Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Gasoline and diesel usage and pricing wikipedia , lookup

Yield management wikipedia , lookup

Resource-based view wikipedia , lookup

Marketing strategy wikipedia , lookup

Revenue management wikipedia , lookup

Global marketing wikipedia , lookup

Service parts pricing wikipedia , lookup

Marketing channel wikipedia , lookup

First-mover advantage wikipedia , lookup

Product planning wikipedia , lookup

Dumping (pricing policy) wikipedia , lookup

Pricing strategies wikipedia , lookup

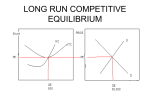

Chapter 11 Monopolistic Competition Lecture Plan • Introduction • • • • Features of Monopolistic Competition Identification of industry Demand and Marginal Revenue Curves of a Firm Price and Output Decisions in Short Run • Price and Output Decisions in Long Run • Monopolistic Competition and Advertising • Comparison between Monopolistic Competition, Monopoly and Perfect Competition Objectives • To understand the nature of imperfect competition or monopolistic competition. • To analyze the pricing and output decisions of a monopolistically competitive firm in the short run and long run. • To comprehend why a firm in monopolistic competition operates with excess capacity. • To understand the rationale behind advertising for the “unique” product of a monopolistically competitive firm. Introduction • Introduced by Joan Robinson (The Economics of Imperfect Competition, 1933) and Edward H. Chamberlin (The Theory of Monopolistic Competition, 1933) • It is a market situation in which a relatively large number of producers offer similar but not identical products. • A combination of perfect competition and monopoly. • Imperfect competition because a large number of sellers sell heterogeneous or differentiated products and buyers have preferences for specific sellers. • Monopolistic, because each of these sellers makes the product unique by some differentiation and has control over the small section of market, just like a monopolist. Features of Monopolistic Competition Chamberlin: “Monopolistic competition is a challenge to the traditional viewpoint of economics that competition and monopoly are alternatives…By contrast it is held that most economic situations are composites of both competition and monopoly.” Features: • Large number of buyers and sellers:.. • Heterogeneous products. – A differentiated product enjoys some degree of uniqueness in the mindset of customers, be it real, or imaginary. – Heterogeneous Products • • • • Selling costs. Independent decision making. Imperfect knowledge. Unrestricted entry and exit. Demand and Marginal Revenue Curves of a Firm Price, Revenu e O M R A R Quanti ty •Normal downward sloping demand curve (AR Curve) as all the firms in the industry sell close substitutes. •Demand is highly elastic and slope of demand curve is flatter •If a firm increases the price of its product slightly, it will lose some, but not all of its customers. •if it lowers the price slightly, it will gain some, but not all of the customers of its rivals. •MR curve lies below AR curve Price and Output Decisions in Short Run • Joan Robinson: Each firm has a monopoly over its product. – When product is differentiated, firm has some monopoly power. • Firms have limited discretion over price, due to the existence of consumer loyalty for specific brands. • Negative slope of the demand curve that is instrumental for chances of monopoly profits in the short run. • The reason for supernormal profit in short run, is supplying a product which is differentiated, or at least perceived to be different by the consumer. Price & Output Decisions in Short Run Firm maximizes profit where (i) MR=MC; (ii) MC cuts MR when MC is rising. Profit maximising output OQE and Price OPE Price, Revenu e, Cost M C PE B A E O QE M R Quanti ty A C A R Total revenue = OPEBQE Total cost =OAEQE Supernormal profit =APEBE since price OPE > OA (AR>AC) Price & Output Decisions in Short Run Firm maximizes profit where (i) MR=MC; (ii) MC cuts MR when MC is rising. Profit maximising output OQE and Price OPE Price, Revenu e, Cost A E PE B O QE M C M R Quanti ty A C A R Total revenue = OPEBQE Total cost =OAEQE Loss =APEBE since price OPE < OA (AR<AC) Price & Output Decisions in Long Run Firm maximizes profit where (i) MR=MC; (ii) MC cuts MR when MC is rising. Profit maximising output OQE and Price OPE Price, Revenu e, Cost PE O M C B QE M R Quanti ty A C A R Total revenue = OPEBQE Total cost =OAEQE Normal profit = No loss no gain since AR=AC Price & Output Decisions in Long Run •Just like perfect competition, in monopolistic competition too all the firms would earn normal profits in the long run. •In the long run supernormal profit would attract new firms to the industry till all the firms earn only normal profits. •Losses, will force firms to exit the industry till remaining firms in the market earn only normal profits. •If all the firms only normal profit there will be no tendency to enter or exit the market. Monopolistic Competition and Advertising Advantages • Since there are a large number of sellers, offering a unique brand, customers need to collect and process information on such large number of brands. • It is more profitable to attract customers through advertising rather than by lowering price. • Advertising induces customers to pay a premium for the particular brand, termed “brand equity” in marketing. • Advertising is to shift the demand curve of one particular firm, at the expense of other firms that are offering similar products. Monopolistic Competition and Advertising Criticism: • Advertising induces customers into spending more, because of the brand, rather than rational factors. • A wasteful expenditure that adds no value to the product • Leads to brand confusion in the minds of the consumers. • Advertisements of rival products may even cancel each other, leading to increase in average costs of each firm, without any corresponding increase of sales. Optimal Level of Advertising MR derived from advertising=MC of advertising MRA=MCA Comparison with Monopoly and Perfect Competition Firms are in equilibrium and earning normal profit AR=AC Price, Revenue, Cost PM PMC LAC EM EM C EC DC PC DM DMC O QM QMC QC Excess Capacity Quantity Perfect competition: horizontal demand curve (DC); output QC; price PC Monopolistic competition: downward sloping highly elastic demand curve (DMC); output QMC (< QC), at price PMC (> PC). Monopoly: downward sloping less elastic curve D M; output Q M (< QC and QMC), at price PM (> PC and PMC). Monopoly and monopolistically competitive firm operate at less than optimum output and charge a higher price. Excess capacity due to market imperfections= QC> Q MC >QM Summary • Most firms compete with each other and have some (if not full) degree of market power. Thus they lie somewhere between the two extremes of monopoly and perfect competition. • Joan Robinson of Cambridge and Chamberlin of Harvard independently came up with a new concept of market, which Robinson referred to as “imperfect competition” and Chamberlin termed as “monopolistic competition”. • A monopolistically competitive has features like large number of buyers and sellers, heterogeneous product, selling costs, independent decision making, imperfect knowledge, unrestricted entry and exit. • It is difficult to define an industry in case of monopolistic competition as firms sell differentiated products. Alternatively, we identify groups of differentiated products in this type of market, by clubbing close substitutes from the same industry and regard them as “product groups”. Summary • Firms under monopolistic competition have a normal demand curve with a negative slope because of substitution effect of heterogeneous products, which are close substitutes of each other. • They may generate supernormal profits or normal profits, or may even incur losses in the short run. • In the long run all firms earn normal profits due to the feature of unrestricted entry and exit. • It is profitable for to attract customers through advertising rather than by lowering the price. • A firm in perfect competition is able to efficiently allocate its resources by maximizing producer and consumer surplus, though a monopolist and a monopolistically competitive firm operate at less than optimum output, and charge a higher price.