEA and DECPG Commodities Group. M bbl U.S. crude oil stocks rise on weak demand 5-year high-low ranges Source: U.S. Dept Energy and DECPG Commodities Group. Non-oil commodity prices Food prices decline in March on weak demand (2000=100) Source: DECPG Commodities Group. Copper prices rebound on falling stocks ‘000 tons $/ton Copper price LME stocks Source: LME and DECPG Commodities Group. Consumption Growth (% y/y) Aluminum Copper Crude Oil World China World China World China 2002-06 7.5 19.9 3.0 9.6 2.0 9.1 2007 10.4 42.8 6.6 34.6 1.2 4.6 1H08 5.6 15.9 0.1 7.4 0.9 5.0 2H08 -6.0 -4.7 -3.5 1.8 -1.5 3.6 1Q09 -20.3 -10.4 -17.6 0.4 -3.7 -3.5 average Source: DECPG Commodities Group. International Finance Capital flows down by two-thirds from first-quarter 2008 levels Gross capital flows to emerging markets $ billion 2007 2008 Q1 Total Total 2009 Q1 Total Jan Feb Mar Q1 156 652 103 389 23 8 9 40 Bonds 58 146 12 65 9 7 2 18 Banks 72 312 71 257 8 1 5 13 Equity 26 194 20 68 6 1 2 8 42 156 19 90 9 3 4 17 20 45 5 20 5 3 2 10 79 247 36 157 5 1 0 5 27 64 2 35 2 1 0 3 24 188 38 98 8 4 2 14 8 23 3 7 2 3 0 5 11 61 11 44 0 1 2 3 Lat. America Bonds E. Europe Bonds Asia Bonds Others Source: DECPG Finance Team. Strong returns to EM equities in 2009 Total returns yr to date in local currency, % MSCI Developed MSCI EM MSCI BRIC EM BIG Developed HY bond *as of April 17th Source: Morgan-Stanley through Thomson/Datastream Volume of EM IPOs has come to a standstill since September 2008 capital raised ($bn) [L], number of deals [R] Capital raised [L] # of deals [R] Source: Dealogic Currencies Focus The External Environment for Developing Countries April 2009 The World Bank Development Economics Prospects Group