Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

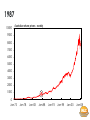

Economic and market prospects Brian Parker CFA Investment Strategist MLC Investment Management August 15 2008 General advice warning and disclaimer Any opinions expressed in this presentation constitute our judgement at the time of issue and are subject to change. We believe that the information contained in this presentation is correct and that any estimates, opinions, conclusions or recommendations are reasonably held or made as at the time of compilation. However, no warranty is made as to their accuracy or reliability (which may change without notice) or other information contained in this presentation. To the maximum extent permitted by law, we disclaim all liability and responsibility for any direct or indirect loss or damage which may be suffered by any recipient through relying on anything contained in or omitted from this presentation. This presentation contains general information and may constitute general advice. It does not take into account any person’s particular investment objectives, financial situation or individual needs. It should not be relied upon as a substitute for financial or other specialist advice. It has been prepared solely as an information service for financial advisers and should not be distributed to clients. Before making any decisions on the basis of this presentation, you should consider the appropriateness of its content having regard to your particular investment objectives, financial situation or individual needs. Opinions expressed constitute our judgement at the time of issue and are subject to change. The presenter is a representative of MLC Investments Limited. MLC Investments Limited ABN 30 002 641 661 105-153 Miller Street, North Sydney NSW 2060 is a member of the National group of companies. MLC Investments Limited is the issuer of the MLC MasterKey Unit Trust. Information about the MLC MasterKey Unit Trust is contained in the current Product Disclosure Statement (‘PDS’), copies of which are available upon request by phoning MLC on 131 831 or on our website at mlc.com.au. 27 years of balanced fund returns 35 MLC Horizon 4 return (%) for financial year ended 30 June 30 25 20 15 10 5 0 -5 -10 1982 1985 1988 1991 1994 1997 2000 Source: Mercer. Performance is after fees and superannuation tax 2003 2006 A tough time for share and LPT investors 1300 Value of A$1000 invested at end June 2007 1200 1100 1000 Global bonds $1100, 8.5% p.a Cash $1084, 7.2% p.a Aust. Bonds $1081, 6.9% p.a 900 Emerging mkts $925, -6.5% p.a 800 700 600 Global shares $843, -13.6% p.a Aust. Shares $819, -15.8% p.a LPTs $629, -32.8% p.a 500 400 Jun-07 Sep-07 Dec-07 Mar-08 Jun-08 Source: Thompson Financial Datastream. Last observation is 13 August 2008 Global economy in snapshot ..and unemployment rates are starting to drift higher.. Economic growth in the G4 economies has slowed... Real GDP y/y% 6 10 Unemployment rate % Source: Thomson Financial Datastream 4 8 2 Source: Thomson Financial Datastream 6 z 0 4 -2 US -4 Euro-area Japan UK 2 US 0 Q1 1997 Q1 1999 Q1 2001 Q1 2003 Q1 2005 Q1 2007 Jul-00 EPS Q1 2002 equals 100 300 US Euro-area 6 Japan UK 2 200 0 150 -2 50 Q1 1998 Q1 2002 Q1 2004 -6 Q1 2006 Jul-06 Jul-08 6 mthly % change -4 Source: Thomson Financial Datastream Q1 2000 Jul-04 UK Source: Thomson Financial Datastream 4 250 100 Jul-02 Japan ..and the leading indicators are consistent with further weakness ..earnings have started to decline.. 350 Euro-area Q1 2008 Jul-98 G7 industrial output Jul-00 Jul-02 G7 leading indicator Jul-04 Jul-06 Jul-08 A global crisis of confidence? Business and consumer confidence in the major economies# 2.5 Deviation from recent history 2.0 # Weighted average of US, Euro-area, Japan 1.5 1.0 0.5 0.0 -0.5 -1.0 -1.5 -2.0 -2.5 Q1 1992 Manufacturing conditions Consumer sentiment Q1 1995 Q1 1998 Q1 2001 Q1 2004 Q1 2007 The US economy is probably in recession already Consumer confidence is already at recession levels 135 125 US Univ. of Michigan consumer sentiment indices GDP growth is OK, but the leading indicators look lousy 10 Expected conditions Current conditions 8 Annual change % Conference Board leading index Real GDP 115 6 105 95 4 85 2 75 65 0 55 -2 45 35 Jan-81 Jan-86 Jan-91 Jan-96 Jan-01 Jan-06 Source: Thomson Financial Datastream -4 Q1 1988 Q1 1992 Q1 1996 Q1 2000 Q1 2004 Q1 2008 US housing: the state of play ..helping to create a huge overhang of unsold homes Home sales have plummeted.. 8500 '000 annualised 12 7500 Unsold single-family homes to total sales ratio 10 6500 8 5500 6 4500 Total home sales (new + existing) 3500 2500 Jan-93 4 2 Jan-96 Jan-99 Jan-02 Jan-05 Jan-08 Jan-85 Jan-88 Jan-91 Jan-94 Jan-97 Jan-00 Jan-03 Jan-06 Housing starts have fallen in response to sharply weaker demand.. ..but more forced sales are likely as delinquency rates have soared. 2500 4.0 Delinquency rate % of loans outstanding 3.5 2000 3.0 1500 2.5 2.0 1000 Housing starts (lhs) 1.5 1.0 500 Jan-93 Jan-96 Jan-99 Jan-02 Jan-05 Source: Thomson Financial Datastream Jan-08 Q2 1990 Q2 1993 Q2 1996 Q2 1999 Q2 2002 Q2 2005 House prices in the English speaking (!?) economies. US houses have come down a long way… 300 Real (inflation adjusted) house prices. March quarter 1988 equals 100 US 250 UK Aust 200 150 100 Sources: Datastream, RBA, MLC Investment Management 50 Q1 1988 Q1 1991 Q1 1994 Q1 1997 Q1 2000 Q1 2003 Q1 2006 ..which has improved affordability.. 150 Housing affordability index 140 130 120 110 100 90 Jan-88 Jan-91 Jan-94 Jan-97 Source: Thompson Financial Datastream Jan-00 Jan-03 Jan-06 ..but that’s a fat lot of good if the banks aren’t lending! US Consumer lending standards are tightening.. 100 Net % of lenders tightening standards 80 ..as are standards for both large and small businesses.. 70 Credit cards Other consumer lending Prime mortgages Sub-prime mortgages 60 Net % of lenders tightening standards Large & medium firms Small firms 50 40 60 30 20 40 10 20 0 -10 0 -20 -30 -20 Q3 1998 Q3 2000 Q3 2002 Q3 2004 Sources: US Federal Reserve, Datastream Q3 2006 Q3 2008 Q3 1998 Q3 2000 Q3 2002 Q3 2004 Q3 2006 Q3 2008 How much more debt can be rammed down the throats of consumers in the English speaking world anyway?.. Australian household debt % 180 160 as % of GDP 140 as % of disposable income 120 100 80 60 40 20 0 Q1 1980 Q1 1985 Q1 1990 Q1 1995 Q1 2000 Q1 2005 UK household debt % 180 160 as % of GDP 140 as % of disposable income 120 100 80 60 40 20 0 Q1 1980 Q1 1985 Q1 1990 Q1 1995 Q1 2000 Q1 2005 Source: Thomson Financial Datastream US household debt 180 % 160 as % of GDP 140 as % of disposable income 120 100 80 60 40 20 0 Q1 1980 Q1 1985 Q1 1990 Q1 1995 Q1 2000 Q1 2005 Europe and Japan are in real danger of recession Japanese growth undermined by domestic spending Sentiment data are consistent with a Eurozone recession in late 2008 5.0 % Index 120 4.5 % Net exports contrib to y/y% growth Real GDP y/y% (lhs) 4.5 EU Economic sentiment index (rhs) 115 4.0 4.0 Domestic demand contrib to y/y% growth 3.5 Real GDP y/y% 110 3.0 3.5 105 3.0 2.5 100 2.0 95 2.5 2.0 1.5 1.0 1.5 90 0.5 1.0 0.5 Last figure is July 2008 85 0.0 80 Q1 1998 Q1 2000 Q1 2002 Q1 2004 Q1 2006 Q1 2008 0.0 -0.5 Q1 2003 Q1 2005 Q1 2007 China is not immune, but is well placed to weather the storm Export growth has slowed only slightly, while imports have accelerated China's growth eases back somewhat Annual change (%) 20 18 16 14 12 10 8 6 Industrial output 4 Real GDP 2 0 Q1 1996 Q1 1998 Q1 2000 Q1 2002 Q1 2004 Q1 2006 Q1 2008 China's non-food CPI has picked up, but from a very low base. Annual change (%) 10 9 8 Headline CPI 7 Non-food CPI 6 5 4 3 2 1 0 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 60 50 40 Annual change (%) Exports Imports 30 20 10 0 -10 -20 Q1 1996 Q1 1998 Q1 2000 Q1 2002 Q1 2004 Q1 2006 Q1 2008 • Chinese exports have slowed a little, and are likely to slow further, but the overall impact on growth is not likely to be severe. • Domestic spending is the key driver – consumer demand has accelerated, and investment spending not likely to slow dramatically, despite a series of policy tightening measures. • Inflation has soared on the back of food and energy costs, but core inflation is still very subdued. Global economic and investment prospects • US is either in recession now or heading into one, and the other major economies are slowing down. • Inflation concerns are largely misplaced, and the rate hike by ECB has only made growth prospects marginally worse.. • ..but the Chinese economy is well-placed to weather the storm (good news for Australia) • The US Federal Reserve and Treasury now understands the magnitude of the problem, and have responded (aggressive rate cuts, massive liquidity injections, public support to key institutions).. • ..and the economy and financial markets will recover (every crisis, every recession, every market downturn comes to an end!).. • ..but we are most unlikely to see a repeat of the kind of investment returns seen in recent years. Australia in summary • Reported growth still solid in March quarter, but more recently.. • • • • • Retail sales have been flat since end 2007 Credit growth has slowed dramatically Home loan approvals have plunged Consumer sentiment is just above 17 year lows Business surveys have shown significant weakness.. • And all this has happened BEFORE the bulk of the impact of past rate hikes could be expected to hit the economy • Bright spots? • Exports • Huge pipeline of investment spending • If domestic demand continues to weaken (likely) RBA’s inflation worries will evaporate. The next move in rates is DOWN, and very soon! RBA has done enough (borrowing costs already too high?) Nominal interest rates the highest since (at least) 1996.. 14 % Source: RBA 12 10 8 6 4 Cash rate Bank std. variable 2 Bank small/med. business rate 0 Jan-95 Jan-98 Jan-01 Jan-04 Jan-07 Interest rates and oil prices are biting Retail sales figure for June was a shocker - trend is now flat 2.0 Consumer sentiment just above levels not seen in seventeen years % 140 130 1.5 120 1.0 110 0.5 100 0.0 90 80 -0.5 70 -1.0 -1.5 Jul-05 m/m% sadj 60 m/m% trend Jul-06 Jul-07 Jul-08 50 Feb-79 Feb-84 Feb-89 Feb-94 Feb-99 Feb-04 Business surveys are the weakest in nearly seven years NAB business survey points to weaker growth 25 Net balance (%) 20 15 10 5 0 -5 -10 Actual business conditions Confidence -15 -20 Mar-97 Mar-99 Mar-01 Mar-03 Mar-05 Mar-07 Huge pipeline of resources projects The $A big picture AUD is still miles above purchasing power parity estimates 1.0 USD 2008 ave. average 0.9 latest 0.8 0.7 0.6 OECD's PPP estimate 0.5 Calendar year average 0.4 1983 1989 1995 2001 2007 Key drivers of the Australian Dollar Australian Dollar has tracked the terms of trade over time 170 165 Real trade-weighted AUD 160 exchange rate (lhs) 155 150 Terms of trade (rhs) 145 140 Source: JPMorgan, Thomson Financial Datastream 135 130 125 120 115 110 105 100 95 90 85 Q1 1983 Q1 1987 Q1 1991 Q1 1995 Q1 1999 Q1 2003 Q1 2007 There has been a reasonable link between the $A and interest rate differentials 120 800 bps 700 105 600 USD Aus/US mid-curve interest rate differential (lhs) 0.95 AUD/USD (rhs) Source: Thomson Financial Datastream 500 90 1.05 0.85 400 0.75 300 200 75 0.65 100 0.55 0 60 -100 Jan-89 0.45 Jan-92 Jan-95 Jan-98 Jan-01 Jan-04 Jan-07 Let’s keep the recent weakness in perspective 7000 ASX300 Index 6500 6000 5500 How will this look in 5 years’ time? 10 years’ time? 5000 4500 4000 3500 3000 Source: Thomson Financial Datastream 2500 Aug-03 Aug-04 Aug-05 Aug-06 Aug-07 Aug-08 1987 1050 Australian share prices - daily 1000 950 900 850 800 750 700 650 600 550 500 Jul-87 Aug-87 Sep-87 Oct-87 Nov-87 Dec-87 1987 1050 Australian share prices - daily 1000 950 900 850 800 750 700 650 600 550 500 Dec-86 Jun-87 Dec-87 Jun-88 Dec-88 Jun-89 Dec-89 Jun-90 Dec-90 1987 1800 Australian share prices - daily 1600 1400 1200 1000 800 600 400 200 Dec-84 Dec-86 Dec-88 Dec-90 Dec-92 1987 2500 Australian share prices - daily 2000 1500 1000 500 0 Dec-82 Dec-84 Dec-86 Dec-88 Dec-90 Dec-92 Dec-94 Dec-96 1987 4000 Australian share prices - weekly 3500 3000 2500 2000 1500 1000 500 0 Dec-79 Dec-82 Dec-85 Dec-88 Dec-91 Dec-94 Dec-97 1987 9000 Australian share prices - weekly 8000 7000 6000 5000 4000 3000 2000 1000 0 Dec-75 Dec-80 Dec-85 Dec-90 Dec-95 Dec-00 Dec-05 1987 10000 Australian share prices - weekly 9000 8000 7000 6000 5000 4000 3000 2000 1000 0 Jan-73 Jan-78 Jan-83 Jan-88 Jan-93 Jan-98 Jan-03 Jan-08 ..“Maybe I should head into cash until things settle down?!?” • Need to get 2 calls right – when to get out, AND when to get back in • Macro indicators are often useless when it comes to timing these things • Dalbar (2007) Investor performance 20 years to end 2006: Market return (S&P500) 11.8% Investors return 4.3% The difference? Trying to time markets! “.. there are known unknowns; that is to say we know there are some things we do not know. But there are also unknown unknowns -- the ones we don't know we don't know." …” • What we don’t know…(and may not know, that we don’t know) ? How far US house prices will fall ? How much damage will be done to household balance sheets ? The full impact on US financial institutions’ balance sheets (and hence their ability to create credit) ? The full impact on household spending and hence the economy ? The full impact on corporate earnings The cash trap: “I can get 7-8% at the bank. Why shouldn’t I take it?” • Market timing is difficult for the best managers, and impossible for the average person • 7.25% is a cyclical peak – cash and TD rates are likely to FALL from here • For non-super money, you lose up to half in tax and half through inflation • For superannuation money, Cash NEVER builds long-term wealth • Would you rather lend to the bank or own it? Quoted Div. Yield NAB 7.3% ANZ 7.8% CBA 5.9% SGB 5.6% WBC 5.6% Banks Index* 6.5% Grossed-up# 10.4% 11.1% 8.4% 8.0% 8.0% 9.2% Source: MLC Investment Management, ASX. Data as at 12 August 2008. *Datastream index of Australian Bank stocks. #Quoted dividend yield multiplied by 1.429 There’s always things to worry about • • • • • • • • • • The 1929 crash Great depression WW II Korean War Cuban missile crisis Vietnam War OPEC oil crisis I OPEC oil crisis II Latin American debt crisis Australia’s ‘banana republic” moment • 1987 stockmarket crash • • • • • • • • • • • • The fall of the Berlin Wall Iraq War I US savings and loan crisis The recession we had to have Bond market crash 1994 Mexican debt crisis 1995 Asian crisis 1997 Russian debt/LTCM crisis Tech wreck September 11 Afghanistan Iraq War II Some questions… • Do you know your own tolerance for risk (the ‘sleep-at-night’ test)? • Do you know your financial goals and needs (both near term and longer term)? • Do you understand what kind of investment returns are achievable and sustainable over time? • Is all of this embodied in a financial plan produced by an appropriately qualified financial adviser? If the answer is ‘yes’ to all of the above, then nothing that’s happened in markets recently should cause you to do much at all!