Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

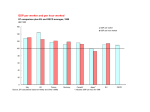

LEZIONE 1 Struttura ed evoluzione dei sistemi tributari Tassazione internazionale delle società - PARTE I Clamep 8 crediti – 50 ore 27.9.2010-6.11.2010 Principali fonti OECD, Revenue Statistics 1965-2008, 2009 Edition http://www.oecd.org/document/4/0,3343,en_2649_34533_41407428 _1_1_1_1,00.html “This annual publication presents a unique set of detailed and internationally comparable tax revenue data in a common format for all OECD member countries from 1965 onwards. It also describes a conceptual framework to define which government receipts should be regarded as taxes and to classify different types of taxes. The 2009 edition includes a Special Feature titled ‘Changes to the guidelines for attributing revenues to levels of government’. 2 Eurostat and European Commission, Taxation trends in the European Union, 2010 edition http://ec.europa.eu/taxation_customs/resources/documents/taxatio n/gen_info/economic_analysis/tax_structures/2010/2010_full_text _en.pdf “This is the fourth issue of 'Taxation Trends in the European Union', an expanded and improved version of a previous publication, 'Structures of the taxation systems in the European Union'. The objective of the report remains unchanged: to present a complete view of the structure, level and trends of taxation in the Union over a medium- to long-term period. Taxation is at the heart of citizens' relationship with the State. Not only government experts and academics, but also citizens regularly address us questions about taxation levels in the EU and on how Member States compare with each other; this report, which is published annually, is one way of answering these questions…. ….. This publication presents time series of tax revenue data from National Accounts for the twenty-seven Member States Norway, and for the first time - Iceland. It provides a breakdown of taxes according to different classifications: by type of taxes (direct taxes, indirect taxes, social contributions), by level of government, and by economic function (consumption, labour, capital). It also compiles data for the sub-group of environmental taxes.” 3 OECD Revenue statistics Total tax revenue as percentage of GDP (p. 19) These ratios are calculated by expressing total tax revenues as a percentage of GDP at current market prices. Tax ratios vary considerably between countries, as does their evolution over time. In 2007, two countries in the European region – Denmark and Sweden – had tax ratios of 45 per cent or more of GDP. In contrast, seven countries – Japan, Korea, Mexico, the Slovak Republic, Switzerland, Turkey and the United States – had tax ratios of below 30 per cent. In 2007, the tax ratio in the OECD area as a whole (unweighted average) remained stable at 35.8 per cent (see Table A), 0.2 percentage point below the highest recorded level in 2000. Overall tax ratios rose in fourteen OECD member countries whereas they fell in fifteen countries. In three countries, the increases in tax ratios were one percentage point of GDP or more, the highest being in Hungary (2.4 points). The reductions in the ratio were generally by less than one percentage point. 4 OECD Revenue statistics Total tax revenue as percentage of GDP Taking a long term view and focusing on major OECD areas, in Canada, Mexico and the United States the tax-take from GDP inched up from an (unweighted) average of 25.2 per cent in 1965 to 26.5 per cent in 2007. In OECD Europe, by contrast, between 1965 and 2007 the overall tax/GDP ratio increased from 26.2 per cent to 38.0 per cent. In OECD Pacific, the corresponding figures were from 21.1 per cent to 30.4 per cent. The trend towards higher tax levels over this period reflects the sizeable increase of public sector outlays in almost all industrialised countries, with recourse of governments to alternative ways to finance their spending – non-tax revenues, borrowing and printing money – being limited for a variety of reasons. 5 Total tax ratio as percentage of GDP, 2007 (page 40) 6 Changes in tax to GDP ratio (in percentage points) (page 44) 1995-2007 7 OECD Revenue statistics Tax structure Tax structures are measured by the share of major taxes in total tax revenue. While, on average, tax levels have been rising, the share of main taxes in total revenues – the tax structure or tax “mix” – has been remarkably stable. Nevertheless, several trends have emerged, as shown in Table C. In 2007, personal income taxes had ceased to be the largest single source of revenue for OECD countries as a whole. Their share had shrunk to 25 per cent of total taxes from 30 per cent in the early 1980s (unweighted averages). The variation in the share of the personal income tax between countries is considerable. In 2007, it ranged from a low of 9 per cent in the Slovak Republic and 12 per cent in the Czech Republic to 42 per cent in New Zealand and 52 per cent in Denmark 8 OECD Revenue statistics Tax structure Over the last decade, the share of the corporate income tax in the tax mix has increased by about 3 percentage points of total taxes (unweighted average), to exceed the 9 per cent level of the 1960s. As with the personal income tax, the share of the corporate income tax in total tax revenues shows a considerable spread (see Table 13 in Section II.A), from 6 per cent (Austria) to 23 per cent (Australia) and 26 per cent (Norway). Apart from the spread in statutory rates of the corporate income tax, these differences are at least partly explained by institutional factors or the exploitation of mineral deposits – the degree to which firms in a country are incorporated, taxation of oil revenues – and the erosion of the corporate income tax base, for example as a consequence of generous depreciation schemes and other instruments to postpone the taxation of earned profits. Taken together, taxes on personal and corporate incomes remain the most important source of revenues used to finance public spending in half of all OECD countries, and in eight of them – Australia, Canada, Denmark, Iceland, New Zealand, Norway, Switzerland and the United States – the share of income taxes in the tax mix exceeds 45 per cent 9 OECD Revenue statistics Tax structure The declining share of the personal income tax for OECD countries taken together was paralleled by the growing share of social security contributions, which by 2007 accounted for 25 per cent of total tax revenues. In seven countries – Austria, the Czech Republic, France, Germany, Greece, the Netherlands and the Slovak Republic – social security contributions are now the largest single source of general government revenue (see Table 7 in Section II.A). The expanding share of contributions in the tax mix (up from 18 per cent of total revenues in 1965) seems to be directly linked to the upward pressure on aggregate benefit spending resulting from ageing populations and rising government expenditure on health care programmes. In 2007, the share of social security contributions in the tax mix varied from 2 per cent (Denmark) to 40 per cent (the Slovak Republic) and 44 per cent (Czech Republic). Australia and New Zealand report no revenue from social security contributions (see Table 15 in Section II.A). OECD countries also show a wide variety in the relative proportions paid by employees and employers (see Tables 17 and 19 in Section II.A). 10 OECD Revenue statistics Tax structure Between 1965 and 2007, the share of taxes on immovable property, net wealth plus property and legal transactions fell significantly, from 8 per cent to 6 per cent of aggregate tax revenues, possibly in part as a result of voter resistance against such highly “visible” taxes and a failure to maintain up-to-date the inflation-adjusted valuation of the tax base. 11 OECD Revenue statistics Tax structure The share of taxes on consumption (general consumption taxes plus specific consumption taxes) fell from 36 to 30 per cent between 1965 and 2007. But in addition the mix of taxes on goods and services has fundamentally changed. A fast growing revenue source has been general consumption taxes, especially the value-added tax (VAT) which is now found in twenty-nine of the thirty OECD countries. General consumption taxes presently produce 19 per cent of total tax revenue, compared with only 14 per cent in the mid-1960s. In fact, the substantially increased importance of the valueadded tax has everywhere served to counteract the diminishing share of specific consumption taxes, such as excises and custom duties. Between 1965 and 2007 the share of specific taxes on consumption (mostly on tobacco, alcoholic drinks and fuels, including some newly introduced environment-related taxes) was halved. Rates of taxes on imported goods were considerably reduced everywhere, reflecting a global trend 12 to remove trade barriers. Taxation trends in the EU (2010 ed.) Nel 2008 si inizia a sentire l’effetto della crisi “The effects of the global economic and financial crisis have hit the EU with increasing force from the second half of 2008, which is the last year for which we possess tax revenues data with the high level of disaggregation needed for the purposes of this report. This means that our revenue data refer only to the beginning of the recession, and not to its entire development. Developments in 2008 were also marked by the circumstance that many countries still recorded satisfactory growth in the first six months of 2008, so that the year as a whole is made up of two rather uneven halves. Nevertheless, as we shall see, the recession had a clear impact on revenues already in 2008, not only on capital taxes (typically highly sensitive to the pace of growth), but also on consumption taxes, which are usually expected to be somewhat more resilient in a slowdown; in particular, consumption tax revenue shrunk more than the volume of consumption itself. The overall revenue impact was a decline by 0.4 percentage points of GDP, compared with the year before, for capital taxes, while revenue from consumption taxes contracted by 0.3 points of GDP. 13 In media, la UE è un area a tassazione elevata “The European Union is, taken as a whole, a high tax area. In 2008, the overall tax ratio, i.e. the sum of taxes and social security contributions in the 27 Member States (EU-27) amounted to 39.3 % in the GDP-weighted average, more than one third above the levels recorded in the United States and Japan. The tax level in the EU is high not only compared to those two countries but also compared to other economies in general; among the major non-European OECD members, only New Zealand has a tax ratio that exceeds 34.5 % of GDP(2). As for less developed countries, they are typically characterised by relatively low tax ratios. The high EU overall tax ratio is not new, dating back essentially to the last third of the 20th century. In those years, the role of the public sector became more extensive, leading to a strong upward trend in the tax ratio in the 1970s, and to a lesser extent also in the 1980s and early 1990s. In the late 1990s, first the Maastricht Treaty and then the Stability and Growth Pact encouraged EU Member States to adopt a series of fiscal consolidation packages. In some Member States, the consolidation process relied primarily on restricting or scaling back primary public expenditures, in others the focus was rather on increasing taxes (in some cases temporarily)…. 14 Ma c’è una grande variabilità fra paesi Despite the high average level of the overall tax ratio, eleven Member States display ratios below the 35 % mark, highlighting that differences in taxation levels across the Union are quite marked; the overall tax ratio ranges over more than twenty points of GDP, from 28.0 % in Romania to 48.2 % in Denmark. In other words, the tax burden in the highest-taxing EU Member State is over 70 % higher than in the least taxing one. These large differences of course depend mainly on social policy choices like public or private provision of services such as old age pensions, health insurance and education, on the extent of public employment, or of State activities, etc.. Technical factors also play a role: some Member States provide social or economic assistance via tax reductions rather than direct government spending…. It should also be highlighted that the GDP value, that constitutes the denominator of the overall tax ratio, includes estimates of production by the informal sector (the 'grey' and 'black' economy); so that not only low taxes, but also high tax evasion can result in a low overall tax ratio. 15 Con una lieve tendenza alla convergenza As a general rule, tax-to-GDP ratios tend to be significantly higher in the old EU-15 Member States (i.e. the 15 Member States that joined the Union before 2004) than in the 12 new Members; the first seven positions in terms of overall tax ratio are indeed occupied by old Member States. ….. … Despite these large differences, over the last years, until 2007 the overall tax ratio tended to converge. The ratio between the standard deviation and the mean of the overall tax ratios declined from 2001 to 2007; also the gap between the highest and the lowest overall tax ratio showed a similar trend. In 2008, however, tax ratios diverged again slightly, possibly owing to the rather different extent of the slowdown within Member States…. 16 La struttura del prelievo: differenza fra “nuovi” e “vecchi” stati membri Generally, the new Member States have a different structure compared with the old Member States; in particular, while most old Member States raise roughly equal shares of revenues from direct taxes, indirect taxes, and social security contributions, the new Member States, with the notable exception of Malta, typically display a lower share of direct taxes in the total. The lowest shares of direct taxes are recorded in Bulgaria (only 21.0 % of the total, still markedly up from 16.9 % in 2005, Slovakia (only 22.1 % of the total), and the Czech Republic (23.8 %). One of the reasons for the low direct tax revenues can be found in the generally more moderate tax rates applied in the new Member States on the corporate income tax and on the personal income tax. Several of these countries have adopted flat rate systems, which typically induce a stronger reduction in direct than indirect tax rates. 17 La struttura del prelievo: vi sono differenza anche fra i “vecchi” stati membri Also among the old Member States (the EU-15) there are some noticeable differences. The Nordic countries as well as the United Kingdom and Ireland have relatively high shares of direct taxes in total tax revenues. In Denmark and, to a lesser extent, also in Ireland and the United Kingdom the shares of social security contributions to total tax revenues are low. There is a specific reason for the extremely low share of social security contributions in Denmark: most welfare spending is financed out of general taxation. This requires high direct tax levels and indeed the share of direct taxation to total tax revenues in Denmark is by far the highest in the Union. Among the old Member States, the German and French tax systems represent in this respect the opposite of Denmark's with high shares of social security contributions in the total tax revenues, and relatively low shares of direct tax revenues. 18 Altre tendenze: PIT From 1995 to 2009, almost all EU Member States cut their top rate. Currently, the top personal income tax (PIT) rate amounts to 37.5 %, on average, in the EU. This rate varies very substantially within the Union, ranging from a minimum of 10 % in Bulgaria to a maximum of 56.4 in Sweden, as Denmark, which levied the highest PIT maximum rate until last year, has cut it to 51.5 %. For the first time in several years, the top PIT rate has increased, on average, in 2010, despite the sizeable Danish cut, as several EU Member States enacted increases (the UK introduced a new 50 % rate, ten points higher than the previous maximum, but Greece and Latvia too hiked their top rates). Lower PIT top rates do not necessarily imply a trend towards lower PIT revenues, because in systems with several tax brackets, the percentage of taxpayers taxed under the highest rate is typically quite limited. In addition, changes in the tax threshold can have important effects on the tax liability, even at unchanged rates; 19 20 Altre tendenze: CIT (1) Similarly to the trend recorded for the PIT, since the second half of the 1990s, corporate income tax (CIT) rates in Europe have been cut forcefully, from a 35.3 % average in 1995 to 23.2 % now. Unlike the case of the PIT, this trend has not been interrupted by the financial crisis, on the contrary a few Member States introduced further cuts in 2010 (the Czech Republic, Greece, Lithuania, Hungary, Slovenia) and none increased them. (vedi grafico p.71) Although the downward trend has been quite general, corporate tax rates still vary substantially within the Union. The adjusted statutory tax rate on corporate income varies between a minimum of 10 % (in Bulgaria and Cyprus) to a maximum of 35.0 % in Malta, although the gap between the minimum and the maximum has shrunk since 1995. 21 22 Altre tendenze: CIT (2) Some countries have implemented changes that go beyond simple rate cuts. Estonia is a good example of this development. The country moved away from the classical corporation tax system: despite the low CIT rate (26 %) in force since 1994, since the beginning of 2000 Estonia decided to levy no corporate tax on retained profits, so that only distributed profits are taxed. The rate was later cut to 21 %. A similar system had been introduced also in Lithuania, but was later abolished. Another example is Belgium, where the introduction of the notional interest system has had the effect of reducing the tax burden fairly significantly, even though it does not translate into a change in the nominal tax rate. 23 Imposte societarie (CIT), personali (PIT) e sul consumo Analysing the role of corporate taxation in the overall tax systems of the OECD countries we find three main interdependencies. First, countries with larger governments tend to rely less on corporate taxation. Further, it can be observed that corporate taxation and personal income taxation tend to move together. On the other hand, governments seem to compensate for corporate tax reductions by increasing value-added taxes. In consequence, over the last two decades, a shift from income taxation towards consumption taxation, i.e. valueadded taxes, can be observed. So far this trend is most pronounced for smaller European countries. However, more recent tax reforms, most notably in Germany, indicate that these tendencies might continue unabated and also in larger economies. (Loretz, 2008) 24 Andamento del gettito e ciclo economico “… actually observed tax revenue developments are not only determined by policy and decision making processes. They are also substantially influenced by factors outside the decision makers' sphere of (direct) influence. Predominant among these other factors impacting on revenue developments are cyclical influences on economic activity. Usually, in a favourable economic climate (company) profits increase and new jobs are created, both of which increase revenues from direct taxes, namely corporate and personal income taxes. Generally, accelerating job creation also means more people being liable to social security contributions, hence increasing revenues of the latter. Conversely, economic downturns are characterised by a deterioration of company profits and only moderate wage developments if not the loss of numerous jobs. Hence, tax and social security revenues based on these macroeconomic variables decrease disproportionately. (Taxation trends,….) 25 Gettito corretto per il ciclo: cosa è? Summing up, economic fluctuations – being only temporary in nature – have an important impact on the assessment in tax revenue developments. Nominal or observed tax revenues are the result of two factors: temporary and permanent ones. Hence, filtering out, to the extent possible, the impact of cyclical - and hence temporary – factors from permanent developments reveals important information to policy makers and policy assessors. assessments of this kind are usually based on correcting nominal tax revenue developments for the economic cycle. The resulting cyclically adjusted tax revenue data show primarily the development of the structural components, which are largely the result of discretionary fiscal policy decisions. In a nutshell, cyclically adjusted revenues in % of GDP for each country (CAR) are derived as the (i) overall tax-to GDP ratio (including social security contributions) (R) minus (ii) the cyclical component of the tax revenues in % of GDP (including social security contributions) (C). CAR = R − C 26 Gettito corretto per il ciclo: come si misura The cyclical component of tax revenues (C) is hence that part of revenue which is due to cyclical developments. In order to determine (C) two measures are necessary: First, a measure of the cyclical position of the economy has to be derived, measuring the deviation of GDP from its "normal" level, i.e. the level that would have been achieved if GDP growth was on its "normal" path over time. In this report, the cyclical position is provided by the HP – filtered output gap, i.e. the difference between actual real GDP and a measure of the trend real GDP. …second measure - the tax revenue sensitivity. The tax revenue sensitivity is defined as the percent change in tax revenues (as a ratio to GDP) in reaction to a 1 % change in the output gap. The cyclical component of tax revenues (C) is hence calculated as the product of the HP-filtered output gap and the tax revenue sensitivity. By subtracting the cyclically determined part of tax revenues (C) from overall tax revenues we arrive at the cyclically adjusted or "structural“ tax revenues, highlighting the effects of discretionary policy action on tax revenues. 27 Gettito corretto per il ciclo: risultati ….the cyclical component of tax revenues was not very pronounced in the period under investigation. The cyclical component only exceeded one percent of GDP at the end of the period in 2007 and 2008, when actual GDP was considerably above its potential, translating into a high positive output gap. This generally low cyclical component just reflects the rather limited reaction of tax revenues to economic activity, as the tax revenue sensitivity is 0.42 for the Euro area [0,49 per Italia] and 0.39 for the EU-25 respectively. In general, the development of the cyclical component for the Euro area and the EU-25 are very similar. However, while the cyclical component was more pronounced for the Euro area at the beginning of the period, it showed higher values for the EU-25 from 2004 onwards. This is the result of faster recovery since 2004 and much higher GDP growth since then for the new Member States. …. Comparing cyclically adjusted tax revenues (dashed lines) with actual tax revenues unveils interesting tax trends that are masked by the economic cycle. The high tax burden observed in 1995-1999 was actually realised against the backdrop of unfavourable economic conditions, resulting in an even higher tax burden in cyclically adjusted terms…… 28 Aliquote effettive e altri indicatori T/PIL e Ti/T sono indicatori aggregati e poco utili (il loro andamento dipende da molteplici fattori) Anche aliquote legali da sole non bastano Indicatori più utili, che tengono conto dell’interazione fra aliquote e basi imponibili: Backward looking o forward looking Micro o macro Esempi: Implicit tax rates (EU trends) Cuneo di imposta sul lavoro (OECD: taxing wages) EMTR e EATR sul capitale (vedi II modulo) 29 Aliquote macroeconomiche implicite (EU trends…) The tax-to-GDP ratio and the breakdown of tax revenues into standard categories such as direct taxes, indirect taxes and social contributions provide a first insight into cross-country differences in terms of tax levels and its composition in terms of tax type. This information is, however, already available from the National Statistical Offices. This publication additionally provides a broad classification of taxation in three economic functions - consumption, labour and capital. The report contains data on the absolute level of taxation by economic function and computes implicit tax rates or ITRs, i.e. average effective tax burden indicators; unlike simple measures of the tax revenue, these take into account the size of the potential tax base, which often differs substantially from one country to the other. The methodology utilised in this survey is discussed in detail in Annex B. (si veda soprattutto parte D p.400) 30 Aliquote macroeconomiche implicite : metodologia The tax revenue relative to GDP statistics presented in this survey can be described as macro backward-looking tax burden indicators. In Part C the taxes raised on economic functions are shown as percentages of total GDP. However, the consideration of tax revenue as a proportion of GDP provides limited information as no insight is given as to whether, for example, a high share of capital taxes in GDP is a result of high tax rates or a large capital tax base. These issues are tackled through the presentation of ITRs which do not suffer from this shortcoming. ITRs measure the actual or effective average tax burden directly or indirectly levied on different types of economic income or activities that could potentially be taxed by Member States. 31 Aliquote macroeconomiche implicite : metodologia Note, however, that the final economic incidence of the burden of taxation can often be shifted from one taxpayer to another through the interplay of demand and supply: a typical example is when firms increase sales prices in response to a hike in corporate income taxation; to a certain extent the firms' customers end up bearing part of the increased tax burden. The ITRs cannot take these effects into account, as this can only be done within a general equilibrium framework. Despite this limitation, ITRs allow the monitoring of tax burden levels over time (enabling the identification of shifts between the taxation of different economic functions e.g. from capital to labour) and across countries. Alternative measures of effective tax rates exist, which, using tax legislation, simulate the tax burden generated by a given tax, and can be linked to individual behaviour. However, these 'forwardlooking' effective tax rates do not allow the comparison of the tax burden implied by different taxes; nor do they facilitate the identification of shifts in the taxation of different economic income and activities. 32 Aliquote macroeconomiche implicite: vantaggi For capital, an average tax rate is estimated by dividing all taxes on capital by a broad approximation of the total capital and business income both for households and corporations. For labour, an average tax rate is estimated by dividing direct and indirect taxes on labour paid by employers and employees by the total compensation of employees. The attractiveness of the approach lies in the fact that all elements of taxation are implicitly taken into account, such as the combined effects of statutory rates, tax deductions and tax credits. They also include the effects due to the composition of income, or companies' profit distribution policies. Further, the effects of tax planning, as well as the tax relief available (e.g. tax bases which are exempted below a certain threshold, non-deductible interest expenses), are also taken implicitly into account. 33 Aliquote macroeconomiche implicite: limiti The advantage of the ITRs in capturing a wide set of influences on taxation is accompanied by difficulties in interpreting the trends when a complete and precise separation of the different forces of influence is not possible. In addition, any timing differences that arise because of lags in tax payments and business-cycle effects may give rise to significant volatility in these measures. In short, they represent a reduced model of all variables influencing taxation, tax rates and bases. 34 Aliquote macroeconomiche implicite: andamento Data for the ITR on consumption, our preferred measure of the effective tax burden, show that effective taxation of consumption, which had been on an uptrend since 2001, dropped sharply in 2008. The EU-27 arithmetic average declined by 0.7 percentage points that year, the sharpest fall in a single year on record. Nevertheless, given the previous relatively strong growth since 2001, the indicator still exceeds its 2000 level by 0.6 points in 2008. This sharp and broad drop cannot be attributed to declines in VAT rates …, and seem therefore rather attributable to the first effects of the crisis on consumption behaviour. The extent and rapidity of this development is striking given that the ITR on consumption should arguably, by construction, show a lesser susceptibility to cyclical developments than other ITRs …. The sharpness of the drop is therefore probably the result of a combination of factors, such as a shift in consumption patterns towards primary goods, typically subject to lower VAT rates, or involuntary inventory build-ups by businesses, which due to the severity of the downturn at the end of 2008 might have led to significant VAT refunds by tax administrations. 35 Aliquote macroeconomiche implicite: andamento Despite a wide consensus on the desirability of lower taxes on labour, the levels of the ITR on labour confirm the widespread difficulty in achieving this aim. Although the tax burden on labour is off the peaks reached around the turn of the century, the downward trend essentially came to a halt in the euro area as several countries witnessed increases in the last few years. Unlike for the ITR on consumption, the crisis did not induce any visible reduction of the ITR on labour in 2008, possibly because of the tendency for labour markets to lag behind cyclical developments. The EU-25 average remained constant and the euro area even recorded an increase in the ITR on labour….. 36 Aliquote macroeconomiche implicite: andamento The ITR on capital shows a stronger decline for 2008, 0.7 points in the EU-25 average, but this level remains the second highest on record after the 2007 figure. Various factors suggest that, barring introduction of new taxes, the ITR on capital is unlikely to remain at these high levels in the next few years. First, the ITR on capital has historically been sensitive to the business cycle: the EU-25 ITR on capital reached a peak between 1999 and 2000, then declined, and picked up again, in line with the business cycle. Inevitably, given the in-built lag in CIT payments, the effects of the recession will increasingly affect the ITR already in the short term. In addition, the strong cuts in the CIT statutory rate should increasingly translate in lower revenues. …The absolute levels of the ITRs on capital differ widely within the EU, ranging from 45.9 % in the UK to a mere 10.7 % in Estonia. 37 Aliquote macroeconomiche implicite: andamento The development of environmental tax revenue is currently subject to opposite forces; on the one hand, policymakers give high priority to environmental protection, a trend which may grow even stronger as attention focuses on the threat from global warming; on the other, greater reliance on policy instruments other than taxes, such as emissions trading, and growing political pressure to accommodate the strong increases in the oil price recorded in the last few years by reducing taxation of energy. Currently, roughly one euro out of every fourteen in revenue is raised from environmental taxes. The implicit tax rate on energy shows that wide differences in the tax revenue raised per unit of energy consumed persist (the highest taxing country levies four times as much revenue per unit of energy than the least taxing Member State), and indicates that in the weighted average, once adjusted for inflation, taxation of energy has been gradually declining. 38 Cuneo di imposta sul lavoro Labour tax wedge: Forward looking micro indicator OECD, Taxing Wages http://www.oecd.org/document/34/0,3343,en_2649_345 33_44993442_1_1_1_37427,00.html Taxing Wages provides estimates of tax burdens and of the tax wedge between labour costs and net take-home pay Table O.1 presents the total tax wedge between total labour costs to the employer and the corresponding net take-home pay for single workers without children at average earnings levels in 2009 and analyses the change in the tax wedge between 2008 and 2009 for all OECD countries. The tax wedge varied widely across OECD countries (column 1): it exceeded 50 per cent in Belgium, Hungary and Germany and was lower than 20 per cent in Korea, New Zealand and Mexico. 39 40 Cuneo di imposta sul lavoro: un approfondimento per l’Italia (Giannini, Guerra, 2010) Non vi è dubbio che in Italia il cuneo di imposta sul lavoro, misurato come divario percentuale fra costo del lavoro per l’imprenditore e salario netto per il lavoratore, sia elevato, anche in relazione ai nostri principali partner. Nell’effettuare confronti internazionali, occorre però tenere sempre in considerazione le modalità di erogazione e finanziamento degli interventi nel campo del welfare e del sostegno ai bisogni familiari. Ad esempio, mentre nel calcolo del cuneo di imposta sul lavoro si tiene conto dei contributi che finanziano i sistemi pensionistici pubblici, altrettanto non accade per i contributi che finanziano i sistemi previdenziali privati di tipo complementare. Ancora, se in un paese il sostegno alle famiglie avviene attraverso l’offerta di servizi, ad accesso gratuito, questo non si rifletterà in modo positivo sul cuneo come accade per un trasferimento monetario, di cui si tiene invece solitamente conto nel calcolo del cuneo stesso. 41 Oltre ad essere sensibile alle varie componenti del prelievo, fiscale e contributivo, che vengono incluse nel calcolo e che possono variare da paese a paese, la misura del cuneo dipende anche dalla figura e dal reddito preso a riferimento, essendo esso in buona parte composto da imposte e trasferimenti personali e progressivi. Pur con queste precisazioni, non vi è dubbio che in Italia le retribuzioni nette siano relativamente basse e, a causa del cuneo fiscale e contributivo, il costo del lavoro relativamente alto. Secondo l’ultimo rapporto dell’Oecd [2009] Taxing wages 2007-2008 – che ricostruisce i cunei di imposta sul salario come rapporto fra imposte e contribuiti, al netto dei trasferimenti monetari alle famiglie, in percentuale del costo del lavoro – per un lavoratore con retribuzione media, con coniuge e due figli a carico, il cuneo di imposta nel 2008 è il 36% in Italia, rispetto ad una media Oecd del 27,3% e dei paesi Ue del 32%. Vi è comunque moltissima variabilità, che riflette anche i fattori istituzionali precedentemente ricordati e nella Ue (fra i 19 paesi considerati dall’Oecd) l’Italia ha una posizione mediana, essendo superata da ben 9 paesi su 19. 42 Tuttavia, a riprova delle difficoltà di confrontare questi indicatori, va sottolineato che l’Oecd non tiene conto, nei calcoli del cuneo, della presenza dell’Irap, che pure ha, tra le componenti della sua base imponibile, la remunerazione del fattore lavoro e su cui peraltro si è concentrata la maggiore attenzione, nel dibattito di policy. Se si tiene compiutamente conto dell’Irap, incluso il fatto che essa è indeducibile dall’Ires, il cuneo aumenta di un paio di punti percentuali. 43 44 45 ….. se la normativa non fosse cambiata, il cuneo sarebbe cresciuto automaticamente, proprio per effetto dell’operare congiunto di fiscal drag e fiscal dividend. L’effetto è maggiore per un contribuente con coniuge e figli a carico, data la presenza, in questo caso, di detrazioni o deduzioni e trasferimenti per oneri familiari, decrescenti al crescere del reddito nominale. Confrontando il cuneo di imposta a legislazione 2000 con quello osservato in base alla normativa vigente ogni anno, è evidente come le numerose normative che si sono susseguite nel periodo, abbiano avuto solo l’effetto di compensare, un po’ meno per un single, un po’ più per un contribuente con familiari a carico, gli effetti automatici legati al fiscal drag e al fiscal dividend… “ 46 Testi di riferimento OECD, Revenue Statistics 1965-2008, 2009 Edition http://www.oecd.org/document/4/0,3343,en_2649_34533_414074 28_1_1_1_1,00.html Eurostat and European Commission, Taxation trends in the European Union, 2010 edition http://ec.europa.eu/taxation_customs/resources/documents/tax ation/gen_info/economic_analysis/tax_structures/2010/2010_ful l_text_en.pdf Altre letture: S. Loretz, Corporate taxation in the OECD in a wider context, Oxford Review of Economic Policy, Volume 24, Number 4, 2008, pp.639–660. Becker, J., Elsayyad, M. 2009. The evolution and convergence of OECD tax systems, Intereconomics: review of European economic policy, 44 2, pp105-113 OECD, Taxing wages, 2009 http://www.oecd.org/document/34/0,3343,en_2649_34533_44993442_1_1_1_ 37427,00.html S.Giannini e M.C.Guerra, Un decennio di fisco: poche riforme e molte occasioni mancate, in M.C.Guerra, A. Zanardi, Rapporto finanza pubblica, 2010, Il Mulino, 2010. 47