Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

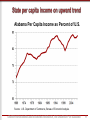

Federal Reserve Bank of Atlanta 2nd Annual LEARN Conference Atlanta, Georgia March 29, 2010 Samuel Addy, Ph.D. Center for Business and Economic Research Culverhouse College of Commerce The Alabama Business Confidence Index™ (ABCI) is a forward-looking quarterly measure of business sentiment across the state. The online survey is in its 9th year (34 consecutive quarters). The second quarter 2010 ABCI is up 0.7 points; a jump of 14 points in third quarter 2009 indicated a clear turnaround in confidence. With an index of 49.5, panelists feel economic conditions will be better in the second quarter. However, they do not think the state will yet see a broad-based recovery encompassing output, sales, profits, employment, and capital spending. Two of the six components, sales and profits, are above the expansion threshold of 50 this quarter. Hiring and capital spending are the weakest links in the recovery. CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 2 National Economy 47.0 Alabama Economy 49.8 Industry Sales 56.4 Industry Profits 50.5 Industry Hiring 47.3 Capital Expenditures 46.1 ABCI 49.5 Index above 50 indicates expansion. Index below 50 indicates contraction. increase from previous quarter decrease from previous quarter CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 3 CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 4 CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 5 CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 6 CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 7 CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 8 Many economic and workforce development successes with accolades for state agencies. A number of cities listed as best places to live and do business. Continued and faster than expected population growth; moving companies report sharp reductions nationwide but net gain for Alabama in 2009. Per capita income reached highest levels relative to the nation’s. Fast-growing tourism and exports industries. Continuing diversification of the state economy into biotechnology, healthcare, aerospace, automotive, national defense, education, steel, shipbuilding, and other high-paying manufacturing and white-collar jobs. CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 9 7/1/2009 Alabama 4,708,708 Anniston-Oxford 114,081 Auburn-Opelika 135,883 Birmingham-Hoover 1,131,070 Decatur 151,399 Dothan 142,693 Florence-Muscle Shoals 144,238 Gadsden 103,645 Huntsville 406,316 Mobile 411,721 Montgomery 366,401 Tuscaloosa 210,839 Non-metro (29.5%) 1,390,422 2008 to 2009 Number Percent Net Change Change Migration 31,244 659 2,778 7,924 1,055 1,247 412 210 9,088 2,589 805 1,937 2,540 0.7 0.6 2.1 0.7 0.7 0.9 0.3 0.2 2.3 0.6 0.2 0.9 0.2 16,363 497 1,993 3,975 571 822 435 254 7,077 691 -1,130 1,063 -19 Source: U.S. Census Bureau, Population Estimates Division. CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 10 Alabama Per Capita Income as Percent of U.S. Source: U.S. Department of Commerce, Bureau of Economic Analysis. CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 11 CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 12 Continuing, but slowing, job losses Declines in consumer spending and income Declining revenue to fund public education Long-term workforce development Cutbacks in federal government spending for some programs Continuing problems in commercial and residential real estate CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 13 The number of employed residents declined at a slower rate from the start of the recession until mid-2008, but has fallen sharply since; 288,441 have lost their jobs and many have become discouraged. After being below the national rate from 2002 through 2008, the state’s unemployment rate has been above the nation’s since February 2009. Most job losses were in manufacturing, construction, retail trade, and professional and business services; except for retail, these sectors pay high salaries and wages. Tax revenues have declined sharply. Unemployment Rate (%) Number Employed Change Percent Change Dec-07 3.9 2,100,370 Jun-08 5.3 2,060,097 -40,273 -1.9 Dec-08 7.0 1,995,929 -64,168 -3.1 Jun-09 10.8 1,916,297 -79,632 -4.0 Dec-09 10.6 1,837,542 -78,755 -4.1 Jan-10 11.8 1,811,929 -25,613 -1.4 Source: Alabama Department of Industrial Relations (non-seasonally adjusted). CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 14 Four main components – Output State Real Output in Sector i = F(The Corresponding U.S. Sector Output or Industrial Production, The Relative Sector Wage Rate, The Relative Tax Burden,…) – Employment State Wage and Salary Employment in Sector i = F(The Corresponding State Industrial Real Output, The Real Industry Wage Rate,…) – Wage rates State Wage Rate in Sector i = F(The Corresponding U.S. Sector Wage Rate, The State Unemployment Rate,…) – Income, includes personal income and its components and detailed wages and salaries by industry State Income category = F(The Corresponding U.S. Income Category,…) CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 15 2008 2009 2010 2011 0.4 -2.4 3.0 2.9 -0.2 -0.8 2.4 2.7 -22.9 -20.4 2.1 27.6 Business Fixed Investment 1.6 -17.7 1.7 7.3 Federal Government 7.7 5.2 3.7 -2.8 State & Local Government 0.5 -0.2 -0.4 0.2 Exports 5.4 -9.6 11.5 6.7 Imports -3.2 -14.2 -10.3 7.5 Payroll Employment (% growth) -0.6 -4.3 -0.7 1.6 Unemployment Rate 5.8 9.3 9.6 9.1 CPI Inflation 3.8 -0.3 1.8 1.8 13.2 10.4 11.8 13.8 (Percent change unless otherwise noted) Real GDP Consumption Residential Investment Light Vehicle Sales (Millions) Source: IHS Global Insight. CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 16 Annual Percent Change (2000 Chained Dollars) CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 17 The state’s economy will be recovering in 2010: – Alabama GDP – Alabama employment – Total tax collections Forecast 1.9 percent -0.1 percent 0.1 percent Range 1.0 to 2.5 percent -1.0 to 1.0 percent -1.5 to 1.5 percent Education and diversification must be priorities – Workforce and economic development funding challenges remain Focus on optimality, sustainability, equity, and flexibility – Public policy (education, infrastructure, health & safety, taxes, …) – Business and consumer behavior CENTER FOR BUSINESS AND ECONOMIC RESEARCH, THE UNIVERSITY OF ALABAMA 18