Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

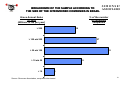

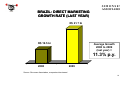

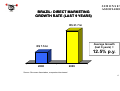

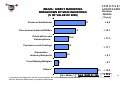

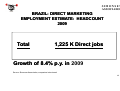

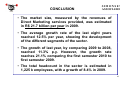

S IM O N S E N ASSOCIADOS ABEMD BRAZILIAN DIRECT MARKETING ASSOCIATION (ASSOCIAÇÃO BRASILEIRA DE MARKETING DIRETO) INDICATORS 2009 and FIRST SEMESTER 2010 1 S IM O N S E N ASSOCIADOS OUR THANKS TO CORREIOS FOR SUPPORTING THIS STUDY 2 S IM O N S E N ASSOCIADOS TECHNICAL ASSISTANCE 3 INDEX S IM O N S E N ASSOCIADOS Objective Methodology ABEMD Indicators 2009 Consolidated Growth: 1st Semester 2010 Conclusions 4 INDEX S IM O N S E N ASSOCIADOS Objective 5 OBJECTIVE S IM O N S E N ASSOCIADOS The objective of this study is to develop a current and updated basis of strategic information on the direct marketing sector, encompassing its main segments. The direct marketing study comprises the estimate of market size, equivalent to the revenue of services provided by its several segments. 6 INDEX S IM O N S E N ASSOCIADOS Methodology 7 METHODOLOGY S IM O N S E N ASSOCIADOS The information presented in this study resulted from analytical treatment of data and information obtained from primary and secondary sources: • Primary sources, represented by interviews carried out with direct marketing service companies, through their various segments, client companies, government agencies and trade associations, seeking to develop, based on these information, knowledge about the market of the direct marketing sector. • Secondary sources are represented by elements extracted from publications and reports of specific researches, found in several data sources and in the Data Bank of SIMONSEN ASSOCIADOS. 8 S IM O N S E N ASSOCIADOS CONSULTED COMPANIES UPDATE: STUDY ON 2009 AND 2010 • Direct Marketing Companies • Client/Customer Companies • Associations and Entities • 214 Total of Interviews 9 CONSULTED COMPANIES: NUMBER OF INTERVIEWS S IM O N S E N ASSOCIADOS • 2009 STUDY = 214 • 2008 STUDY = 102 • 2007 STUDY = 125 • 2006 STUDY = 183 10 S IM O N S E N ASSOCIADOS LOCATION OF CONSULTED COMPANIES 2009 % BY GEOGRAPHIC REGION South 17 Southeast 59 Northeast 13 Center West North 9 2 Source: Simonsen Associados, companies interviewed 11 BRAZIL: GEOGRAPHIC BREAKDOWN OF GDP 2008 ESTIMATE % BY GEOGRAPHIC REGION S IM O N S E N ASSOCIADOS 5 NORTH 14 NORTHEAST 7 CENTER WEST 55 SOUTHEAST 19 SOUTH Source: Central Bank , IBGE 12 S IM O N S E N BREAKDOWN OF THE SAMPLE ACCORDING TO ASSOCIADOS THE SIZE OF THE INTERVIEWED COMPANIES IN BRAZIL Gross Annual Sales in 2009 (Millions of R$ per year) % of the number of consulted companies > 200 16 > 100 até 200 27 > 50 até 100 33 > 10 até 50 < 10 19 5 Source: Simonsen Associados, companies interviewed 13 INDICE S IM O N S E N ASSOCIADOS ABEMD Indicators 2009 Growth in the First Semester of 2010 14 S IM O N S E N ASSOCIADOS BRAZIL: DIRECT MARKETING MARKET SIZE ESTIMATE ( REVENUE ) R$ 21.7 Bi 2009 Source: Simonsen Associados, companies interviewed 15 S IM O N S E N ASSOCIADOS BRAZIL: DIRECT MARKETING GROWTH RATE (LAST YEAR) R$ 21.7 bi R$ 19.5 bi Average Growth 2008 to 2009 (last year) = 11.3% p.y. 2008 2009 Source: Simonsen Associados, companies interviewed 16 S IM O N S E N ASSOCIADOS BRAZIL: DIRECT MARKETING GROWTH RATE (LAST 9 YEARS) R$ 21.7 bi Average Growth (last 9 years) = R$ 7.5 bi 12.5% p.y. 2000 2009 Source: Simonsen Associados, companies interviewed 17 S IM O N S E N ASSOCIADOS BRAZIL: DIRECT MARKETING MARKET SIZE GROWTH RATES Growth rate 2008 to 2009 (last year) = 11,3% p.y. Growth rate 2000 to 2009 (last 9 years) = 12,5% p.y. Growth rate 1st Semester 2010 compared to 1st Semester 2009 (first semester) = 21,1% p.y. Future trend according to the point of view of the interviewed companies 2010 to 2014 (next 5 years average) = Source: Simonsen Associados, companies interviewed 16,4% p.y. 18 BRAZIL: DIRECT MARKETING S IM O N S E N ASSOCIADOS BREAKDOWN BY MARKET SEGMENT REVENUE: 2009 ESTIMATE* Revenue (R$ mi) % of total Internet and E-commerce Services 24.9% 5,400 Call center/ Contact center/Telemarketing Companies 22.5% Distribution and Logistics 14.0% 3,040 Print Shops: Printings for Direct Marketing 13.9% 3,020 Technology applied to Direct Marketing 13.8% 3,000 Database and CRM Direct Marketing Agencies 1.8% Mailing Lists Suppliers 0.4% Others 2.4% 4,880 6.2% 1,350 400 90 520 Total M R$ 21,700 * Digital included in several of the segments Source: Simonsen Associados, companies interviewed 19 BRAZIL: DIRECT MARKETING BREAKDOWN BY MARKET SEGMENT AND ANNUAL INCREASE IN REVENUE: 2009 ESTIMATE* S IM O N S E N ASSOCIADOS % of total Revenue (M R$) 24.9% 5,400 Internet and E-commerce Services Variation 2008/07 (% p.y.) + 15.6 Call center/ Contact center/Telemarketing Companies 22.5% Distribution and Logistics 14.0% 3,040 + 10.1 Print Shops: Printings for Direct Marketing 13.9% 3,020 + 9.0 Technology applied to Direct Marketing 13.8% 3,000 + 8.7 Direct Marketing Agencies 1.8% Mailing Lists Suppliers 0.4% Others 2.4% + 11.1 400 90 + 12.5 520 + 15.6 M = Million Source: Simonsen Associados, companies interviewed + 8.4 + 17.4 6.2% 1,350 Database and CRM * Digital included in several of the segments 4,880 Total M R$ 21,700 + 11.3 20 S IM O N S E N ASSOCIADOS COMPARISON OF THE BRAZILIAN DIRECT MARKETING MARKET SIZE WITH GDP - 2009 GDP R$ 3,143.0 bi DIRECT MARKETING MARKET SIZE SHARE R$ 21.7 bi 0.69% * GDP 2008 = R$ 3,004.9 billion and Direct Marketing R$ 19.7 billion or 0.66% of share. Source: IBGE 21 S IM O N S E N ASSOCIADOS BRAZIL: DIRECT MARKETING BREAKDOWN BY MAIN INDUSTRIES (% OF VALUE OF 2009) Financial Institutions 22 Telecommunications/Utilities 15 Publications and Subscriptions 10,5 Commerce and Catalogs 10 Automotive Industry/Autoparts Fund Raising/Religion 8,5 3 Others* *: includes several segments, but the main segments are construbusiness and educational Source: Simonsen Associados, companies interviewed 31 22 S IM O N S E N ASSOCIADOS BRAZIL: DIRECT MARKETING BREAKDOWN BY MAIN INDUSTRIES (% OF VALUE OF 2009) Financial Institutions 22 Telecommunications/Utilities + 6,4 15 Publications and Subscriptions + 15,1 10,5 Commerce and Catalogs + 11,3 10 Automotive Industry/Autoparts Fund Raising/Religion Variation 2009/08 (% p.y.) + 17,1 8,5 + 5,1 3 - 4,7 Others* 31 M = Milhão Total M R$ 21.700 *: includes several segments, but the main segments are construbusiness and educational Source: Simonsen Associados, companies interviewed + 15,0 + 11,3 23 BRAZIL: DIRECT MARKETING BREAKDOWN BY TYPE OF BUSINESS 2009 S IM O N S E N ASSOCIADOS B2B 34% B2C 66% Total = R$ 21.7 billion 24 Source: Simonsen Associados, companies interviewed S IM O N S E N ASSOCIADOS BRAZIL: DIRECT MARKETING EMPLOYMENT ESTIMATE: HEADCOUNT 2009 Total 1,225 K Direct jobs Growth of 8.4% p.y. in 2009 Source: Simonsen Associados, companies interviewed 25 INDEX S IM O N S E N ASSOCIADOS Conclusion 26 CONCLUSION S IM O N S E N ASSOCIADOS • The market size, measured by the revenues of Direct Marketing services provided, was estimated in R$ 21.7 billion per year in 2009. • The average growth rate of the last eight years reached 12.5% per year, showing the development of the different segments of the sector. • The growth of last year, by comparing 2009 to 2008, reached 11.3% p.y. However, the growth rate reaches 21.1% comparing the first semester 2010 to first semester 2009. • The total headcount in the sector is estimated in 1,225 k employees, with a growth of 8.4% in 2009. 27 S IM O N S E N ASSOCIADOS WWW.ABEMD.ORG.BR WWW.SIMONSEN.COM.BR Indicadores ABEMD 28 S IM O N S E N ASSOCIADOS OUR THANKS TO CORREIOS FOR SUPPORTING THIS STUDY 29 S IM O N S E N ASSOCIADOS TECHNICAL ASSISTANCE 30