Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

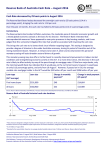

Macro-Financial Review H1 2016 14 June 2016 Key Messages • External Risks remain elevated and have increased since the last Macro-Financial Review • A Brexit would have short term and long-term effects for Ireland • Domestic output continues to grow strongly • High indebtedness across private and public sectors leave the economy vulnerable to higher interest rates and/or economic shocks • In the banking sector, the workout of impaired loans and the disposal of NPLs is ongoing. Domestic banks have returned to profitability but it remains weak and varies at individual bank level • Domestic non-life insurance sector face difficult operating conditions with high-impact firms reporting underwriting losses in 2015 2 • External economic and financial outlook has deteriorated. Domestic growth remains strong. Composition of Irish GDP growth Real GDP growth (global) forecasts, 2016-2017 per cent per cent per cent per cent 15 15 10 10 5 5 1.5 0 0 1.0 1.0 -5 -5 0.5 0.5 -10 -10 0.0 -15 3.0 3.0 2.5 2.5 2.0 2.0 1.5 0.0 WEO Oct 15 WEO Apr 16 WEO Oct 15 WEO Apr 16 2016 2017 euro area UK US Source: IMF World Economic Outlook (WEO) Database. -15 07 09 11 13 15 17f Government expenditure Personal consumption Capital formation Net exports GDP growth rate (rhs) Source: CSO and Central Bank of Ireland. Notes: 2016 and 2017 are forecasts from the Central Bank’s Quarterly Bulletin No. 2 2016. 3 • Corporate and household indebtedness remain high. Leaving economy vulnerable to economic shocks. Private sector debt, consolidated, % of GDP per cent per cent 300 300 250 250 200 200 150 150 Household debt to gross household disposable income – European comparison per cent per cent 300 300 250 250 200 200 150 150 100 100 100 50 50 50 50 0 0 0 0 05 06 07 08 09 10 11 12 13 14 15 Private sector Households NFC (foreign parent) NFC (Irish parent) Source: CSO & Central Bank of Ireland. Romania Slovenia Croatia Czech Republic Italy Germany Austria France Greece Belgium Spain Finland Portugal United Kingdom Ireland Sweden Netherlands Denmark 100 Source: ECB, CSO and CBI. Notes: Debt is defined as loans. Data as at 2015Q4 except for disposable income for Denmark for which 2014Q4 is the latest available. 4 • House price increases and expectations have moderated. Housing supply remains too low. Residential property price growth: National, Dublin & non-Dublin year-on-year change per cent year-on-year change per cent 30 30 25 25 20 Stock listed for sale or rent on Daft.ie number of units number of units 70,000 10,500 20 60,000 9,000 15 10 15 10 50,000 7,500 5 5 40,000 6,000 0 0 -5 -5 30,000 4,500 20,000 3,000 10,000 1,500 -10 -10 -15 -15 -20 -20 -25 -25 -30 -30 06 07 08 National Source: CSO. 09 10 11 12 13 14 National excluding Dublin 15 16Apr Dublin 0 0 07 08 09 10 11 Nat'l stock for sale (lhs) Dublin stock for sale (rhs) 12 13 14 15 16May Nat'l stock for rent (lhs) Dublin stock for rent (rhs) Source: Daft.ie. 5 • Commercial real estate prices increasing at a high rate. Demand driven by foreign investment. Breakdown of commercial property capital and rental value growth by sector year-on-year change per cent year-on-year change per cent Sources of Irish commercial property investment expenditure € billions number of deals 5.0 250 4.5 225 4.0 200 3.5 175 3.0 150 2.5 125 2.0 100 1.5 75 5 1.0 50 0 0 0.5 25 -5 -5 0.0 40 40 35 35 30 30 25 25 20 20 15 15 10 10 5 -10 -10 14Q1 14Q2 14Q3 14Q4 15Q1 15Q2 15Q3 15Q4 16Q1 Retail (capital) Office (capital) Industrial (capital) Source: MSCI/IPD. Retail (rental) Office (rental) Industrial (rental) 0 06 07 08 09 10 11 Pre-2011 investment Private REIT No. of transactions (rhs) 12 13 14 15 16Q1 Other Property co. Institution/fund Source: CBRE Research. Notes: Investment spending relates to individual transactions worth at least €1 million. Breakdown by the original source of funding is only available from 2011. 6 • Non-performing loans continue to decline, but remain high. Higher net interest margins driven by funding costs ,rather than interest income. Domestic banks’ non-performing loans as a share of loans to sector per cent per cent Domestic banks’ net-interest margins per cent per cent 70 70 6 6 60 60 5 5 50 50 4 4 40 40 3 3 30 30 2 2 20 20 1 1 10 10 0 0 0 11 Q3 CRE 12 Q3 13 Q3 14 SME & corporate Q3 15 Q3 16 Mortgages 0 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Net-interest margin (lhs) Interest expense/assets (rhs) Interest income/assets (rhs) Source: Central Bank of Ireland. Notes: Data are consolidated and represent impairment rates for each sector. Source: SNL Financial and Central Bank of Ireland calculations. 7 Conjuctural assessment Impact on procyclicality ConjuncturalBank credit & house prices assessment Credit/housing market developments Side effects Housing supply, unsecured lending & rents Credit/housing market Banking sector developments resilience Changes in lending practises & resilience The Review Household resilience Impact on inproSide effects Changes borrower characteristics & cyclicality resilience to shocks Housing supply, Bank credit & unsecured house prices lending & rents Banking Sector resilience Changes in lending practices & resilience 15 June 10 August End November Open public submissions via website Close public submissions Publication of Review Outcome Central Bank accepting evidence-based submissions: 15 June 2016 – 10 August 2016 8