Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

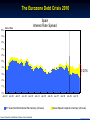

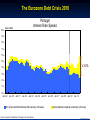

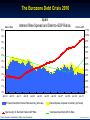

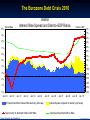

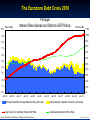

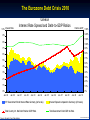

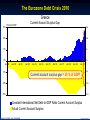

© RAINER MAURER, Pforzheim Digression: The Eurozone Debt Crisis 2010 Prof. Dr. Rainer Maurer Maure -1- © RAINER MAURER, Pforzheim Digression: The Eurozone Debt Crisis 2010 Prof. Dr. Rainer Maure -2- The Eurozone Debt Crisis 2010 ➤ The Return of the Interest Rate Spreads: After the foundation of the European Monetary Union (EMU) interest rates spreads between the member states nearly disappeared. ■ By the end of the year 2008, interest rate spreads reappeared. ■ For some countries interest rate spreads have become large: © RAINER MAURER, Pforzheim ■ Prof. Dr. Rainer Maure -3- The Eurozone Debt Crisis 2010 10% Spain Interest Rate Spread Interest Rate 9% 8% 7% 6% 5% 4% 2,0% 3% 2% 1% © RAINER MAURER, Pforzheim 0% Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 10Y Government Bond Interest Rate Germany (left scale) Source: Eurostat, Central Bank of Spain, Own Calculations Prof. Dr. Rainer Maure Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 Interest Spread compared to Germany (left scale) -4- © www.rainer-maurer.com The Eurozone Debt Crisis 2010 Ireland Interest Rate Spread 10% Interest Rate 9% 8% 7% 6% 5% 4% 2,5% 3% 2% 1% © RAINER MAURER, Pforzheim 0% Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 10Y Government Bond Interest Rate Germany (left scale) Prof. Dr. Rainer Maure Source: Eurostat, Own Calculations Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 Interest Spread compared to Germany (left scale) -5- © www.rainer-maurer.com The Eurozone Debt Crisis 2010 10% Portugal Interest Rate Spread Interest Rate 9% 8% 7% 6% 5% 3,4% 4% 3% 2% 1% © RAINER MAURER, Pforzheim 0% Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 10Y Government Bond Interest Rate Germany (left scale) Source: Eurostat, Central Bank of Portugal, Own Calculations Prof. Dr. Rainer Maure Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 Interest Spread compared to Germany (left scale) -6- © www.rainer-maurer.com The Eurozone Debt Crisis 2010 10% Greece Interest Rate Spread Interest Rate 9% 8% 7% 6,9% 6% 5% 4% 3% 2% © RAINER MAURER, Pforzheim 1% 0% Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 10Y Government Bond Interest Rate Germany (left scale) Source: Eurostat, Own Calculations Prof. Dr. Rainer Maure Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 Interest Spread compared to Germany (left scale) -7- © www.rainer-maurer.com The Eurozone Debt Crisis 2010 ➤ What caused the crisis? ■ Increasing public and private debt positions ....have casted doubt on the ability of governments and banks safeguarded by governments to pay back debt. ■ Investors fear of a default of governments on their debt and © RAINER MAURER, Pforzheim ....demand therefore a higher risk premiums. Prof. Dr. Rainer Maure -8- The Eurozone Debt Crisis 2010 10% Interest Rate Spain Interest Rate Spread and Debt-to-GDP Ratios Debt-to-GDP 110% 9% 100% 8% 90% 80% 7% 70% 6% 60% 5% 50% 4% 40% 3% 30% 20% 1% 10% 0% Jan. 99 0% © RAINER MAURER, Pforzheim 2% Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 10Y Government Bond Interest Rate Germany (left scale) Interest Spread compared to Germany (left scale) Total Country Int. Net Debt Position GDP Ratio Total Government Debt GDP-to-Ratio Source: Eurostat, Central Bank of Spain, Own Calculations Prof. Dr. Rainer Maure -9- © www.rainer-maurer.com The Eurozone Debt Crisis 2010 10% Interest Rate Ireland Interest Rate Spread and Debt-to-GDP Ratios Debt-to-GDP 80% 70% 9% 60% 8% 50% 7% 40% 30% 6% 20% 5% 10% 0% 4% -10% 3% -20% 2% -30% -40% 1% -50% © RAINER MAURER, Pforzheim 0% Jan. 99 -60% Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 10Y Government Bond Interest Rate Germany (left scale) Interest Spread compared to Germany (left scale) Total Country Int. Net Debt Position GDP Ratio Total Government Debt GDP-to-Ratio Prof. Dr. Rainer Maure Source: Eurostat, Own Calculations - 10 - © www.rainer-maurer.com The Eurozone Debt Crisis 2010 10% Interest Rate Portugal Interest Rate Spread and Debt-to-GDP Ratios Debt-to-GDP 110% 9% 100% 8% 90% 80% 7% 70% 6% 60% 5% 50% 4% 40% 3% 30% 20% 1% 10% 0% Jan. 99 0% © RAINER MAURER, Pforzheim 2% Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 10Y Government Bond Interest Rate Germany (left scale) Interest Spread compared to Germany (left scale) Total Country Int. Net Debt Position GDP Ratio Total Government Debt GDP-to-Ratio Source: Eurostat, Central Bank of Portugal, Own Calculations Prof. Dr. Rainer Maure - 11 - © www.rainer-maurer.com The Eurozone Debt Crisis 2010 10% Interest Rate Greece Interest Rate Spread and Debt-to-GDP Ratios Debt-to-GDP 130% 120% 9% 110% 8% 100% 7% 90% 6% 80% 70% 5% 60% 4% 50% 3% 40% 30% 2% 20% © RAINER MAURER, Pforzheim 1% 10% 0% 0% Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 10Y Government Bond Interest Rate Germany (left scale) Interest Spread compared to Germany (left scale) Total Country Int. Net Debt Position GDP Ratio Total Government Debt GDP-to-Ratio Prof. Dr. Rainer Maure Source: Eurostat, Own Calculations - 12 - © www.rainer-maurer.com The Eurozone Debt Crisis 2010 ➤ The situation is even worse than these figures suggest! ■ The change of a country's total debt position is the negative current account surplus. ■ We can calculate the current account surplus which is necessary to stabilize the current international debt-to-GDP ratio with the following formula (for a derivation see the digression): Interest Rate Primary Current Account Balance © RAINER MAURER, Pforzheim EX-IM-i*D B Y i GDP Growth Y dY dt International Net Debt Position of the Country D Y GDP Prof. Dr. Rainer Maure - 13 - The Eurozone Debt Crisis 2010 © RAINER MAURER, Pforzheim ➤ Applying this formula to the data of the countries shows that their actual account surplus is far away from the surplus necessary to keep their debt-to-GDP ratio constant: Prof. Dr. Rainer Maure - 18 - The Eurozone Debt Crisis 2010 Spain 15% Current Account Surplus Gap Percent of GDP 15% Current account surplus necessary to stabilize the International Debt-to-GDP ratio is 7,5% of GDP. 10% 10% 5% 5% 0% 0% Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 -5% -5% Acutal current account surplus - 5,5% of GDP! © RAINER MAURER, Pforzheim -10% -15% Prof. Dr. Rainer Maure -10% => Current account surplus gap = 13 % of GDP! -15% Constant Intern. Net Debt-to-GDP Ratio Current Account Surplus (right scale) Actual Current Account Surplus Source: Eurostat, Own Calculations - 19 - © www.rainer-maurer.com The Eurozone Debt Crisis 2010 Portugal 15% Current Account Surplus Gap Percent of GDP 15% 10% 10% 5% 5% 0% 0% Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 -5% -5% Current account surplus gap = 18,5 % of GDP! © RAINER MAURER, Pforzheim -10% -10% -15% Prof. Dr. Rainer Maure -15% Constant International Net Debt-to-GDP Ratio Current Account Surplus Actual Current Account Surplus Source: Eurostat, Own Calculations - 20 - © www.rainer-maurer.com The Eurozone Debt Crisis 2010 Ireland 15% Current Account Surplus Gap Percent of GDP 15% 10% 10% Current account surplus gap = 15 % of GDP! 5% 5% 0% Jan. 99 0% Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 -5% -5% © RAINER MAURER, Pforzheim -10% -10% -15% Prof. Dr. Rainer Maure -15% Constant International Net Debt-to-GDP Ratio Current Account Surplus Actual Current Account Surplus Source: Eurostat, Own Calculations - 21 - © www.rainer-maurer.com The Eurozone Debt Crisis 2010 Greece 15% Current Account Surplus Gap Percent of GDP 15% 10% 10% 5% 5% 0% 0% Jan. 99 Jan. 00 Jan. 01 © RAINER MAURER, Pforzheim -5% Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 -5% Current account surplus gap = 25 % of GDP! -10% -10% -15% -15% Prof. Dr. Rainer Maure Constant International Net Debt-to-GDP Ratio Current Account Surplus Actual Current Account Surplus Source: Eurostat, Own Calculations - 22 - © www.rainer-maurer.com The Eurozone Debt Crisis 2010 Interest Rates (Average: Sept. 2009 - May 2010) and Constant International Debt Position-to-GDP Ratio Primary Current Account Gap (Average: Jan. 2009 - Aug. 2009) 6,0% Nominal Interest Rates 10Y Bonds Correlation Coefficient: 70,1% Greece The larger the current account gap, the higher the risk premium! 5,5% 5,0% Ireland Cyprus 4,5% Malta © RAINER MAURER, Pforzheim Italy Belgium Luxembourg Austria Finland3,5% Netherlands Portugal Slovakia 4,0% Slovenia Spain United Kingdom France Germany Constant IDP-to-GDP Ratio Current Account Surplus Gap 3,0% -15% -10% Source: Eurostat, Own Calculations Prof. Dr. Rainer Maure -5% 0% 5% 10% 15% - 20% 23 - © www.rainer-maurer.com The Eurozone Debt Crisis 2010 ➤ The situation is precarious! ➤ How to get out of this??? ➤ To help countries like Greece, Portugal, Spain and Ireland their " Current Account Gap" must be reduced: B Y Bt Yt it dYt dt Yt Dt Bt Yt Yt © RAINER MAURER, Pforzheim o Prof. Dr. Rainer Maure Depressed - 25 EMU The Eurozone Debt Crisis 2010 ➤ How to get out of this??? ➤ Special problem of indebted countries, which are member states of a monetary union: 1. They have no own currency they can depreciate to improve their current account: e$€ ↓ => P€ e$€ ↓ < P$ => ( EX ↑ – IM ↓ ) ↑ © RAINER MAURER, Pforzheim Reduction of current account gap! 2. They have no own currency to inflate away debt! Prof. Dr. Rainer Maure - 26 - Digression: How to "inflate away" government debt ??? The present value (=PVt,T=market value) of government debt with a face value of 1€ is given by the formula: PVt ,T The Dark Corners of Fiscal Policy zT 1 1 1 T T ( 1 i ) i ( 1 i ) t ,T t ,T t ,T If the market interest rate it,T=2% is equal to fixed interest rate of government debt zt,T =2%, the market value is equal to the face value = 1€: PVt ,T 2% T 1 1 1 T T (1 2% t ,T ) (1 2% t ,T ) 2% t ,T 1 © RAINER MAURER, Pforzheim If an increase of inflation by 3% increases the nominal market interest rate (=real interest rate + inflation rate) by 3% and the average maturity of government debt is T=10 years, the market value of government debt falls by nearly one quarter: => PVt ,T Prof. Dr. Rainer Maurer Maure 2% T 1 1 1 10 10 (1 5% t ,T ) (1 5% t ,T ) 5% t ,T Create a 0,77 little bit inflation and buy back - 27 - The Eurozone Debt Crisis 2010 ➤ How to get out of this??? ➤ Special problem of member states of a monetary union: 3. Leaving the monetary union will cause the countries debt position to explode !!! ◆ If Greece would leave the eurozone: Its new currency (the Neodrachmae) will depreciate against the Euro: e€Neodramae ↓ ↓ Prof. Dr. Rainer Maure The Greek debt measured in Neodramae will grow in case of a depreciation: DNeodramae = ( D€ / e€Neodramae↓ ) ↓ © RAINER MAURER, Pforzheim However, Greek government bonds (as well as private debt) are denominated in Euro D€ ! - 28 - The Eurozone Debt Crisis 2010 ➤ How has it come to this? ■ The EMU is a monetary union across countries which have asynchronous business cycles: GDP Gaps of ECU Member States and the USA © RAINER MAURER, Pforzheim (Trend Deviation of GDP in Percent of Trend measured by Hodrick-Prescott-Filter) 0,020 0,015 0,010 0,005 2009Q03 2009Q01 2008Q03 2008Q01 2007Q03 2007Q01 2006Q03 2006Q01 2005Q03 2005Q01 2004Q03 2004Q01 2003Q03 2003Q01 2002Q03 2002Q01 -0,005 -0,010 -0,015 GDP Gap = Actual GDP minus trend GDP in % of trend GDP -0,020 Germany (left scale) USA (left scale) Standard Deviation without Cyprus, Malta, Slovenia, Slovakia, USA (right scale) Source: Eurostat, Own Prof. Dr. Rainer Maure 2001Q03 2001Q01 2000Q03 0,000 2000Q01 8% 7% 6% 5% 4% 3% 2% 1% 0% -1% -2% -3% -4% -5% -6% -7% -8% www.rainer-maurer.com - 29 - The Eurozone Debt Crisis 2010 ➤ How has it come to this? ■ As a result, inflation rates across the EMU member state are typically quite different: GDP Price Deflator Relative to Germany Indices Relative to Germany (1999 = 100%) 130% 125% 120% 115% 110% Euro area (16 countries) Source: EU Commission, AMECO, Own Calculations Prof. Dr. Rainer Maure Ireland Greece Spain 2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 100% 1999 © RAINER MAURER, Pforzheim 105% Portugal www.rainer-maurer.com - 30 - The Eurozone Debt Crisis 2010 ➤ How has it come to this? ■ The European Central Bank can set only one main refinancing rate. ■ Therefore, after the start of the EMU, nominal interest rates across the eurozone converged. ■ However, convergence of nominal interest rate and different country-specific interest rates causes a divergence of real interest rates! Real Interest Nominal Interest Inflation © RAINER MAURER, Pforzheim r i => Countries with a high inflation rate have low real interest rates! Prof. Dr. Rainer Maure Countries with a low inflation rate have high real interest rates! - 31 - The Eurozone Debt Crisis 2010 ➤ How has it come to this? ■ Convergence of nominal interest rate & divergence of real interest rates: Variance Coefficients across the 12 EMU Founding Member States 1,5% 1,3% 1,1% 0,9% 0,7% 0,5% © RAINER MAURER, Pforzheim 0,3% Prof. Dr. Rainer Maure 0,1% Jan. 97 Jan. 98 Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 -0,1% Source: Eurostat, Own Calculations Nominal Interest Rates for 10-Year Government Bonds Inflation Rates (HCPI) Real Interest Rates for 10-Year Government Bonds © www.rainer-maurer.com - 32 - The Eurozone Debt Crisis 2010 ➤ How has it come to this? ■ Real interest rates compared to Germany: Real Interest Rates for 10 Years Government Bonds (based on BIP-Deflator) 9,0% 8,0% 7,0% 6,0% 5,0% 4,0% 3,0% 2,0% © RAINER MAURER, Pforzheim 1,0% 0,0% Jan. 97 Jan. 98 Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 -1,0% -2,0% -3,0% -4,0% Germany Prof. Dr. Rainer Maure Source: Eurostat, Own Calculations Spain Greece Ireland Portugal © www.rainer-maurer.com - 33 - The Eurozone Debt Crisis 2010 ➤ How has it come to this? ■ Real interest rates and net international debt position: December 2009 Accumulated Net Debt Position in Percent of GDP and Average Real Interest Rate from Januar 1999 to December 2009 120% Net Debt Position in % of GDP in % of GDP 100% Portugal Spain Greece 80% Ireland 60% 40% Italy © RAINER MAURER, Pforzheim 20% 0% 1,3% France Austria Finland 1,5% -20% 1,7% 1,9% 2,1% 2,3% 2,5% Netherlands Belgium 2,7% Real Interest Rate Germany -40% Prof. Dr. Rainer MaureQuelle: Eurostat, Eigene Berechnungen © www.rainer-maurer.com - 34 - The Eurozone Debt Crisis 2010 ➤ How has it come to this? ■ Inflation rates and net international debt position: December 2009 Accumulated Net Debt Position in Percent of GDP and Average HCPI Price Index from Januar 1999 to December 2009 120% Net Debt Position in % of GDP in % of GDP 100% Portugal Spain Greece 80% Ireland 60% 40% Italy © RAINER MAURER, Pforzheim 20% 0% 1,4% France Finland Austria 1,6% 1,8% Inflation Rate 2,0% 2,2% 2,4% 2,6% 2,8% 3,0% 3,2% Netherlands -20% Germany Belgium -40% Prof. Dr. Rainer MaureQuelle: Eurostat, Eigene Berechnungen © www.rainer-maurer.com - 35 - The integrated EMU capital market is in equilibrium, while The Eurozone Debt Crisis 2010 there is a disequilibrium in single countries! ➤ How has it come to this? ■ Consequently, high inflation countries experienced on average lower real interest rates than low inflation countries: r r S(Y) S(Y) Excess Supply rL * r* © RAINER MAURER, Pforzheim Excess Demand Prof. Dr. Rainer Maure rH* Low inflation country: rL*= i*- πL I(Y) S, I I(Y) High inflation country: S, I rH*= i*- πH - 36 - The Eurozone Debt Crisis 2010 ➤ How has it come to this? ■ Countries with high inflation rates built up a net international ■ debt position. Countries with low inflation rates built up a net international wealth position. International Net Debt Position of Eurozone Debtor and Creditor Countries 1500 Bn. Euro 1000 500 0 Jan. 98 Jan. 99 Jan. 00 Jan. 01 Jan. 02 Jan. 03 Jan. 04 Jan. 05 Jan. 06 Jan. 07 Jan. 08 Jan. 09 Jan. 10 © RAINER MAURER, Pforzheim -500 -1000 -1500 Sum of Net International Debt Position of Spain, Greece, Ireland, Portugal Sum of Net International Debt Position of Germany, Belgium, Luxembourg, Netherlands Prof. Dr. Rainer Maure Source: Eurostat, Own Calculations © www.rainer-maurer.com - 37 - 4.2. Financial Market Crises 4.2.5. The Eurozone Debt Crisis 2010 ➤ How has it come to this? Consequently, the eurozone debt crisis is not by chance! ■ It is caused by a design faulty of the EMU! ■ What can be done to built a more stable EMU? © RAINER MAURER, Pforzheim ■ Prof. Dr. Rainer Maure - 38 -