Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

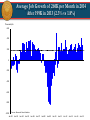

2015 Texas Economic Outlook: Tapping on the Brakes Keith Phillips Sr. Economist and Research Officer The views expressed in this presentation are strictly those of the presenter and do not necessarily reflect the positions of the Federal Reserve Bank of Dallas or the Federal Reserve System. Any secondary distribution of this material is strictly prohibited. National Economy Picking Up • Consumer spending picked up in 2014 as housing prices and stock market improved, and consumer debt fell • Declining energy prices in second half provided a further boost • Europe remains a question mark but if energy prices remain low, US economy should pick up further in 2015 Average Job Growth of 260K per Month in 2014 After 199K in 2013 (2.3% vs 1.8%) Thousands,SA 600 400 200 0 -200 -400 -600 -800 Source: Bureau of Labor Statistics -1000 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 U.S. Leading Index Suggests Continued Good Growth over Next 6 Months Annualized % change 20 15 12-month 6-month 10 5 0 -5 -10 -15 -20 1960 1965 1970 1975 1980 Source: Conference Board, Federal Reserve Bank of Dallas 1985 1990 1995 2000 2005 2010 2015 RGDP Grew 2.5% in 2014, January Blue Chip Survey Projects 2.8% in 2015 SAAR, Percent 8.0 2013 3.1% 2014 2.4% Q4/Q4 Q4/Q4 6.0 4.6 2012 2.0% Q4/Q4 3.9 3.9 4.0 1.3 4.5 2015 2.8% Q4/Q4 3.5 2.7 2.5 2.9 2.0 5.0 4.6 1.7 2.7 2.3 2.5 2.2 1.8 1.6 0.8 0.1 0.0 -0.5 -2.0 -1.5 -2.1 -4.0 -5.4 -6.0 -8.0 -8.2 -10.0 Source: Blue Chip Economic Indicators 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 TX Economy Has Grown Above Trend and Stronger than Most States • In past five years growth in energy, construction and exports provided a strong stimulus to Texas. • 2014 growth was broad based across sectors. Energy, construction, business services, health care, exports and tourism strong. Government sector improved. • In 2015, low oil prices and continued labor market tightness will likely restrain growth. Strong dollar may dampen exports. I expect job growth will slow in 2015 to between 1.0% and 2.0% (from 3.4% in 2014). Texas Economy Growing Well Above Trend (Texas Business Cycle Index) M/M SAAR 12 10 8 6 4 2 2.6% trend 0 -2 -4 -6 -8 NOTE: Shaded areas represent Texas recession. Texas Ranked Sixth in Job Growth in 2014 Percent Change, Dec. 2013 - Dec. 2014 5 4.5 4 3.5 TX 3 2.5 U.S. 2 1.5 1 0.5 0 ND FL GA UT NV TX CO OR WA CA NC SC AR AZ TN US DE ID KY MA LA WY MI WI OK NY AL NM MD CT IN IA KS OH NH MN RI PA IL DC VT AK VA SD MO NJ NE MS MT ME HI WV -0.5 Source: Bureau of Labor Statistics Texas Jobs Growing Faster Than Nation’s Percent, Job Growth Y/Y 5 U.S. Texas 4 3.5 3.4 2.7 2.3 2.1 2.3 1.8 1.6 1.7 3 2 0.8 1 0 -1 -2 -3 -3.4 -4 -5 -3.8 Source: Bureau of Labor Statistics, Federal Reserve Bank of Dallas 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 Job Growth is Broad-Based Across Large Texas Metro Areas Nonfarm Employment Index Aug. 2008=100 120 Austin 115 Houston San Antonio Dallas TX Ft. Worth 110 Corpus Christi 105 El Paso U.S.* 100 95 90 2008 2009 2010 2011 *Indexed from U.S. Peak Employment in January 2008 Source: Bureau of Labor Statistics, Federal Reserve Bank of Dallas 2012 2013 2014 2015 Texas Unemployment Rate Low and Falling Percent, SA 10.5 9.5 US unemployment rate 8.5 7.5 6.5 5.7 (Jan.) 5.5 Texas unemployment rate 4.5 4.4 (Jan.) 3.5 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Source: Bureau of Labor Statistics, Federal Reserve Bank of Dallas Job Growth Broad-Based Across Industries Dec/Dec Percent Change 20 Oil & Gas (Job Growth 2011-2014) 15 10 Construction Manufacturing Business Services Finance, Insurance, & Real Estate Trade, Transportation, & Utilities 5 Leisure & Hospitality Information Services Health & Education Government 0 Share of Total Employment -5 (2.6%) (5.5%) (20.1%) (7.6%) (13.4%) (6.1%) Source: Bureau of Labor Statistics, Federal Reserve Bank of Dallas (10.3%) (1.8%) (13.2%) (15.9%) Texas Construction Contract Values Increased Strongly Last Year Real $, Mil 5MMA, SA 8000 7000 Total 6000 5000 4000 Residential 3000 Non Residential 2000 1000 Non Building 0 1990 1992 1994 1996 1998 2000 Source: F.W. Dodge, Federal Reserve Bank of Dallas 2002 2004 2006 2008 2010 2012 2014 TX Home Inventories Remain at Historically Low Levels Months 18 Texas 3.4 16 U.S. 5.2 14 12 10 8 Jan. 2014 6 4 2 0 Source: Multiple Listing Service Mortgage Foreclosures Back to Normal levels but Delinquencies Remain Elevated 5 4.5 TX Delinquencies TX Foreclosures Started US Delinquencies US Foreclosures Started 4 3.5 3 2.5 2.1 2 1.9 1.5 1 0.46 0.5 .35 0.34 0 1998 1999 2000 2001 2002 Source: Mortgage Bankers Association 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Low TX Office Vacancy Rate Likely to Motivate Continued Strength in Office Construction Real, Millions $, 5MMA Percent 450 35 Office and Bank Buildings Contract Value 400 350 30 Office Vacancy Rate 300 25 250 20 200 150 15 100 10 50 0 5 '86 '88 '90 '92 '94 '96 '98 '00 Source: F.W. Dodge, CBRE, Federal Reserve Bank of Dallas '02 '04 '06 '08 '10 '12 '14 TX Manufacturing Production Growth Slow, New Orders Falling Index 100 80 60 40 Feb-15 20 0 -20 -40 -60 Production Volume of New Orders -80 -100 Jun-04 Dec-04 Jun-05 Dec-05 Jun-06 Dec-06 Jun-07 Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Texas Exports Have Weakened in Recent Months as Value of the Dollar has Risen Index, SA, Real Jan. 2000=100 260 Texas Value of the Dollar Index Jan. 1988=100 110.0 105.0 240 100.0 220 95.0 200 90.0 180 Texas 85.0 160 80.0 140 75.0 120 100 70.0 U.S. minus Texas 80 65.0 60.0 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Source: U.S. Census, Bureau of Labor Statistics, WISERtrade Federal Reserve Bank of Dallas Oil Prices Low, Drilling Rig Count In Sharp Decline Number 1000 Nominal $ Rig Count 160 900 140 800 120 700 100 600 80 500 60 400 40 Oil price 300 Gas price(*10) 200 20 0 Source: Oil and Gas Journal, Baker Hughes. Hughes Low Oil Prices Will Likely Dampen TX Job Growth in 2015 • Oil prices have declined over 50% since last July, initial drop from $106 to $80 likely was good for TX economy • Sustained drop from $80 to $50 will hurt TX economy - $50 is below the breakeven point for majority of shale drilling. • Texas GDP growth will likely weaken more than jobs as output per worker in mining is about 4.6 times more than average for the state. Energy’s Share of TX Economy Increased with Shale Drilling Percent, SA 5 Percent 16 Mining as a Share of Nominal Texas GDP 4.5 13.5 % 14 4 12 3.5 10 3 2.5 2 2.7 % Mining as a Share of Total Texas Employment 8 6 1.5 4 1 0.5 0 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 NOTE: GDP values prior to 1997 and employment values prior to 1990 extrapolated from SIC coded data. SOURCES: Bureau of Labor Statistics, Bureau of Economic Analysis, FRB Dallas. 2 0 TX Job Growth Relative to Nation Impacted by Oil Prices Real price, $, monthly average 160 Percent difference in TX and U.S. growth, 12MMA 4 Texas Job Growth Relative to U.S. 3 140 2 120 1 100 0 -1 80 Real Oil Price -2 60 -3 40 -4 20 -5 -6 1982 0 1984 1986 1988 1990 1992 1994 1996 SOURCES: Wall Street Journal, Bureau of Labor Statistics. 1998 2000 2002 2004 2006 2008 2010 2012 2014 Recent Weakness in Leading Index Led By Declining Oil Prices and Rising Dollar Texas Leading Index Components, 3 month change November -January Net Change in Texas Leading Index -3.54 Texas Value of the Dollar -1.03 U.S. Leading Index 0.31 Real Oil Price -1.41 Well Permits -1.30 New Unemployment Claims -0.47 Texas Stock Index 0.15 Help Wanted Index 0.45 Average Weekly Hours -0.25 -4.00 -3.50 -3.00 -2.50 -2.00 -1.50 -1.00 -0.50 0.00 0.50 1.00 Texas Job Growth Likely to be about 1.0–2.0% in 2015, down from 3.4% in 2014 Index (1987=100) 135 Millions of Jobs 12.5 12.0 130 Leading Index 125 11.5 120 11.0 115 10.5 110 Texas Nonfarm Employment and TLI Forecast (with 80% confidence band) 10.0 105 9.5 100 9.0 Jan-00 95 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10 Source: Bureau of Labor Statistics, Federal Reserve Bank of Dallas, author's calculations Jan-12 Jan-14 Jan-16 San Antonio has a Small Share of Jobs in the Oil and Gas Industry El Paso* Brownsville-Harlingen Mcallen-Edinburg-Pharr Sherman-Denison San Antonio Beaumont-Port Arthur Austin-Round Rock Lubbock Dallas-Fort Worth-Arlington Laredo Amarillo College Station-Bryan Houston-Baytown-Sugar Land Corpus Christi Tyler San Angelo Abilene Victoria Longview Odessa Midland 0 5 10 15 20 Share of Employment in Mining Sector *El Paso data as of 2008. All others as of 2012. Source: Bureau of Economic Analysis 25 30 No Clear Boost to San Antonio Job Growth from Eagle Ford Development Y/Y job growth 8 6 Texas San Antonio 4 2 0 -2 -4 -6 1992 1994 1996 1998 2000 SOURCE: Bureau of Labor Statistics, Federal Reserve Bank of Dallas. 2002 2004 2006 2008 2010 2012 2014 Summary • U.S. economy picked up in 2014 – lower oil prices at year end stimulating further gains in consumer spending • TX growth was strong and broad-based in 2014 - initial oil price decline from $106 to $80 had positive impact. • Movement of oil prices from $80 to $50 will have negative impacts but growth likely to remain positive. • This year Texas job growth likely to moderate to 1.0-2.0% • Bottom line: Texas likely to continue to grow but not nearly as strongly as last year.