Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

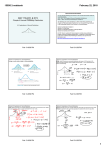

Eyeopener – NBP projection and data abroad 26 February 2010 Market moods remain volatile. Yesterday slight weakening of the zloty with deteriorated sentiment in the global markets due to weak labour market data from the US, warnings about possible downgrade of Greece’s rating and fall in stock markets. Overnight higher optimism and gains of the zloty after strong data from Asia. Local bonds gained being resistant to zloty performance and events abroad Today a bunch of major data abroad, the NBP released new Inflation report with details of new projections Yesterday during the domestic session the zloty slightly recovered with deteriorated moods in the global markets due to negative influence of weak data from the US labour market, warnings from rating agencies about a possible downgrade of Greece and weak macro figures from the euro zone. Much better expected data on durable goods from the US failed to improve market sentiment. The euro zone’s economic sentiment indicator unexpectedly fell to 95.9 in February from 96.0 in January (against expected rise to 96.4) and this was the first drop after 10 months of growth. The number of initial jobless claims in the US rose 22k and reached 496k against expected drop to 460k. The date increased concerns about prospects for improvement in labour market. Durable goods in the US increase 3%MoM in January after rise of 1.9%MoM a month earlier while growth of 1.5% was expected. On Wednesday, the S&P agency said that it might downgrade rating of Greece until the end of March and yesterday head of the agency’s European ratings said that the downgrade of rating for Greece would be a political challenge and could force the government to take necessary steps towards resolution of fiscal problems. At the same time he said there is no risk of insolvency of any country in the euro zone. Also yesterday Moody’s said rating of Greece may be downgraded, if it fails to execute its plan of fiscal deficit reduction from the highest level in the EU (12.7% of GDP in 2009). The EURPLN rate went slightly up during the day to ca. 4.00 from 3.988 at the opening. The zloty slightly weakened against the euro despite slight recovery of the single currency against the dollar to 1.353 at the end of the session from 1.347 at the opening. This in turn occurred despite declines in the stock markets and warnings from rating agencies regarding Greece. Both the dollar and the euro weakened against the Japanese yen. During the Asian session the EURUSD rate increase was continued to ca. 1.36 amid improving risk appetite after better than expected data on industrial output in Japan (increase by 2.5% in January) and moods in manufacturing in Korea. Sentiment improvement abroad resulted in the zloty strengthening, which opened stronger today near 3.98 vs. the euro. Relatively negative performance of the zloty and quite pessimistic moods in the world markets did not affect the local debt market, which strengthened during the day by a few basis points. At the same time there was an increase in RIS rates by a few basis points. In the core debt markets there were no significant changes despite weakening of the stock markets and amid mixed tone of the US data. At the end of the day yields of 10Y Treasuries and Bunds were at 3.11% and 3.647%, respectively, against 3.10% and 3.66% at the opening. In the interim forecasts for the 7 biggest economies of the European Union, the European Commission upwardly revised GDP growth forecast for Poland for 2010 to 2.6% from 1.8% predicted in autumn forecasts. At the same time it maintained its forecast for the EU and the euro zone at 0.7% (1.2% in Germany). According to comments from EU Economic and Monetary Affairs Commissioner Olli Rehn, the European Commission is going to present the assessment of the updated Polish Convergence programme in March. Minister of finance Jacek Rostowski said yesterday that assumptions to the bills, which would allow to introduce measures included in the fiscal consolidation plan, will be known in March-April. Today in the morning the National Bank of Poland published the Inflation Report, which included the new inflation projection of CPI and GDP. As regards growth projections, the report notes the expected change in the breakdown of growth in Poland in the next couple of years – acceleration in domestic demand (moderate in case of consumption and more significant for fixed investments) and neutral or slightly negative effect of net exports. We assume the similar change in the GDP breakdown but of a larger scale and thus higher GDP growth. According to the NBP the balance of risks for GDP and CPI projections is neutral. On the one hand, NBP said that substantial risk is connected with a possibility of higher food and energy prices (the projection assumes these prices to accelerate in 2012 anyway). On the other hand, lower inflation path as compared to the central projection (and GDP) might be driven by zloty appreciation. In our opinion, the latter factor is more important and more probable. More details will be known after the press conference, which started at 9:00 local time. Today in the euro zone inflation data will be published. According to market expectations HICP index in January rose by 1%YoY against 0.9% in December. In the afternoon the revised US GDP data for the fourth quarter will be released and the market consensus points to the figures of 5.7%YoY and 0.6%QoQ. This would be in line with previous release. In the last quarter of 2009 growth in the US was driven by positive impact of change in inventories (slowdown in inventory destocking process), slowdown in imports and some rebound in nonhousing investments. Later during the day (15:45 CET) the Chicago PMI will be published with expected fall in January to 60 from 61.5. Also, ten minutes later the Michigan index of consumer confidence will be released and analysts expect it remained close to the preliminary reading of 73.7. Data on home sales, to be released at the end of European session, are forecasted by the market at 0.9%MoM. 0, ECONOMIC ANALYSIS TREASURY SERVICES ul. Marszałkowska 142. 00-061 email: [email protected] fax +48 022 586 83 40 Web site: http://www.bzwbk.pl Maciej Reluga (Chief Economist) Piotr Bielski Piotr Bujak Cezary Chrapek +48 (0) 22 586 83 63 +48 (0) 22 586 83 33 +48 (0) 22 586 83 41 +48 (0) 22 586 83 42 Gdańsk Kraków Poznań Warszawa Wrocław +48 (0) 58 326 2630-32 +48 (0) 12 424 9501-02 +48 (0) 61 856 5814/25 +48 (0) 22 586 8320 +48 (0) 71 370 2587 Eyeopener – daily update Kursy walutowe (dzisiejsze otwarcie) EURUSD USDPLN EURPLN CHFPLN JPYPLN* GBPPLN 1.3570 2.9332 3.9795 2.7198 3.2839 4.4749 Kurs złotego (fixing) CADPLN DKKPLN NOKPLN SEKPLN CZKPLN HUFPLN Przegląd rynku finansowego 2.7659 0.5348 0.4944 0.4089 0.1533 1.4719 - 3.00 4.15 2.95 4.10 2.90 4.05 2.85 4.00 2.80 3.95 25.02.2010 Rentowności obligacji skarbowych % 6.30 6.10 5.70 % Zmiana (pb) % Zmiana (pb) % Zmiana (pb) 5.50 4.41 4.97 5.29 5.48 5.58 5.72 5.72 -2 2 2 3 2 5 6 0.46 1.05 1.66 2.17 2.59 3.38 3.69 -3 -4 -5 -6 -7 -7 -7 1.11 1.44 1.88 2.15 2.44 3.07 3.34 -1 -3 -1 -1 0 1 2 5.30 5.10 4.90 Dzienna zmiana (pb) 4.15 1X2 3X6 6X9 9X12 3X9 6X12 3.63 4.22 4.42 4.65 4.35 4.59 0 1 -4 0 -4 -3 4.10 17 Feb 15 Feb 13 Feb 25 Feb % 25 Feb Termin Stawki FRA (Mid) 23 Feb -1 5 0 1 0 -1 0 0 0 23 Feb 2.87 3.01 3.31 3.41 3.62 4.14 4.24 4.36 4.44 21 Feb O/N T/N SW 2W 1M 3M 6M 9M 1Y 5L 21 Feb Dzienna zmiana (pb) 19 Feb % 11 Feb 9 Feb 2L Termin 19 Feb Stawki WIBOR 7 Feb 5 Feb 28 Jan 4.70 3 Feb EZ 1 Feb US 30 Jan PL 10L 3-miesięczne stawki rynku pienięŜnego % 4.50 4.45 4.40 4.35 4.30 4.25 WIBOR FRA 3x6 17 Feb 15 Feb 13 Feb 11 Feb 9 Feb 5 Feb 3 Feb 1 Feb 30 Jan 28 Jan 4.20 7 Feb 1L 2L 3L 4L 5L 8L 10L EUR (prawa oś) 5.90 Stawki IRS (Mid) Termin 25 Feb 4.972 5.778 6.046 23 Feb 10.02 2.12 20.01 21 Feb 0 -6 -4 19 Feb 4.88 5.42 6.02 USD (lewa oś) Obligacje 17 Feb 2L 5L 10L 15 Feb Śr. rentown. 13 Feb % Ostatnia aukcja 11 Feb Termin Zmiana (pb) 9 Feb 3.9933 2.9601 - 7 Feb fixing 3.9967 2.9599 1.3510 5 Feb zamkn. 3.9880 2.9605 1.3475 3 Feb otwarcie 1 Feb max 4.0067 2.9752 1.3527 30 Jan min 3.9846 2.9528 1.3465 EURPLN USDPLN EURUSD 28 Jan Główne notowania walutowe FRA 6x9 * for 100 JPY Source: Reuters This publication has been prepared by Bank Zachodni WBK S.A. (a member of AIB Group) for information purposes only. It is not an offer or solicitation for the purchase or sale of any financial instrument. Information presented in the publication is not an investment advice. All reasonable care has been taken to ensure that the information contained herein is not untrue or misleading. But no representation is made as to its accuracy or completeness. No reliance should be placed on it and no liability is accepted for any loss arising from reliance on it. Forecasts or data related to the past do not guarantee future prices of financial instruments or financial results. Bank Zachodni WBK S.A.. its affiliates and any of its or their officers may be interested in any transactions. securities or commodities referred to herein. Bank Zachodni WBK S.A. or its affiliates may perform services for or solicit business from any company referred to herein. This publication is not intended for the use of private investors. Clients should contact analysts at and execute transactions through a Bank Zachodni WBK S.A. entity or an AIB Group entity in their home jurisdiction unless governing law permits otherwise. Copyright and database rights protection exists in this publication. Additional information is available on request. Please contact Bank Zachodni WBK S.A. Treasury Division. Economic Analysis Unit. ul. Marszałkowska 142. 00-061 Warsaw. Poland. phone (+48 22) 586 83 63. email [email protected]. http://www.bzwbk.pl Bank Zachodni WBK is a member of Allied Irish Banks Group