Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Bretton Woods system wikipedia , lookup

Currency war wikipedia , lookup

International monetary systems wikipedia , lookup

Foreign exchange market wikipedia , lookup

Foreign-exchange reserves wikipedia , lookup

Purchasing power parity wikipedia , lookup

Fixed exchange-rate system wikipedia , lookup

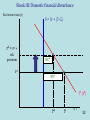

Economics 122a Open-Economy Macroeconomics Topics: 1. International issues 2. Balance of payments accounting 3. Saving and investment in the open economy 4. Determination of the exchange rate What are the enduring international issues? • International trade and investment increase productivity and growth (standard trade and capital theory) • International competition heightens the process of “creative destruction” and is resisted by those why are hurt (non-standard trade theory) • International spillovers (standard macro) – lead to exports and imports and affect output and employment – lead to capital flows and affect exchange rates, relative prices, interest rates, asset prices, and wealth • Markets cannot manage themselves. This is why nations need active rules, institutions, and policies: – Foreign economic policies on trade and finance – To coordinate policy – International institutions to help prevent destructive “prisoners’ dilemma” outcomes on trade, capital flows, war, … 3 Trade and Growth IMF What are the today’s issues? What was on the agenda at the Pittsburgh G-20 Summit?* • The Great Recession • Fight off protectionism – US probably the worst sinner with “buy America” and recent “tires” case; CO2 trade sanctions. • International spillovers – Coordinate stimulus plans and savings-investment balance – Climate change • Markets cannot manage themselves. – IMF, World Bank, G-20 – Coordinate risk and regulatory standards for banks * See http://www.whitehouse.gov/the_press_office/Leaders-statement-on-thePittsburgh-summit/ 5 Measuring international flows Essential balancing property of Balance of Payments Current Account Financial Account Net Balance A -A 0 7 Balance of Payments v. Real Goods and Services 1. Macro: NX = Net Exports = exports goods and services – imports g&s 2. Current account: Current account = NX + locational adjustments (domestic v. national product) + unilateral transfers (not current goods/services) Difference = locational stuff + transfers 8 Balance of Payments, 2008 Goods and services Exports Imports Net income of foreign investments Unilateral transfers, net -696 1,827 -2,523 118 -128 Balance on Current Account Net change in assets Central banks Other Statistical discrepancy -706 506 482 52 Balance on Financial Account Net exports * I have omitted "capital account," which is trivial in $ terms. 200 706 -696 Openness/globalization: Trade Imports, exports (% of GDP) 20 16 Rising trend 12 8 4 Imports Exports 0 1950 1960 1970 1980 1990 2000 10 Savings and Investment in the Open Economy ACCOUNTING: Y = output = C + I + G + NX Y = income = Yd + T + Sb = C + Spers + Sb + T = C + Spriv+ T → I + NX = Spriv + Sgov = Sn or NX = Spriv + Sgov – I = Sn – I FINANCIAL COUNTERPART: Net domestic saving = net foreign investment = lending abroad = ΔNFA = financial account deficit that corresponds to the current account surplus 11 Overview of analysis 1. 2. 3. 4. Savings-investment accounting S, I, and NX determination How S, I, and NX determine real exchange rate Small and large open economies 12 Classical Open Economy Equilibrium Now study open-economy equilibrium: 1. Classical economy • Full employment, flex w and p; this implies that domestic output is at potential 2. Small open economy • Too small to affect goods prices or financial markets 3. Mobile financial capital • free flow of funds among countries • Investors therefore compare domestic and foreign interest rates (rd, rw ) • In small economy, rd = rw = world interest rate 13 Recall Closed Economy S and I equilibrium Real interest rate (r) Sn = Spriv + (T-G) r* Id (r) I* S, I 14 Open Economy S and I equilibrium Real interest rate (r) Sn = Spriv + (T-G) Net exports > 0 r*=rW China, Japan, OPEC today Id (r) I* S, I 15 Open Economy S and I equilibrium Real interest rate (r) Sn = Spriv + (T-G) US today; LDCs classically rW Net exports < 0 Id (r) I* S, I 16 Shock I: Increase in world interest rate Real interest rate (r) rW’ rW S = Sp + (T-G) NX** NX* Id (r) I** I* S, I 17 Shock II: Increase in G Real interest rate (r) S* S** NX*>0 rW NX**<0 Id (r) I* S, I 18 “International money”: Foreign exchange rates Financial Globalization 140 Assets as % of US GDP 120 US assets abroad (% US GDP) ROW assets in US (% US GDP) 100 80 60 40 20 0 1975 1980 1985 1990 1995 2000 2005 2010 Exchange rates Foreign-exchange rates are the relative prices of different national monies or currencies. Convention in Econ 122: Nominal exchange rate • exchange rates = amount of foreign currency per unit of domestic currency. • Think Japanese Yen: 100 yen to $. 21 Terminology For market-determined exchange rates: • An appreciation of a currency is when the value of the currency rises – e or R rises • A depreciation of a currency is when the value of the currency falls – e or R falls For fixed exchange rates: • Price set by government is the “parity.” • A revaluation is an increase in the official parity. • A devaluation is a decrease in the parity. 22 Index of US nominal exchange rate (e) Appreciation Nominal exchange rate against 30 major countries 140 January 1997 = 100 120 100 80 60 40 1970 1975 1980 1985 1990 1995 2000 2005 2010 Depreciation 23 The Transmission Mechanism in Open Economy Macro We saw that changes in domestic saving and investment, or changes in world interest rates, or domestic risk premiums would affect net exports. How does that happen? Through the adjustment of the real exchange rate. Let see how. 24 Real exchange rates Real exchange rate, R [Mankiw uses ε) R = nominal exchange rate corrected for relative prices R = e × (p d / p f ) = p d / (p f / e) = domestic prices/foreign prices in a common currency Note: If you calculate the rate of growth of R, you get rate of real rate of nominal domestic foreign appreciation appreciation inflation rate inflation rate Example of car exchange rate: 100 Yen/$; Toyota = 2,000,000Y; Ford = $20,000; R = 100 * 20000/2000000 = 1 Toyota/Ford 25 Real exchange rate, US dollar, against broad group of currencies 120 110 75 80 85 90 95 Flight to safety in financial panic Internet bubble spills over Dollar bubble 1980s from high interest rates Real exchange rate of $ relative to major currencies (R) Appreciation 130 100 90 80 00 05 10 Depreciation 26 We saw last time that changes in the domestic S-I balance led to changes in NX (the trade balance). We need next to understand the macroeconomic mechanism by which this occurs. We will see that this operates through changes in the real exchange rate, which leads to changes in the relative prices of foreign and domestic goods. The important condition is: NX(R) = Spriv + Sg – I(rw) Net exports and the real exchange rate Real exchange rate (R) The only new relationship is NX(R): – Real deprecation (R ↓) lowers the price of exports in foreign markets and raises import P in domestic markets. – This raises exports and lowers imports; raising NX. – Hence NX’(R) < 0 ……………………….. R* NX(R) NX* Using the NX curve and S-I curves, we can see how real exchange rate is determined. 0 NX Net exports and the real exchange rate Real exchange rate (R) Why is NX so negative for US? R* NX(R) NX* 0 NX 29 Have two behavioral relationships: (1) NX and (2) net savings. R and NX are determined as the equilibrium of these two functions. Sn-I(rw) R Savings-investment and the determination of the real exchange rate: NX(R) = Sn-I(rw) R* E* NX(R) NX* 0 S-I, NX 30 Political crisis and a domestic risk premium Question for class: • Assume that there is a political crisis in Slobovia. • Investors now require a risk premium for investing there (relative to the rest of the world • What happens? 31 Shock III: Domestic financial disturbance Real interest rate (r) S = Sp + (T-G) rd = rW + risk premium rW NX** NX* Id (rd) I** I* S, I 32 Why does fiscal tightening lead to a lower trade deficit? 33 Fiscal tightening (S-I(rw))* (S-I(rw))** R Fiscal policy: G↓→ net S ↑ → R ↓→ NX ↑ E* E** NX(R) NX* 0 NX** S-I, NX 34 Impact of protectionism Protectionism (S-I(rw)) R R** NX(R)’ R* NX(R) NX*=NX** 0 S-I, NX 36 Now analyze large open economy Large Open Economy: - Country large enough to affect world financial markets - Domestic assets imperfect substitutes for foreign assets. - Because imperfect substitutes, domestic r differs from foreign r (rd ≠ rw) Analysis Goods markets: (1) NX(R) = Sn – I(rd) Financial market equilibrium: CF = net financial investment abroad = - financial surplus (2) CF = CF(rd, rw). In analysis, we suppress rw Notes that capital flows in if domestic interest rates rise CF’(rd) < 0. Equilibrium comes when (1) and (2) equilibrate the balance of payments: (3) NX(R) = CF(rd) = Sn – I(rd) In our diagrams below, we reorganize and use: (4) I(rd) + CF(rd) = Sn = Spriv + Sg 37 rd Domestic interest rate (rd) Sn rd* I(rd)+CF(rd) CF(rd) CF* CF 0 S, I,CF Real exchange rate, R R* NX(R) NX* NX 0 Bernanke’s surprising theory of why the US deficit is so high “I will argue that over the past decade a combination of diverse forces has created a significant increase in the global supply of saving--a global saving glut--which helps to explain both the increase in the U.S. current account deficit and the relatively low level of long-term real interest rates in the world today.” (Bernanke, 2005) Global savings glut: Global effect Real interest rate (r) Sworld * Sworld ** r* r** Id (r) I* I** S, I 40 rd Domestic interest rate (rd) Sn rd* CF(rd) I+CF CF 0 S, I,CF Effect on US of global savings glut: are effects of increased Chinese saving R R* NX(R) NX* NX 0 rd Domestic interest rate (rd) S rd* CF(rd) I+CF CF 0 S, I,CF R Bernanke’s “world savings glut” -Current situation is one in which rest of world has savings glut (particularly China, Japan, and oil exporting countries accumulating $ reserves). - This increases inflows to US. - This is leading to low world and US real interest rates and to the large US trade deficit. R* NX(R) NX* NX 0 Here are the basic data .01 16 NX/GDP ( <---- ) .00 14 -.01 12 -.02 10 -.03 8 -.04 6 Net exports/GDP 10-year T-bond rate -.05 -.06 80 82 84 86 88 90 92 4 T-bond rate (----> ) 94 96 98 00 02 04 2