Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Pensions crisis wikipedia , lookup

Non-monetary economy wikipedia , lookup

Edmund Phelps wikipedia , lookup

Money supply wikipedia , lookup

Quantitative easing wikipedia , lookup

Inflation targeting wikipedia , lookup

Austrian business cycle theory wikipedia , lookup

Full employment wikipedia , lookup

Fiscal multiplier wikipedia , lookup

Monetary policy wikipedia , lookup

Transformation in economics wikipedia , lookup

Early 1980s recession wikipedia , lookup

Phillips curve wikipedia , lookup

Stagflation wikipedia , lookup

Post-war displacement of Keynesianism wikipedia , lookup

Interest rate wikipedia , lookup

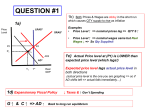

The Keynesian Model Chapter 9 John Maynard Keynes and the General Theory of Employment, Interest and Money Derivation of the Keynesian AS Crucial assumption: If nd is less than ns, W does not fall Nominal wages are sticky downwards (Fig. 9.1) 1. 2. 3. 4. 5. 6. We start from an initial given point (P0,Y0) in the (P,Y) space. Increase P0 to P1. If nd > ns, W increases so that W/P remains the same. W1/P1 = W0/P0 and we have now (P1,Y0). Now, let us decrease P0 to P2. In the very short run, the real wage W0/P2 is associated with nd<ns, and the wage does not fall (Keynesian assumption). Employment falls to nlow and we have ‘involuntary unemployment’. Y falls to Ylow . Using (P0,Y0) and (P2,Ylow), we derive the Keynesian AS. Survival guide fro ISLM with Keynesian AS 1. 2. 3. 4. Make all moves in the (i,Y) space and make all shifts to IS and LM here. Adjust Y (use the final value) in the (P,Y) space. The AD shifts to keep Y in (I,Y) and (P,Y) spaces consistent. Here, we get the final P and Y values. Adjust the expenditure line. Determine if C and I have changed. Also, determine what happens to real wages. If nd < ns employment will fall. If nd > ns nominal wages adjust to ensure that real wage remains the same. Interpret the results. Policy Experiment I An increase in G (Fig. 9.2) 1. 2. 3. 4. The IS curve shifts to the right. Interest rates (i) increase, Y increases to Y1. In the (P,Y) space, the AD curve shifts to the right. Inflation increases (to P1). The expenditures line shifts up. C increases; I falls. ns > nd (both at W0/P0 and W0/P1 ), so W does not change and real wages fall but employment increases. Note the Keynesian multiplier effect. Results: An increase in G increases employment, C and Y. But I and real wages fall. Policy Experiment II An increase in M (Fig. 9.3) LM shifts to the right and interest rates decrease. 2. In the (P,Y) space, the AD curve shifts to the right. Inflation increases (to P1) and Y increases. 3. The expenditures line shifts up. C and I increase. ns > nd (both at W0/P0 and W0/P1 ), so W does not change and real wages fall but employment increases. 4. Results: A monetary expansion as a tool of demand-side stabilization is effective in increasing Y and employment. Overheating (Fig. 9.4) 1. Policy Experiment III Engineering a soft-landing (Fig. 9.5) Policymakers are trying to cool down the overheated economy. The Fed contracts money. 1. 2. 3. 4. LM2 shifts to the left (to LM1) and interest rates increase to ihigher. Y falls to Ymoderate. Since monetary policy works with a significant and variable lag, this process can take from 6 months to 2 years (Milton Friedman). In the (P,Y) space, the AD curve shifts to the left (Ymoderate). Inflation falls (to Pmoderate). The expenditures line shifts down. C falls as Y declines, and I falls as a result of higher interest rates. Since P falls, real wages increase and employment falls to nlower. Results: If the economy can be stabilized at Ymoderate, Pmoderate, and nlower, then we can have a successful softlanding. Because contractionary fiscal policies involve longer-term decision making and longer implementation lags, monetary contraction remains the policy of choice to engineer a soft-landing. Policy Experiment IV Engineering a soft-landing (Fig. 9.6): When low interest rates no longer work! Assume that consumer and investor confidence levels have fallen dramatically (e.g. as a result of SAP bubble). 1. IS0 shifts to the left (to IS1) and interest rates and Y fall. 2. The Fed increases M and lowers interset rates further to revive Y. Interest rates are at ifinal (very low rates) and Y stabilizes at Yfinal , which is still lower than the initial level,Y0. 3. In the (P,Y) space, AD0 shifts to ADfinal and P falls to Pfinal . 4. The expenditures line shifts down. Cfinal is lower than C0 , and Ifinal is lower than I0 (assuming the effect from the fall in investor confidence dominates the effect from the fall in interest rates). As P increases, real wages increase so unemployment increases. 5. Results: We get a situation similar to the liquidity trap. Expansionary monetary policy is impotent! Example: The U.S. by late 2008. The Phillips Curve A negative relationship between the rate of inflation and changes in unemployment (published in a 1958 article by William Phillips). Consistent with the predictions of the Keynesian model. Led to the (controversial) outputinflation tradeoff. The Yield Curve and the Keynesian Paradigm Upward slopping yield curve: Often, indicative of an economy in the early stages of a sustained recovery. As the AD increases (as a result fiscal or monetary expansion), the rate of inflation is expected to increase so lenders will incorporate this in their decisions of long term loans (the Fisher effect). Thus, long-term rates are higher than short term rates. Inverted yield curve: Often, indicative of an impending recession. (See experiment III) When the Fed engineers soft-landing, lenders see that short-term interest rates (controlled by the Fed) are going up and so they expect a recession or at least a slowdown of the economy. This will eventually decrease the rate of inflation so expectation of less future inflation leads to lower nominal long-term interest rates. The Great Depression: Four Policy Mistakes Wage Floors 2. Tax Increases and Decreases in Government Spending 3. Liquidity Crisis 4. The Smoot-Hawley Act of 1930 1. Could a Great Depression happen again? Discussion: Article 9.3