Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

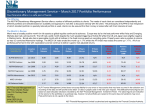

FUND FACTSHEET – MARCH 2015 All data expressed as at 28 February 2015 unless otherwise stated RHB-OSK CHINA-INDIA DYNAMIC GROWTH FUND This Fund aims to achieve medium to long term capital appreciation through investing mainly in the securities of corporations in, or corporations listed or to be listed on stock exchanges in, or corporations (wherever located) which, in the opinion of the managers, derive significant revenue or profits from or have significant assets or business interests in, the People’s Republic of China (“China”) or the Republic of India (“India”). INVESTOR PROFILE INVESTMENT STRATEGY This Fund is suitable for Investors who: • wish to tap the growth prospects of two emerging growth engines of the world i.e. China and India; • are willing to accept a higher risk in their investments to obtain potentially higher returns in the medium to long term; and • seek capital appreciation. • At least 95% of NAV: Investments in the units of United China-India Dynamic Growth Fund. • 2% - 5% of NAV: Investments in liquid assets including money market instruments and deposits with financial institutions. FUND PERFORMANCE ANALYSIS FUND DETAILS Performance Chart Since Launch* Cumulative Performance (%)* 1 Month Fund 1.22 Benchmark 2.18 Fund Benchmark 1 Year 41.17 38.32 Calendar Year Performance (%)* 2014 Fund 28.49 Benchmark 20.88 Investment Manager 3 Months 12.67 12.29 6 Months 24.93 22.06 3 Years 59.95 44.98 Since Launch 34.42 25.97 2013 10.79 5.73 2012 16.81 17.62 RHB Asset Management Sdn. Bhd. Trustee TMF Trustees Malaysia Bhd Fund Category Feeder Fund Fund Type Growth Fund Launch Date 11 March 2010 Unit NAV RM0.6720 Fund Size (million) RM16.28 Units In Circulation (million) 24.23 Financial Year End 31 July MER (as at 31 July 2014) 0.47% Min. Initial Investment RM1,000.00 Min. Additional Investment RM100.00 Benchmark 50% MSCI China Index (RM) + 50% MSCI India Index (RM) Sales Charge Up to 5.50% of investment amount Redemption Charge None Annual Management Fee 1.80% p.a. of NAV* Annual Trustee Fee 0.08% p.a. of NAV, subject to a min. of RM18,000 p.a.* Switching Fee RM25.00 per switch Redemption Period Within 10 days after receipt the request to repurchase Distribution Policy Incidental *For the purpose of computing the annual management fee and annual trustee fee, the NAV of the Fund is exclusive of the management fee and trustee fee for the relevant day. YTD 9.59 11.55 2011 -28.79 -26.54 Source: Lipper IM FUND PORTFOLIO ANALYSIS Sector Allocation* Financials Information Technology Industrials Consumer Discretionary Healthcare Telecommunication Energy Consumer Staples Materials Utilities Cash FUND STATISTICS Country Allocation* 29.74% 18.06% 9.52% 9.37% 8.51% 5.88% 5.56% 4.98% 4.78% 1.08% 2.52% 0% 5% 10% 15% 20% 25% 30% 35% India 52.21% China 42.43% Hong Kong 2.84% Cash 2.52% 0% 10% 12 Months 0.6760 0.4636 Since Launch 0.6760 0.3648 Source: Lipper IM 20% 30% 40% 50% Top Holdings (%)* TENCENT HOLDINGS LIMITED 5.12 INFOSYS LIMITED 4.32 CHINA MOBILE LIMITED 4.26 CHINA CONSTRUCTION BANK - H 3.86 INDUSTRIAL & COMMERCIAL BK OF CHINA - H 3.81 *As percentage of NAV *Source: UOBAM, 28 February 2015. Exposure in United China India Dynamic Growth Fund - 96.93% RHB Asset Management Sdn Bhd (174588-x) Historical NAV (RM) 1 Month High 0.6760 Low 0.6472 60% Historical Distributions (Last 4 Years) (Net) Distribution Yield (%) (sen) 31 Jul 2014 31 Jul 2013 31 Jul 2012 31 Jul 2011 - Source: RHB Asset Management Sdn. Bhd. Head Office: 19th Floor, Plaza OSK, Jalan Ampang, 50450 Kuala Lumpur General Line: 603-2164 3036 FUND FACTSHEET – MARCH 2015 All data expressed as at 28 February 2015 unless otherwise stated RHB-OSK CHINA-INDIA DYNAMIC GROWTH FUND This Fund aims to achieve medium to long term capital appreciation through investing mainly in the securities of corporations in, or corporations listed or to be listed on stock exchanges in, or corporations (wherever located) which, in the opinion of the managers, derive significant revenue or profits from or have significant assets or business interests in, the People’s Republic of China (“China”) or the Republic of India (“India”). MANAGER'S COMMENTS Fund performance In the month of February 2015, the United China-India Dynamic Growth fund gained 3.87% (JPY terms) under-performing the benchmark 50% MSCI China, 50% MSCI India which gained 4.78% (JPY terms), by 0.91%. Asset Allocation Our official asset allocation is now neutral China-India, i.e. 50 China: 50 India in the first quarter of 2015. We had moved from slightly overweight India vs China in the previous quarter, i.e. 55 India: 45 China. In China, we see policy easing being supportive the markets now despite weaker than expected economic data. Valuations remain very attractive, versus the region and its history too. The government’s focus on reforms and restructuring SOEs could improve sentiment and improve corporate profitability. In India, the market has enjoyed a strong re-rating on the BJP’s decisive election victory and continues to benefit from strong macro tailwinds. Lower energy and commodity prices ease inflation and improve the current account and fiscal deficits. It has also given a boost to corporate earnings. Valuations have reflected these positive tailwinds to some extent as MSCI India is trading close to 1 standard deviation above its historical mean. Much of the market re-rating has been done, and earnings growth will be the driver of the markets going forward. China Market Commentary MSCI China gained 5.27% (JPY terms) in the month of February 2015. The China market gained in February, outperforming the broad Asia ex-Japan markets, which lagged other regions across global equities. Developed markets outperformed emerging market equities. Australia was the best-performing market globally as the central bank cut policy rate for the first time in 1½ years. The US Federal Reserve chairman’s comments, which were generally viewed as dovish on rate hikes and China’s further monetary easing measures buoyed markets. Within China, consumer discretionary was the best performer, driven by auto stocks. Information technology, energy, telecommunication and financials outperformed while utilities, healthcare and consumer staples were the worst performers. On the economic front, global leading indicators were mixed in February. In developed markets, the US and Japan purchasing managers’ indices (PMIs) softened while the UK improved and Eurozone was stable. In emerging markets, Russia and China PMIs improved while India and Brazil PMIs softened. China’s official PMI rose slightly to 49.9 in February from 49.8 in January, though continuing to show contraction in manufacturing activity. However, the private sector HSBC PMI rose from 49.7 in January to 50.7 in February – its first sign of expansion after more than a year in contraction. Other latest activity indicators such as industrial production and retail sales generally improved across global markets except in Japan, Russia and India. Inflation remained subdued. Across central banks in Asia Pacific, Australia and Indonesia both cut policy rates by 25 basis points (bps) each in February. The China market outperformed as the central bank further eased monetary conditions. It cut reserve requirement ratio by 50 bps earlier in the month and further reduced interest rates by 25 bps at the end of February after a first round of rate cuts in November last year. The one-year benchmark deposit rate is now 2.5% from 2.75% and one-year benchmark lending rate is 5.35% from 5.6%. The PBoC also announced an increase in deposit rate ceiling premium from 20% to 30%, in a move to further liberalise interest rates. The rate cut is expected to lower funding cost to the real economy and address disinflation pressure. China Market Outlook and Strategy Chinese policy makers face a difficult challenge of reforming the economy and achieving growth targets. Evidence so far suggests that efforts to reform the economy and weed out corruption will likely continue into 2015 and beyond. The push to reform combined with demographic realities, implies that growth expectations for China will likely be reduced in the periods ahead. This shift will have a significant bearing on our investment strategy in the years ahead. Achieving stable growth while restraining credit growth will be particularly difficult. China’s debt to GDP exploded to over 240% of GDP as of September 2014 from less than 150% in 2008. Even amidst this robust credit growth, GDP growth slowed from over 10% to 7% currently. While the central government balance sheet is still healthy, local government and SOE corporate balance sheets are stretched. Financial risks are rising given the slowdown in the property market and the acceleration of non-performing loans (NPLs). Sectors that had flourished against a backdrop of excessive fixed asset investment, real estate investment and credit growth are likely to face challenges as economic drivers shift. The Chinese economy faces an urgent need to reduce overcapacity, restructure SOEs, and clean up the environment. While policy easing could temporarily help support the financial and real estate markets, it is clear that the drivers of future opportunities in China have already shifted. The policy driven sectors of the earlier development phase in China will not be where the opportunities lie in the future. As China has transitioned from a low income to middle income economy, the rising disposable income of the household sector is where future opportunities will arise. The birth of the internet has created significant opportunities in retail and media sectors. Meanwhile, household patterns in the consumption of services is evolving, new business segments are emerging and opportunities for investment have already shifted to cater for evolving consumer demands. This transition in the underlying growth backdrop and shift in the structure and character of the economy will create winners and losers. Picking the right stocks in this challenging macro-environment will be critical. We are positive on China. We believe that the macro challenges have been reflected in share prices, with stock valuations at well below their 10-year mean on price-to-earnings metrics (close to 2008 global financial crisis levels on price-to-book metrics). China is the cheapest market in Asia. Nonetheless, we remain vigilant in tracking operating conditions with the slowdown in growth having an uneven impact across industries. Within China, we like technology, particularly the internet – social media and ecommerce, which are facilitating a sea change in consumer spending patterns. We are also overweight in selected industrials stocks, which are gaining in competitiveness against international peers, are leveraged to structurally positive trends such as increased travel, and benefit from lower energy prices. We have turned tactically positive on the financial sector given the tailwinds of monetary easing. However, we are cognizant that the banks still face challenges – contracting profit and net interest margins, non-bank disintermediation and rising NPLs. Within financials, we prefer insurance and securities companies. We remain underweight energy and materials given the weaker growth backdrop and overcapacity challenges. As is frequently the case with emerging markets, economic and market performance diverge. China is no exception. However, unlike environments in the past, where a rising tide lifts all boats, more recent conditions favour choosing the right boat. In the long term, China should continue to deliver above average economic growth. Supported by high savings rates and income growth, this should be an attractive backdrop for consumption growth and investment. We believe that the continued emergence of China as an economic superpower will create interesting opportunities in the years ahead DISCLAIMER: Based on the fund’s portfolio returns as at 15 February 2015, the Volatility Factor (VF) for this fund is 12.3 and is classified as “Very High”. (source: Lipper) “Very High” includes funds with VF that are above 10.2 (source: Lipper). The VF means there is a possibility for the fund in generating an upside return or downside return around this VF. The Volatility Class (VC) is assigned by Lipper based on quintile ranks of VF for qualified funds. VF is subject to monthly revision and VC will be revised every six months. The fund’s portfolio may have changed since this date and there is no guarantee that the fund will continue to have the same VF or VC in the future. Presently, only funds launched in the market for at least 36 months will display the VF and its VC. The VC referred to was dated 31 December 2014 which is calculated once every six months and is valid until its next calculation date, i.e. 30 June 2015. A Product Highlights Sheet (“PHS”) highlighting the key features and risks of the Fund is available and investors have the right to request for a PHS. Investors are advised to obtain, read and understand the PHS and the contents of the Master Prospectus dated 15 March 2014 and its supplementary(ies) (if any) (“the Master Prospectus”) before investing. The Master Prospectus has been registered with the Securities Commission Malaysia who takes no responsibility for its contents. Amongst others, investors should consider the fees and charges involved. Investors should also note that the price of units and distributions payable, if any, may go down as well as up. Where a distribution is declared, investors are advised that following the issue of additional units/distribution, the NAV per unit will be reduced from cum-distribution NAV to exdistribution NAV. Any issue of units to which the Master Prospectus relates will only be made on receipt of a form of application referred to in the Master Prospectus. For more details, please call 1-800-88-3175 for a copy of the PHS and the Master Prospectus or collect one from any of our branches or authorised distributors. The Manager wishes to highlight the specific risks of the Fund are management risk and foreign investment risks such as currency risk and country risk and the specific risks of the target fund are equity risk, country concentration risk, small and medium capitalisation companies risk, repatriation risk, regulatory risk, taxation risk and political risk. These risks and other general risks are elaborated in the Master Prospectus. This factsheet is prepared for information purposes only. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive it. Past performance is not necessarily a guide to future performance. Returns may vary from year to year. RHB Asset Management Sdn Bhd (174588-x) Head Office: 19th Floor, Plaza OSK, Jalan Ampang, 50450 Kuala Lumpur General Line: 603-2164 3036