Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Production for use wikipedia , lookup

Economic growth wikipedia , lookup

Business cycle wikipedia , lookup

Fei–Ranis model of economic growth wikipedia , lookup

Ragnar Nurkse's balanced growth theory wikipedia , lookup

Gross fixed capital formation wikipedia , lookup

Uneven and combined development wikipedia , lookup

Economic democracy wikipedia , lookup

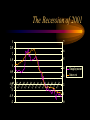

Real Business Cycles Supply Side Economics The Real Economy • Neoclassical (Supply Side) Economics suggests that business cycles are the result of random disturbances to productivity. The Real Economy • Neoclassical (Supply Side) Economics suggests that business cycles are the result of random disturbances to productivity. • The initial impact takes place in labor markets (employment/output) The Real Economy • Neoclassical (Supply Side) Economics suggests that business cycles are the result of random disturbances to productivity. • The initial impact takes place in labor markets (employment/output) • Capital markets determine the impact on future labor markets (Investment today affects the capital stock in the future) Example: A negative supply shock • Consider an unanticipated rise in oil prices (permanent enough to impact capital investment). 28 24 20 16 12 8 4 0 0 100 200 300 400 500 Example: A negative supply shock • Consider an unanticipated rise in oil prices (permanent enough to impact capital investment). • This drop in productivity lowers labor demand resulting in lower wages, lower employment, and lower output 28 24 20 16 12 8 4 0 0 100 200 300 400 500 Example: A negative supply shock • Now, moving to capital markets, the drop in productivity ( from lower employment as well as high oil prices) lowers investment demand 20 16 12 8 4 0 0 100 200 300 400 500 Example: A negative supply shock • Now, moving to capital markets, the drop in productivity ( from lower employment as well as high oil prices) lowers investment demand • Lower investment demand causes interest rates, investment, and savings to fall 20 16 12 8 4 0 0 100 200 300 400 500 Investment and the Capital Stock • Recall that investment is defined as the purchase of new capital goods. Investment and the Capital Stock • Recall that investment is defined as the purchase of new capital goods. • Capital goods are constantly wearing out (depreciation). Therefore, positive investment is needed to maintain the current capital stock. Investment and the Capital Stock • Recall that investment is defined as the purchase of new capital goods. • Capital goods are constantly wearing out (depreciation). Therefore, positive investment is needed to maintain the current capital stock. • The capital stock evolves according to K (Future) = (1-dep)*K + I Investment and the Capital Stock • Recall that investment is defined as the purchase of new capital goods. • Capital goods are constantly wearing out (depreciation). Therefore, positive investment is needed to maintain the current capital stock. • The capital stock evolves according to K (Future) = (1-dep)*K + I • A large enough drop in current investment causes the capital stock to shrink. Example: A negative supply shock • With a lower capital stock, labor productivity drops (capital and labor are complements) causing another drop in labor demand 28 24 20 16 12 8 4 0 0 100 200 300 400 500 Example: A negative supply shock • With a lower capital stock, labor productivity drops (capital and labor are complements) causing another drop in labor demand • Therefore, wages, employment, and output continue to fall 28 24 20 16 12 8 4 0 0 100 200 300 400 500 Example: A negative supply shock • Lower employment causes another drop in capital investment (not as big as the previous decline – the capital stock is lower than it was before) 20 16 12 8 4 0 0 100 200 300 400 500 Example: A negative supply shock • Lower employment causes another drop in capital investment (not as big as the previous decline – the capital stock is lower than it was before) • Interest rates and investment continue to fall 20 16 12 8 4 0 0 100 200 300 400 500 Example: A Negative supply shock 1 0.9 0.8 0.7 0.6 0.5 0.4 0.3 0.2 0.1 0 Employment Output Wages Investment Capital 0 Example: A Negative supply shock 0 -1 -2 -3 -4 -5 -6 -7 0 1st Qtr Employment Output Wages Investment Capital Example: A Negative supply shock 0 -1 0 1st Qtr 2nd Qtr -2 -3 -4 -5 -6 -7 -8 -9 Employment Output Wages Investment Capital Example: A Negative supply shock 0 -1 0 1st Qtr 2nd Qtr 3rd Qtr -2 -3 -4 -5 -6 -7 -8 -9 Employment Output Wages Investment Capital Example: A Negative supply shock 0 0 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr -2 -4 -6 -8 -10 -12 Employment Output Wages Investment Capital Example: A Negative supply shock 0 0 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr 5th Qtr -2 -4 -6 -8 -10 -12 Employment Output Wages Investment Capital Example: A Negative supply shock 6 4 2 0 -2 0 -4 -6 -8 -10 -12 -14 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr 5th Qtr 6th Qtr Employment Output Wages Investment Capital Example: A Negative supply shock 8 6 4 2 0 -2 0 -4 -6 -8 -10 -12 -14 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr 5th Qtr 6th Qtr 7th Qtr Employment Output Wages Investment Capital Example: A Negative supply shock 8 6 4 2 0 -2 0 -4 -6 -8 -10 -12 -14 1st Qtr 2nd Qtr 3rd Qtr 4th Qtr 5th Qtr 6th Qtr 7th Qtr 8th Qtr Employment Output Wages Investment Capital Example: A Negative supply shock 8 6 4 2 0 -2 0 -4 -6 -8 -10 -12 -14 1st 2nd 3rd 4th 5th 6th 7th 8th 9th Qtr Qtr Qtr Qtr Qtr Qtr Qtr Qtr Qtr Employment Output Wages Investment Capital Example: A negative supply shock 8 6 4 2 0 -2 0 -4 -6 -8 -10 -12 -14 1st 2nd 3rd 4th 5th 6th 7th 8th 9th 10th Qtr Qtr Qtr Qtr Qtr Qtr Qtr Qtr Qtr Qtr Employment Output Wages Investment Capital -1 -2 -3 -4 12/1/02 8/1/02 4/1/02 12/1/01 8/1/01 4/1/01 12/1/00 8/1/00 4/1/00 12/1/99 8/1/99 4/1/99 The Recession of 2001 3 2 1 0 GDP Consumption Productivity -5 Jan-03 Sep-02 May-02 Jan-02 Sep-01 May-01 Jan-01 Sep-00 May-00 Jan-00 Sep-99 May-99 -10 Jan-99 The Recession of 2001 25 20 15 10 Investment 5 0 1/ 1/ 99 5/ 1/ 9 9/ 9 1/ 99 1/ 1/ 0 5/ 0 1/ 00 9/ 1/ 0 1/ 0 1/ 01 5/ 1/ 0 9/ 1 1/ 01 1/ 1/ 0 5/ 2 1/ 02 9/ 1/ 0 1/ 2 1/ 03 5/ 1/ 03 The Recession of 2001 3 7 2.5 2 6 1.5 1 0.5 0 -0.5 -1 -1.5 -2 5 4 3 2 1 0 Employment Interest What caused the 2001 recession? What caused the current recession? • Collapse of the stock market • The Dow dropped 30% from its Jan 14, 2000 high of $11,722 • The Nasdaq dropped 75% from its March 10, 2000 high of $5,132 • The S&P 500 dropped 45% from its July 17, 2000 high of $1,517 What caused the current recession? • Collapse of the stock market • The Dow dropped 30% from its Jan 14, 2000 high of $11,722 • The Nasdaq dropped 75% from its March 10, 2000 high of $5,132 • The S&P 500 dropped 45% from its July 17, 2000 high of $1,517 • Y2K/Capital Overhang What caused the current recession? • Collapse of the stock market • The Dow dropped 30% from its Jan 14, 2000 high of $11,722 • The Nasdaq dropped 75% from its March 10, 2000 high of $5,132 • The S&P 500 dropped 45% from its July 17, 2000 high of $1,517 • Y2K/Capital Overhang • A sharp rise in oil prices (oil prices doubled in late 1999) What caused the current recession? • Collapse of the stock market • The Dow dropped 30% from its Jan 14, 2000 high of $11,722 • The Nasdaq dropped 75% from its March 10, 2000 high of $5,132 • The S&P 500 dropped 45% from its July 17, 2000 high of $1,517 • Y2K/Capital Overhang • A sharp rise in oil prices (oil prices doubled in late 1999) • Enron/Accounting scandals What caused the current recession? • Collapse of the stock market • The Dow dropped 30% from its Jan 14, 2000 high of $11,722 • The Nasdaq dropped 75% from its March 10, 2000 high of $5,132 • The S&P 500 dropped 45% from its July 17, 2000 high of $1,517 • • • • Y2K/Capital Overhang A sharp rise in oil prices (oil prices doubled in late 1999) Enron/Accounting scandals Terrorism/SARS