Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

Truncated variation - its properties and

applications in stochastic analysis

Rafał M. Łochowski

Osaka 2015

Rafał M. Łochowski

Truncated variation

Osaka 2015

1 / 51

Outline

1

Definition and basic properites

2

The truncated variation as a measure of path irregularity

3

Realized volatility estimation

4

Limit theorems for segment crossings

Rafał M. Łochowski

Truncated variation

Osaka 2015

2 / 51

Truncated variation - definition

For a path f : [a; b] → E , where E is a normed space with norm | · |, its

truncated variation is defined with the following formula

n−1

TVc (f , [a; b]) := sup

sup

∑ max {|f (ti +1) − f (ti )| − c , 0} ,

n a≤t1 <t2 <...<tn ≤b i =1

(1)

where c > 0 is the truncation parameter.

Fact

If E is complete (i.e. Banach) space, then TVc (f , [a; b]) < +∞ for any

c > 0 iff f is regulated, i.e. it has right and left limits.

Rafał M. Łochowski

Truncated variation

Osaka 2015

3 / 51

Truncated variation - basic properties

Let kf − g k∞ := supt ∈[a;b] |f (t ) − g (t )| .

From the triangle inequality, for g such that kf − g k∞ ≤ c /2, we

immediately get

|f (ti +1 ) − f (ti )| − c ≤ |g (ti +1 ) − g (ti )|

and from this

TVc (f , [a; b]) ≤ TV (g , [a; b]) ,

(2)

where TV (g , [a; b]) is just the (total) variation of g .

Rafał M. Łochowski

Truncated variation

Osaka 2015

4 / 51

Truncated variation - basic properties

Let kf − g k∞ := supt ∈[a;b] |f (t ) − g (t )| .

From the triangle inequality, for g such that kf − g k∞ ≤ c /2, we

immediately get

|f (ti +1 ) − f (ti )| − c ≤ |g (ti +1 ) − g (ti )|

and from this

TVc (f , [a; b]) ≤ TV (g , [a; b]) ,

(2)

where TV (g , [a; b]) is just the (total) variation of g .

Remark

The fact stated on the previous slide becomes clear when one recalls

that the family of regulated functions attaing values in a Banach space

coincides with the family of functions which may be uniformly

approximated by finite variation functions (equivalently: by step

functions) with an arbitrary accuracy.

Rafał M. Łochowski

Truncated variation

Osaka 2015

4 / 51

Truncated variation - variational property

When f is a real function, then the bound (2) is attainable, i.e. there

exists a function f c : [a; b] → R, such that kf − g k∞ ≤ c /2 and

TVc (f , [a; b]) = TV (f c , [a; b])

Thus, we have the following variational property of TV c :

TVc (f , [a; b]) =

Rafał M. Łochowski

inf

kf −g k∞ ≤c /2

Truncated variation

TV (g , [a; b]) .

(3)

Osaka 2015

5 / 51

Truncated variation - variational property

When f is a real function, then the bound (2) is attainable, i.e. there

exists a function f c : [a; b] → R, such that kf − g k∞ ≤ c /2 and

TVc (f , [a; b]) = TV (f c , [a; b])

Thus, we have the following variational property of TV c :

TVc (f , [a; b]) =

inf

kf −g k∞ ≤c /2

TV (g , [a; b]) .

(3)

Remark

It is an open question if property (3) holds in other spaces than R. Even

for spaces E where the equality does not hold, it seems to be interesting

to assess how much the left side of (3) differs from the right side.

Rafał M. Łochowski

Truncated variation

Osaka 2015

5 / 51

Truncated variation - asymptotics

From definition (1) or variational property (3) (for real paths) we

naturally have that

lim TVc (f , [a; b]) = TV (f , [a; b]) .

c ↓0

If TV (f , [a; b]) = +∞ (which is common for many important families of

stochastic processes) the rate of the divergence of TVc (f , [a; b]) to +∞

as c ↓ 0 may be viewed as the measure of irregularity of the path f

Rafał M. Łochowski

Truncated variation

Osaka 2015

6 / 51

p−variation

Naturally, in analysis there were many other notions of variations

introduced. One of the most natural seems to be the p−variation,

p > 0, defined as

n−1

p

V (f , [a; b]) := sup

n

|f (ti +1 ) − f (ti )|p .

∑

a≤t <t <...<t ≤b

sup

1

2

n

(4)

i =1

For any f , if Vp (f , [a; b]) < +∞ and q > p > 0, then Vq (f , [a; b]) < +∞.

Rafał M. Łochowski

Truncated variation

Osaka 2015

7 / 51

p−variation

Naturally, in analysis there were many other notions of variations

introduced. One of the most natural seems to be the p−variation,

p > 0, defined as

n−1

p

V (f , [a; b]) := sup

n

|f (ti +1 ) − f (ti )|p .

∑

a≤t <t <...<t ≤b

sup

1

2

n

(4)

i =1

For any f , if Vp (f , [a; b]) < +∞ and q > p > 0, then Vq (f , [a; b]) < +∞.

This observation makes meaningful to define the variation index

Indvar (f ) := inf {p : Vp (f , [a; b]) < +∞} ,

which may be also viewed as a measure of irregularity of the path - the

greater Indvar (f ) , the more irregular path.

Rafał M. Łochowski

Truncated variation

Osaka 2015

7 / 51

p−variation

Naturally, in analysis there were many other notions of variations

introduced. One of the most natural seems to be the p−variation,

p > 0, defined as

n−1

p

V (f , [a; b]) := sup

n

|f (ti +1 ) − f (ti )|p .

∑

a≤t <t <...<t ≤b

sup

1

2

n

(4)

i =1

For any f , if Vp (f , [a; b]) < +∞ and q > p > 0, then Vq (f , [a; b]) < +∞.

This observation makes meaningful to define the variation index

Indvar (f ) := inf {p : Vp (f , [a; b]) < +∞} ,

which may be also viewed as a measure of irregularity of the path - the

greater Indvar (f ) , the more irregular path.

Remark

If f is a step function then Indvar (f ) = 0, otherwise usually Indvar (f ) ≥ 1.

Rafał M. Łochowski

Truncated variation

Osaka 2015

7 / 51

The variation index vs. the asymptotics of the

truncated variation

Let G ([a; b]) denote the set of real-valued, regulated functions

f : [a; b] → R.

Rafał M. Łochowski

Truncated variation

Osaka 2015

8 / 51

The variation index vs. the asymptotics of the

truncated variation

Let G ([a; b]) denote the set of real-valued, regulated functions

f : [a; b] → R.

For p ≥ 1 let V p ([a; b]) denote the subset of G ([a; b]) consisting of

functions with finite p−variation.

Rafał M. Łochowski

Truncated variation

Osaka 2015

8 / 51

The variation index vs. the asymptotics of the

truncated variation

Let G ([a; b]) denote the set of real-valued, regulated functions

f : [a; b] → R.

For p ≥ 1 let V p ([a; b]) denote the subset of G ([a; b]) consisting of

functions with finite p−variation.

Next, for p ≥ 1 let U p ([a; b]) denote the subset of G ([a; b]) consisting

of functions f for which

lim sup c p−1 · TVc (f , [a; b]) < +∞.

c ↓0

Rafał M. Łochowski

Truncated variation

Osaka 2015

8 / 51

The variation index vs. the asymptotics of the

truncated variation

Let G ([a; b]) denote the set of real-valued, regulated functions

f : [a; b] → R.

For p ≥ 1 let V p ([a; b]) denote the subset of G ([a; b]) consisting of

functions with finite p−variation.

Next, for p ≥ 1 let U p ([a; b]) denote the subset of G ([a; b]) consisting

of functions f for which

lim sup c p−1 · TVc (f , [a; b]) < +∞.

c ↓0

We have U 1 ([a; b]) = V 1 ([a; b]) and for any 1 < p < q we have

V p ([a; b]) ( U p ([a; b]) ( V q ([a; b]) .

Rafał M. Łochowski

Truncated variation

Osaka 2015

8 / 51

Irregularity of a typical Brownian path

If B is a standard Brownian motion, then Indvar (B ) = 2 with probability

1.

However, an old result of P. Lévy states that V2 (B , [a; b]) = +∞ with

probability 1, thus B ∈

/ V 2 ([0; t ]) with probability 1.

Rafał M. Łochowski

Truncated variation

Osaka 2015

9 / 51

Irregularity of a typical Brownian path

If B is a standard Brownian motion, then Indvar (B ) = 2 with probability

1.

However, an old result of P. Lévy states that V2 (B , [a; b]) = +∞ with

probability 1, thus B ∈

/ V 2 ([0; t ]) with probability 1.

On the other hand, in [LM2013] it was proven that for any t > 0,

lim c · TVc (B , [0; t ]) = t ,

c →0

with probability 1,

thus B ∈ U 2 ([0; t ]) with probability 1.

Rafał M. Łochowski

Truncated variation

Osaka 2015

9 / 51

Irregularity of a typical Brownian path

If B is a standard Brownian motion, then Indvar (B ) = 2 with probability

1.

However, an old result of P. Lévy states that V2 (B , [a; b]) = +∞ with

probability 1, thus B ∈

/ V 2 ([0; t ]) with probability 1.

On the other hand, in [LM2013] it was proven that for any t > 0,

lim c · TVc (B , [0; t ]) = t ,

c →0

with probability 1,

thus B ∈ U 2 ([0; t ]) with probability 1.

Remark

In [LM2013] there was a more general fact proven: if Xt , t ≥ 0, is a

continuous semimartingale with quadratic variation < · > then for any

t > 0,

lim c · TVc (X , [0; t ]) =< X >t , with probability 1.

c →0

Rafał M. Łochowski

Truncated variation

Osaka 2015

9 / 51

Irregularity of a typical Brownian path measured

by ϕ− variation

For a continuous, increasing function ϕ : [0; +∞) → [0; +∞) such that

ϕ (0) = 0 one may define ϕ−variation as

n−1

ϕ

V (f , [a; b]) := sup

sup

∑ ϕ (|f (ti +1) − f (ti )|) .

(5)

n a≤t1 <t2 <...<tn ≤b i =1

Rafał M. Łochowski

Truncated variation

Osaka 2015

10 / 51

Irregularity of a typical Brownian path measured

by ϕ− variation

For a continuous, increasing function ϕ : [0; +∞) → [0; +∞) such that

ϕ (0) = 0 one may define ϕ−variation as

n−1

ϕ

V (f , [a; b]) := sup

∑ ϕ (|f (ti +1) − f (ti )|) .

sup

(5)

n a≤t1 <t2 <...<tn ≤b i =1

An old result of S. J. Taylor [T1972] states that

ϕ0 (x ) = x 2 / ln (max [ln (1/x ) , 2])

is a function with the greatest order in the neighbourhood of 0 and such

that for any t > 0,

Vϕ0 (B , [0; t ]) < +∞,

Rafał M. Łochowski

with probability 1.

Truncated variation

Osaka 2015

10 / 51

Irregularity of a typical Brownian path measured

by ϕ− variation, cont.

ϕ(x )

Moreover, for any function ϕ such that limx ↓0 ϕ (x ) = +∞ and t > 0 we

0

have

Vϕ (B , [0; t ]) = +∞,

with probability 1.

Remark

The asymptotics of the truncated variation for functions with finite

ϕ−variation is still to be investigated.

Rafał M. Łochowski

Truncated variation

Osaka 2015

11 / 51

Truncated variation, p−variation and ϕ−variation

norms of a Brownian path

The already mentioned irregularity results for the Brownian paths may

be stated using p−variation, ϕ−variation and truncated variation

norms, defined as

kB kp−var ,[0;T ] := (Vp (B , [0; T ]))1/p ,

for p ≥ 1,

kB kϕ−var ,[0;T ] := inf {λ > 0 : Vϕ (B /λ, [0; T ]) ≤ 1} ,

and

kB kTV ,p,[0;T ] := sup c

p−1

1/p

· TV (B , [0; T ])

,

c

for p ≥ 1.

c >0

Rafał M. Łochowski

Truncated variation

Osaka 2015

12 / 51

Truncated variation, p−variation and ϕ−variation

norms of a Brownian path

The already mentioned irregularity results for the Brownian paths may

be stated using p−variation, ϕ−variation and truncated variation

norms, defined as

kB kp−var ,[0;T ] := (Vp (B , [0; T ]))1/p ,

for p ≥ 1,

kB kϕ−var ,[0;T ] := inf {λ > 0 : Vϕ (B /λ, [0; T ]) ≤ 1} ,

and

kB kTV ,p,[0;T ] := sup c

p−1

1/p

· TV (B , [0; T ])

,

c

for p ≥ 1.

c >0

Remark

One always has

kB kTV ,p,[0;T ] ≤ kB kp−var ,[0;T ] .

Rafał M. Łochowski

Truncated variation

Osaka 2015

12 / 51

Truncated variation, p−variation and ϕ−variation

norms of a Brownian path, cont.

For such defined p−variation, ϕ−variation and truncated variation

norms, we have

(

< +∞ if p ∈ (2; +∞),

kB kp,[0;T ] =

+∞ if p ∈ [1; 2];

kB kϕ,[0;T ] =

and

(

< +∞ if

+∞ if

ϕ(x )

limx ↓0 ϕ (x ) < +∞,

0

ϕ(x )

limx ↓0 ϕ (x ) = +∞

0

(

< +∞ if p ∈ [2; +∞),

kB kTV ,p,[0;T ] =

+∞ if p ∈ [1; 2).

Rafał M. Łochowski

Truncated variation

Osaka 2015

13 / 51

Truncated variation vs. p−variation norms of a

fractional Brownian path

Similarly, for a fractional Brownian BH motion with the Hurst parameter

H ∈ (0; 1) we have

(

< +∞ if p ∈ (1/H ; +∞),

kBH kp,[0;T ] =

+∞ if p ∈ [1; 1/H ]

and

(

< +∞ if p ∈ [1/H ; +∞),

kBH kTV ,p,[0;T ] =

+∞ if p ∈ [1; 1/H ).

Thus, for each T > 0

BH ∈ U 1/H ([0; T ]) \V 1/H ([0; T ]) ,

Rafał M. Łochowski

Truncated variation

with probability1.

Osaka 2015

14 / 51

Young integrals of irregular paths

Using truncated variation techniques it is possible to prove the following,

stronger version of Young’s result from 1936 [Young, 1936]:

Theorem

Let f , g : [a; b] → R be two functions with no common points of

discontinuity. If f ∈ U p ([a; b]) and g ∈ U q ([a; b]) , where p > 1, q > 1,

´b

p−1 + q −1 > 1, then the Riemann Stieltjes a f (t ) dg (t ) exists.

Moreover, there exist a constant Cp,q , depending on p and q only, such

that

ˆ b

f

(

t

)

d

g

(

t

)

−

f

(

a

)

[

g

(

b

)

−

g

(

a

)]

a

p−p/q

1+p/q −p

≤ Cp,q kf kTV ,p,[a;b] kf kosc ,[a;b] kg kTV ,q ,[a;b] ,

where kf kosc ,[a;b] := supa≤s<t ≤b |f (t ) − f (s)|.

Rafał M. Łochowski

Truncated variation

Osaka 2015

15 / 51

How to calculate the truncated variation?

There exists an algorithm based on drawdown and drawup times. Let

us define

TUc f = inf t ∈ (a; b] : f (t ) − inf f (s) > c

a≤s≤t

TDc f

Rafał M. Łochowski

= inf t ∈ (a; b] : sup f (s) − f (t ) > c

a≤s≤t

Truncated variation

Osaka 2015

16 / 51

How to calculate the truncated variation?

There exists an algorithm based on drawdown and drawup times. Let

us define

TUc f = inf t ∈ (a; b] : f (t ) − inf f (s) > c

a≤s≤t

TDc f

If min

TUc f <

= inf t ∈ (a; b] : sup f (s) − f (t ) > c

a≤s≤t

TUc f , TDc f = +∞, then TVc (f , [a; b]) = 0. If not, assuming

TDc f we define TDc ,−1 f = a and then for k = 0, 1, 2, . . .

(

TUc ,k f = inf

)

t ∈ (TDc ,k −1 f ; b] : f (t ) −

inf

TDc ,k −1 f ≤s≤t

f (s ) > c

(

TDc ,k f = inf

Rafał M. Łochowski

that

,

)

t ∈ (TUc ,k f ; b] :

sup

f (s) − f (t ) > c

.

TUc ,k f ≤s≤t

Truncated variation

Osaka 2015

16 / 51

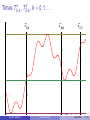

Times TUc ,k , TDc ,k , k = 0, 1, . . .

c

TU,0

2.5

c

TD,0

c

TU,1

2.0

c

1.5

c

1.0

0.5

0.0

c

-0.5

Rafał M. Łochowski

Truncated variation

Osaka 2015

17 / 51

Calculation of the truncated variation, cont.

Now, to calculate the truncated variation we define

mk =

inf

s∈[TD ,k −1 ;TU ,k ]

f (s),

Mk =

inf

s∈[TU ,k ;TD ,k ]

f (s),

and for t such that t ∈ [TU ,k ; TD ,k ] we have

k −1

TVc (f , [a; t ]) =

k −1

∑ (Mi − mi − c ) + ∑ (Mi − mi +1 − c )

i =0

+

(6)

i =0

sup

f ( s ) − mk − c .

s∈[TUc ,k f ,t ]

Similarly, for t such that t ∈ [TD ,k ; TU ,k +1 ] we have

k −1

k

TVc (f , [a; t ]) =

∑ (Mi − mi − c ) +

i =0

+ Mk −

Rafał M. Łochowski

inf

∑ (Mi − mi +1 − c )

(7)

i =0

f (s ) − c .

s∈[TDc ,k f ,t ]

Truncated variation

Osaka 2015

18 / 51

Stopping times TUc ,k , TDc ,k , k = 0, 1, . . .

If Xt , t ≥ 0, is a stochastic process with càdlàg (or even regulated!)

trajectories, adapted to the filtration Ft , t ≥ 0, then for each trajectory

f = X (ω) the just defined times TUc ,k , TDc ,k , k = 0, 1, . . . are stopping

times such that

lim TUc ,k = lim TDc ,k = +∞,

k →+∞

Rafał M. Łochowski

k →+∞

Truncated variation

with probability 1.

Osaka 2015

19 / 51

Stopping times TUc ,k , TDc ,k , k = 0, 1, . . .

If Xt , t ≥ 0, is a stochastic process with càdlàg (or even regulated!)

trajectories, adapted to the filtration Ft , t ≥ 0, then for each trajectory

f = X (ω) the just defined times TUc ,k , TDc ,k , k = 0, 1, . . . are stopping

times such that

lim TUc ,k = lim TDc ,k = +∞,

k →+∞

k →+∞

with probability 1.

To see this, note that for any t > 0 there exists such K < +∞ that

TUc ,K > t and TDc ,K > t . Otherwise we would obtain two infinite

∞

∞

sequences (sk )k =1 , (Sk )k =1 such that 0 ≤ s1 < S1 < s2 < S2 < ... < t

and f (Sk ) − f (sk ) ≥ 12 c . But this is a contradiction, since f is a

∞

∞

regulated function and (f (sk ))k =1 , (f (Sk ))k =1 have a common limit.

Rafał M. Łochowski

Truncated variation

Osaka 2015

19 / 51

Calculation of the truncated variation of a process

with continuous trajectories

When Xt , t ≥ 0, is a stochastic process with continuous trajectories

then for any t > 0, TVc (X , [0; t ]) may be calculated with the stochastic

sampling scheme based on the stopping times TUc ,k , TDc ,k , k = 0, 1, . . . .

Indeed, for continuous f = X (ω) we have XTUc ,k (ω) = f (TUc ,k ) = mk + c

and XTDc ,k (ω) = f (TDc ,k ) = Mk − c , hence from formulas (6) and (7) we

have

TVc X , [0; TUc ,k ] =

k −1 XTDc ,i − XTUc ,i + c +

∑

i =0

k −1 XTDc ,i − XTUc ,i +1 + c .

∑

i =0

Similarly,

k

TV

c

X , [0; TDc ,k ]

=

∑

i =0

Rafał M. Łochowski

XTDc ,i − XTUc ,i + c +

Truncated variation

k −1 ∑

i =0

XTDc ,i − XTUc ,i +1 + c .

Osaka 2015

20 / 51

Realized volatility estimation

If Xt , t ≥ 0, is a continuous semimartingale then the (mentioned

already) relation

c · TVc (X , [0; t ]) →< X >t ,

with probability 1

(8)

(in the uniform convergence topology on compacts) and the stated

algorithm provides us with a tool for the realized volatility estimation.

Rafał M. Łochowski

Truncated variation

Osaka 2015

21 / 51

Realized volatility estimation

If Xt , t ≥ 0, is a continuous semimartingale then the (mentioned

already) relation

c · TVc (X , [0; t ]) →< X >t ,

with probability 1

(8)

(in the uniform convergence topology on compacts) and the stated

algorithm provides us with a tool for the realized volatility estimation.

Remark

The rate of convergence in (8) is better than the rate of the usual

algorithms based on the calendar time or business time sampling (this

was proved at least for some class of diffusions), and is of the same

order as the order of tick time sampling schemes, which are special

case of stochastic sampling schemes for realized volatility estimation

introduced by Masaaki Fukasawa [F2010].

Rafał M. Łochowski

Truncated variation

Osaka 2015

21 / 51

Rate of convergence in (8)

Let Xt , t ≥ 0 be the strong solution of the SDE

dXt = µ (Xt ) dt + σ (Xt ) dBt , where B is a standard Brownian motion

and µ, σ > 0 satisfy ”usual” conditions guaranteeing the existence

uniqueness of the strong solution of SDE. In [LM2013] the following

result was proven

1

c

(c · TVc (X , [0; t ]) − < X >t ) ⇒ W<X >t /3 ,

where W is another standard Brownian motion, independent from B

and the convergence ⇒ is understood as the stable convergence in the

uniform convergence topology on compacts.

Rafał M. Łochowski

Truncated variation

Osaka 2015

22 / 51

Stochastic sampling schemes for realized volatility

estimation

Masaaki Fukasawa considered general stochastic sampling schemes

and obtained similar rates of convergence for tick sampling.

He considered a continuous semimartingale X = A + M , where Mt ,

t ≥ 0, is a continuous local martingale adapted to some filtration Ft ,

t ≥ 0,´and At , t ≥ 0, is a finite variation process such that

t

At = 0 ψs d < M >s , where ψs , t ≥ 0, is locally bounded, left

continuous process adapted to Ft and a sequence of Ft −stopping

times 0 = τ0 < τ1 < . . . such that for every T > 0

Nτ (t ) := max {k ≥ 0 : τk > t } < +∞,

Rafał M. Łochowski

Truncated variation

with probability 1.

Osaka 2015

23 / 51

Stochastic sampling schemes for realized volatility

estimation, cont.

The statistics

Nτ (t )−1

RVτ (t ) :=

∑

(Xτk +1 − Xτk )2

k =0

is an estimator of < X >t and the rate of convergence of this statistics

depends on the sequence τ = {τ0 < τ1 < . . . } .

The best rates of convergence one obtains taking e.g. tick sampling, i.e.

τc0 = 0 and for k = 0, 1, . . .

n

o

τck +1 = inf t > tk : Xt − Xτck > c ,

and we have stable convergence to a non-trivial limit of the processes

1

c

Rafał M. Łochowski

(RVτc (t ) − < X >t ) .

Truncated variation

Osaka 2015

24 / 51

Stochastic sampling schemes for realized volatility

estimation, general remarks

With the tick time sampling (based on stopping times τck ) (or the

truncated variation sampling based on stopping times TUc ,k , TDc ,k ,)

we need to control the process very precisely (no unobserved big

fluctuations between consecutive samplings) like in the case of

the calendar time sampling τk = k /n.

As a reward for this we obtain a better mode of the first order

convergence (almost sure convergence instead of the

convergence in probability) and a better asymptotics of the second

order convergence.

This is no problem as long we assume that we are able to observe

rounded values of the process X at any time.

The tick time sampling or the truncated variation sampling are

robust to the price rounding (market microstructure noise).

Rafał M. Łochowski

Truncated variation

Osaka 2015

25 / 51

Variational properties of the tick sampling scheme

The tick time sampling scheme has also interesting property regarding

the total variation of the càdlàg process X̂ c defined as

X̂tc = Xτck ,

where k = max {i = 0, 1, 2, . . . : τci ≤ t } .

This process approximates the process X with accuracy c and we have

TV X̂ c , [0; t ] = c · Nτ (t )

and

RVτc (t ) := c 2 · Nτc (t ) = c · TV X̂ c , [0; t ] .

Thus, recalling

the convergence results for RVcτc (t ) we get that

c

TV X̂ , [0; t ] has the same magnitude as TV (X , [0; t ]) and it

approximates uniformly X with accuracy c (which differs from the

optimal accuracy for a process with the total vatiation TVc (X , [0; t ]) by

factor 2).

Rafał M. Łochowski

Truncated variation

Osaka 2015

26 / 51

The truncated variation and segment crossings

The truncated variation appears to be esspecially relevant for the

investigation of the numbers of segment crossings. First, let us recall

the Banch Indicatrix theorem. If f : [a, b] → R is a continuous function

then

ˆ

N y (f , [a; b]) dy ,

TV (f , [a; b]) =

R

where

N y (f , [a; b]) := card {x ∈ [a; b] : f (x ) = y }

is called the Banach indicatrix. A generalisation of this result for the

case of regulated f is possible.

Unfortunately, when TV (f , [a; b]) = +∞ this result seems to be useless.

Rafał M. Łochowski

Truncated variation

Osaka 2015

27 / 51

The truncated variation and segment crossings,

cont.

However, when instead of considering the level crossings, one

considers segment crossings and instead of considering the total

variation one considers the truncated variation then one gets the

following result.

For any regulated f : [a; b] → R and c > 0,

ˆ

y

c

TV (f , [a; b]) =

nc (f , [a; b]) dy .

(9)

R

Here,

y

nc (f , [a; b]) = number of times that f crosses the segment [y ; y + c ].

(10)

Rafał M. Łochowski

Truncated variation

Osaka 2015

28 / 51

Segment crossings - precise definition

To be more precise, we define

y

y

y

nc (f , [a, b]) = dc (f , [a, b]) + uc (f , [a, b]) .

y

dc (f , [a, b]) = number of downcrossings the segment [y ; y + c ]..

σ0 = a, and for k = 0, 1, . . .

νk = inf {t > σk : f (t ) > y + c }

σk +1 = inf {t > νk : f (t ) < y } .

Now we define

y

dc (f , [a, b]) = max {k : σk ≤ b} .

Rafał M. Łochowski

Truncated variation

Osaka 2015

29 / 51

Segment crossings - precise definition

To be more precise, we define

y

y

y

nc (f , [a, b]) = dc (f , [a, b]) + uc (f , [a, b]) .

y

dc (f , [a, b]) = number of downcrossings the segment [y ; y + c ]..

σ0 = a, and for k = 0, 1, . . .

νk = inf {t > σk : f (t ) > y + c }

σk +1 = inf {t > νk : f (t ) < y } .

Now we define

y

dc (f , [a, b]) = max {k : σk ≤ b} .

y

dc (f , [a, b]) = number of downcrossings the segment [y ; y + c ].

σ̃0 = a, and for k = 0, 1, . . .

ν̃k = inf {t > σ̃k : f (t ) < y }

σ̃k +1 = inf {t > ν̃k : f (t ) > y + c } .

y

uc (f , [a, b]) = max {k : σ̃k ≤ b} .

Rafał M. Łochowski

Truncated variation

Osaka 2015

29 / 51

Limit theorems for segment crossings

Relation (9), linking the truncated variation with the numbers of

segment crossings, allows to obtain, for relatively broad spectrum of

stochastic processes, limit theorems for the numbers of segment

crossings of these processes.

For example, for a continuous semimartingale Xt , t ≥ 0, using the

already mentioned convergence

c · TVc (X , [0; t ]) →< X >t ,

with probability 1

one obtains the convergence

ˆ

y

c · nc (X , [0; t ]) dy →< X >t ,

with probability 1.

R

It is also possible to make some of the levels more important than

others, by introducing continuous density g : R → R, and obtain

ˆ

ˆ

y

c · nc

(X , [0; t ]) g (y )dy →

t

g (Xs ) d < X >s ,

with probability 1.

0

R

Rafał M. Łochowski

Truncated variation

Osaka 2015

(11)

30 / 51

Limit theorems for segment crossings, diffusions

Similalry, from the already mentioned convergence

1

c

TV (X , [0; t ]) −

c

< X >t

⇒ W<X >t /3 ,

for Xt , t ≥ 0, being the strong solution of the SDE

dXt = µ (Xt ) dt + σ (Xt ) dBt , where B is a standard Brownian motion

and µ, σ > 0 satisfy ”usual” conditions guaranteeing the existence

uniqueness of the strong solution of SDE, and any continuous function

g : R → R, the following convergence of the integrated numbers of

segment crossings was obtained ([LG2014]):

ˆ

y

nc

(X , [0; t ]) g (y )dy −

R

1

c

ˆ

t

ˆ

g (Xs ) d < X >s

0

⇒

t

g (Xs ) W <X >t ,

3

0

where B and W are two independent standard Brownian motions.

Rafał M. Łochowski

Truncated variation

Osaka 2015

31 / 51

Limit theorems for segment down-, up- crossings,

diffusions

Together with the convergence of segment crossings, one has (obvious)

first order convergence of segment down- and up- crossings (since

y

y

uc (X , [0; t ]) − dc (X , [0; t ]) ∈ {−1, 0, 1}):

ˆ

y

c · uc

(X , [0; t ]) g (y )dy →

R

1

2

ˆ

t

g (Xs ) d < X >s ,

with probability 1.

0

But in the case of the second order convergence an interesting

correction term (the Stratonovich integral) appears:

ˆ

y

uc

R

1

ˆ

t

g (Xs ) d < X >s

(X , [0; t ]) g (y )dy −

2·c 0

ˆ

ˆ

1 t

1 t

⇒

g (Xs ) W <X >t +

g (Xs ) ◦ dXs ,

2

0

3

2

0

where B and W are two independent standard Brownian motions.

Rafał M. Łochowski

Truncated variation

Osaka 2015

32 / 51

Segment crossings and local times of diffusions

y

Let Lt (X ) be the local time of X at y ∈ R and g : R → R be a

continuous function. Recalling the occupation times formula

ˆ

ˆ

t

y

g (Xs ) d < X >s =

0

we get

ˆ y

nc

(X , [0; t ]) −

R

Rafał M. Łochowski

g (y ) Lt (X ) dy .

R

1

c

y

Lt

ˆ t

(X ) g (y ) dy ⇒

g (Xs ) W <X >t .

0

Truncated variation

3

Osaka 2015

33 / 51

Segment crossings and local times of diffusions

y

Let Lt (X ) be the local time of X at y ∈ R and g : R → R be a

continuous function. Recalling the occupation times formula

ˆ

ˆ

t

y

g (Xs ) d < X >s =

0

we get

ˆ y

nc

(X , [0; t ]) −

R

g (y ) Lt (X ) dy .

R

1

c

y

Lt

ˆ t

(X ) g (y ) dy ⇒

g (Xs ) W <X >t .

0

3

On the other hand, we have the following convergence ([Kasahara,

1980] for a standard Brownian motion, [LG2014, Theorem 4.5] for

diffusions)

√

1 y

y

c nc (X , [0; t ]) − Lt (X ) ⇒ WLy (X ) .

t

c

Rafał M. Łochowski

Truncated variation

Osaka 2015

33 / 51

Segment crossings and local times of diffusions

y

Let Lt (X ) be the local time of X at y ∈ R and g : R → R be a

continuous function. Recalling the occupation times formula

ˆ

ˆ

t

y

g (Xs ) d < X >s =

0

we get

ˆ y

nc

(X , [0; t ]) −

R

g (y ) Lt (X ) dy .

R

1

c

y

Lt

ˆ t

(X ) g (y ) dy ⇒

g (Xs ) W <X >t .

0

3

On the other hand, we have the following convergence ([Kasahara,

1980] for a standard Brownian motion, [LG2014, Theorem 4.5] for

diffusions)

√

1 y

y

c nc (X , [0; t ]) − Lt (X ) ⇒ WLy (X ) .

t

c

y

Thus we see that integrating differences nc (X , [0; ·]) − 1c Ly (X ) we get

√

much faster convergence (multiplication by c is no needed).

Rafał M. Łochowski

Truncated variation

Osaka 2015

33 / 51

”Meta-theorem”, almost sure convergence

For a process Xt , t ≥ 0, let us denote TVc (X , ·) := TVc (X , [0; ·]) and

nca (X , ·) := nca (X , [0; ·]).

Rafał M. Łochowski

Truncated variation

Osaka 2015

34 / 51

”Meta-theorem”, almost sure convergence

For a process Xt , t ≥ 0, let us denote TVc (X , ·) := TVc (X , [0; ·]) and

nca (X , ·) := nca (X , [0; ·]).

Theorem (M1)

Let Xt , t ≥ 0, be a càdlàg process and assume that there exists an

increasing function ϕ : (0; +∞) → (0; +∞) , such that limc →0+ ϕ (c ) = 0,

and a càdlàg process ζt , t ≥ 0, with locally finite variation, such that the

following convergence holds

ϕ (c ) TVc (X , ·) → ζ.

Then for any continuous function f : R → R we have the following

convergence

ˆ

ˆ

nca (X , ·)f

ϕ (c )

(a) da →

f (Xt − ) dζt .

0

R

Rafał M. Łochowski

·

Truncated variation

Osaka 2015

34 / 51

”Meta-theorem”, stable convergence

Theorem (M2)

Let Xt , t ≥ 0, be a càdlàg process and assume that there exists an

increasing function ϕ : (0; +∞) → (0; +∞) , with limc →0+ ϕ (c ) = 0, and

a càdlàg process ζt , t ≥ 0, with locally finite variation, such that the

following convergence holds

ϕ (c ) TV c (X , ·) ⇒ ζ

then for any continuous function f : R → R we have the following

convergence

ˆ

ˆ

nca (X , ·)f (a)da

ϕ (c )

⇒

f (Xt − ) dζt .

0

R

Rafał M. Łochowski

·

Truncated variation

Osaka 2015

35 / 51

Self-similar processes

Theorem (SsP)

Let Xt , t ≥ 0, be a càdlàg process such that it has stationary

increments. Next, assume that X is a self-similar proces, that is, there

exists β ∈ (0; 1) such that

n

A

−β

o

XAt , t ≥ 0 =d {Xt , t ≥ 0}

for any A > 0. Additionally we assume that for some c > 0,

ETVc (X , [0, 1]) < +∞ and that the tail σ-field is trivial. Then

c 1/β−1 TVc (X , ·) → C · Id .

Rafał M. Łochowski

Truncated variation

Osaka 2015

36 / 51

Lévy processes

Theorem (LP1)

Let Xt , t ≥ 0, be a Lévy process which has infinite total variation and is

no monotonic on any non-degenerate interval. Moreover, assume that

E sup0≤t <T c0 X Xt < +∞ for some c0 > 0, where we define

D

TDc X := inf t ≥ 0 : sup0≤s≤t Xs − Xt > c ,

Rafał M. Łochowski

Truncated variation

θcU := ETDc X

Osaka 2015

37 / 51

Lévy processes

Theorem (LP1)

Let Xt , t ≥ 0, be a Lévy process which has infinite total variation and is

no monotonic on any non-degenerate interval. Moreover, assume that

E sup0≤t <T c0 X Xt < +∞ for some c0 > 0, where we define

D

TDc X := inf t ≥ 0 : sup0≤s≤t Xs − Xt > c ,

ξcU := sup0≤s<t <TDc X (Xt − Xs − c )+ ,

Rafał M. Łochowski

Truncated variation

θcU := ETDc X

ηcU := EξcU .

Osaka 2015

37 / 51

Lévy processes

Theorem (LP1)

Let Xt , t ≥ 0, be a Lévy process which has infinite total variation and is

no monotonic on any non-degenerate interval. Moreover, assume that

E sup0≤t <T c0 X Xt < +∞ for some c0 > 0, where we define

D

TDc X := inf t ≥ 0 : sup0≤s≤t Xs − Xt > c ,

ξcU := sup0≤s<t <TDc X (Xt − Xs − c )+ ,

θcU := ETDc X

ηcU := EξcU .

If for

χU (c ) := θcU /ηcU

and for any u > 0, P ξcU ≤ u /χU (c ) /θcU → 1 as c → 0+, then we

have the following convergence

χU (c ) TVc (X , ·) ⇒ 2 · Id .

Rafał M. Łochowski

Truncated variation

Osaka 2015

37 / 51

Lévy processes, cont.

Theorem (LP2)

Let Xt , t ≥ 0, be a Lévy process which has infinite total variation and is

no monotonic on any non-degenerate interval. Moreover, assume that

E sup0≤t <T c0 X Xt < +∞ for some c0 > 0, where we define

D

TUc X := inf {t ≥ 0 : Xt − inf0≤s≤t Xs > c } ,

Rafał M. Łochowski

Truncated variation

θcD := ETDc X

Osaka 2015

38 / 51

Lévy processes, cont.

Theorem (LP2)

Let Xt , t ≥ 0, be a Lévy process which has infinite total variation and is

no monotonic on any non-degenerate interval. Moreover, assume that

E sup0≤t <T c0 X Xt < +∞ for some c0 > 0, where we define

D

TUc X := inf {t ≥ 0 : Xt − inf0≤s≤t Xs > c } ,

ξcD := sup0≤s<t <TUc X (Xs − Xt − c )+ ,

Rafał M. Łochowski

Truncated variation

θcD := ETDc X

ηcD := EξcD .

Osaka 2015

38 / 51

Lévy processes, cont.

Theorem (LP2)

Let Xt , t ≥ 0, be a Lévy process which has infinite total variation and is

no monotonic on any non-degenerate interval. Moreover, assume that

E sup0≤t <T c0 X Xt < +∞ for some c0 > 0, where we define

D

TUc X := inf {t ≥ 0 : Xt − inf0≤s≤t Xs > c } ,

ξcD := sup0≤s<t <TUc X (Xs − Xt − c )+ ,

θcD := ETDc X

ηcD := EξcD .

If for

χD (c ) := θcD /ηcD

and for any u > 0, P (ξcD ≤ u /χD (c )) /θcD → 1 as c → 0+, then we

have the following convergence

χD (c ) TVc (X , ·) ⇒ 2 · Id .

Rafał M. Łochowski

Truncated variation

Osaka 2015

38 / 51

Consequence of Theorem M1 and Theorem SsP

Corollary (S)

Let Xt , t ≥ 0, be a self-similar càdlàg process as in Theorem SsP and

f : R → R be a continuous function, then

ˆ

ˆ

c

1/β−1

nca (X , ·)f

(a) da → C

·

f (Xt − ) dt ,

0

R

where the constant C is the same as in Theorem SsP.

Rafał M. Łochowski

Truncated variation

Osaka 2015

39 / 51

Consequence of Theorem M2 and Theorems LP1,

LP2

Corollary (L)

Let Xt , t ≥ 0, be a Lévy process as in Theorem L1. If the assumptions

of Theorem L1 are satisfied then

ˆ

ˆ

nca (X , ·)f

χU (c )

·

(a) da ⇒ 2

f (Xt − ) dt .

0

R

An analogous convergence, namely

ˆ

ˆ

nca (X , ·)f

χD (c )

(a) da ⇒ 2

·

f (Xt − ) dt ,

0

R

holds when the assumptions of Theorem L2 are satisfied.

Rafał M. Łochowski

Truncated variation

Osaka 2015

40 / 51

More specific case - spectrally assymetric

processes with ”almost” α-stable jumps

Theorem

Let Xt , t ≥ 0, be a Lévy process without Brownian component, with the

Lévy measure Π such that

Π(dx ) =

L(x )

(−x )1+α

1x <0 dx

for α ∈ (1; 2) and some Borel-measurable function

α(α−1)

α−1

L : (−∞; 0) → (0; +∞) , slowly varying at 0. Then χD (c ) ∼ Γ(2−α) Lc(−c )

and

α (α − 1) c α−1

TVc (X , ·) ⇒ 2 · Id .

Γ (2 − α) L (−c )

Rafał M. Łochowski

Truncated variation

Osaka 2015

41 / 51

A remark on local times

The most common definition of the local times L = Lat , a ∈ R, t ≥ 0, of a

given process Xt , t ≥ 0, is as the Radon-Nikodym derivative of the

occupation measure of X with respect to the Lebesgue measure in R;

for every Borel measurable function f : R → R and t > 0,

ˆ

ˆ

t

f (a) Lat da.

f (Xs ) ds =

0

Rafał M. Łochowski

R

Truncated variation

Osaka 2015

42 / 51

A remark on local times

The most common definition of the local times L = Lat , a ∈ R, t ≥ 0, of a

given process Xt , t ≥ 0, is as the Radon-Nikodym derivative of the

occupation measure of X with respect to the Lebesgue measure in R;

for every Borel measurable function f : R → R and t > 0,

ˆ

ˆ

t

f (a) Lat da.

f (Xs ) ds =

0

R

Notice that for any càdlàg process Xt , t ≥ 0, and continuous f

ˆ

ˆ

·

·

f (Xt − ) dt =

0

f (Xt ) dt .

0

Thus, in view of Corollary S and Corollary L we have that the natural

candidates for the local times Lat for a self-similar or a Lévy process X

are the limits (if they exist)

1

1

χU (c ) nca (X , t ) or

χD (c ) nca (X , t ).

C −1 c 1/β−1 nca (X , t ),

2

2

Rafał M. Łochowski

Truncated variation

Osaka 2015

42 / 51

Second order convergence of the truncated

variation of strictly α-stable processes

Let Xt , t ≥ 0, be strictly α-stable process with the characteristic

exponent

ΨX (θ) = C0 |θ|α 1 − i γ tan

πα

2

sgnθ ,

(12)

where α ∈ (1; 2) is the index, C0 > 0 is the scale parameter and

γ ∈ [−1; 1] is the skewness parameter. Define

A := lim E TV1 (X , [0; N + 1]) − TV1 (X , [0; N ]) .

N →+∞

(it is possible to prove that this limit exists) and

Ttc := TVc (X , [0, t ]) − c 1−α A · t .

Rafał M. Łochowski

Truncated variation

Osaka 2015

43 / 51

Second order convergence of the truncated

variation of strictly α-stable processes, cont.

Theorem (SecondOrder)

Let α ∈ (1; 2) and Xt , t ≥ 0, be strictly α-stable process with the

characteristic exponent given by formula (12), then

T c =⇒ L1 + L2 ,

where L1 and L2 are two independent, spectrally positive processes

such that X = L1 − L2 and L1 + L2 is strictly α-stable, spectrally positive

process with the characteristic exponent given by formula

α

ΨL1 +L2 (θ) = C0 |θ|

Rafał M. Łochowski

1 − i tan

Truncated variation

πα

2

sgnθ .

Osaka 2015

44 / 51

Second order convergence of the truncated

variation of strictly 1-stable processes

Let Xt , t ≥ 0, be strictly 1-stable process with the characteristic

exponent

ΨX (θ) = C0 |θ| + i ηθ,

(13)

with the scale parameter C0 > 0 and the drift η ∈ R. (The characterisitc

exponent of a strictly 1-stable process is necessarily of this form.) Let

us set

B = lim E TV1 (X , [0; N + 1]) − TV1 (X , [0; N ]) − TV (Y , [0; N ]) ,

N →+∞

where Y = ∑N <s≤N +1 |Xs − Xs− | 1|Xs −Xs− |≥1 and

2

Ttc := TVc (X , [0, t ]) − C0 log c −1 · t − B · t .

π

Rafał M. Łochowski

Truncated variation

Osaka 2015

45 / 51

Second order convergence of the truncated

variation of strictly 1-stable processes, cont.

Theorem (SecondOrder1)

Let Xt , t ≥ 0, be strictly 1-stable process with the characteristic

exponent given by formula (13), then

T c =⇒ M 1 + M 2 ,

where M 1 , M 2 are two independent, spectrally positive processes such

that X = M 1 − M 2 and M 1 + M 2 is 1-stable process with the

characteristic exponent given by formula

2 ( 1 − C)

ΨM 1 +M 2 (θ) = C0 |θ| 1 + i sgn (θ) log |θ| − i

C0 θ,

π

π

2

where C = Γ0 (1) ≈ 0.577 is the Euler-Mascheroni constant.

Rafał M. Łochowski

Truncated variation

Osaka 2015

46 / 51

Second order convergences for numbers of

segment crossings

The immediate consequences of Theorem SecondOrder,

SecondOrder1 and equality (10) is the second order convergence for

the integrated numbers of segment crossings:

if X is strictly α-stable (α ∈ (1; 2)):

ˆ

nc (X , t ) dy − c 1−α A · t =⇒ L1 + L2

y

R

and if X is strictly 1-stable:

ˆ

R

Rafał M. Łochowski

2

y

nc (X , t ) dy − C0 log c −1 · t − B · t =⇒ M 1 + M 2 .

π

Truncated variation

Osaka 2015

47 / 51

Open questions

Naturally, the next step would be the investigation of the second order

convergence for the integrated numbers of segment crossings with

respect to the measure f (y )dy:

ˆ

y

nc (X , t ) f (y )dy .

R

Why it may be interesting?

Rafał M. Łochowski

Truncated variation

Osaka 2015

48 / 51

Open questions

Naturally, the next step would be the investigation of the second order

convergence for the integrated numbers of segment crossings with

respect to the measure f (y )dy:

ˆ

y

nc (X , t ) f (y )dy .

R

Why it may be interesting?

´

y

1

The integral R nc (X , t ) f (y )dy may reveal much stronger

y

concentration than nc (X , t ) for given y ∈ R.

2

Investigation

together with R nc (X , t ) f (y )dy integrals of the form

´ y

y

R dc (X , t ) f (y )dy , where dc (X , t ) is the number of

downcrossings of X from above the level y + c to the level y till

time t , may reveal interesting correction terms.

´

Rafał M. Łochowski

y

Truncated variation

Osaka 2015

48 / 51

Some references

[F2010] M. Fukasawa, Central limit theorem for the realized volatility

based on tick time sampling. Fin. Stoch. 14:209–233, 2010.

[Kasahara, 1980] Y. Kasahara. On Lévy’s downcrossing theorem. Proc.

Japan Acad. Ser. A Math. Sci., 56:455–458, 1980.

[LG2014] R. M. Łochowski and R. Ghomrasni. Integral and local limit

theorems for numbers of level crossings for diffusions and the Skorohod

problem. Electron. J. Probab. 19(10):1–33, 2014.

[LM2013] R. M. Łochowski and P. Miłoś. On truncated variation, upward

truncated variation and downward truncated variation for diffusions.

Stochastic Process. Appl. 123:446-474.

[LM2014] R. M. Łochowski and P. Miłoś. Limit theorems for the

truncated variation and for numbers of interval crossings of Lévy and

self-similar processes. preprint, available from the web page

www.akson.sgh.waw.pl\ ∼rlocho

Rafał M. Łochowski

Truncated variation

Osaka 2015

49 / 51

Some references, cont.

[L2014] R. M. Łochowski. On the existence of the Riemann-stieltjes

integral. Preprint arXiv:1403.5413, 2014.

[T1972] S. J. Taylor. Exact asymptotic estimates of Brownian path

variation. Duke Math. J., 39(2):219–241, 1972.

[Young, 1936] L. C. Young. An inequality of the Hölder type, connected

with Stieltjes integration. Acta Math., 67(1):251–282, 1936.

Rafał M. Łochowski

Truncated variation

Osaka 2015

50 / 51

Thank you!

Rafał M. Łochowski

Truncated variation

Osaka 2015

51 / 51