Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

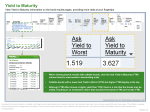

Australian Corporate Bond Price Tables Jul 13, 2017 a Corporate bonds offer an alternative to equity investment in providing a fixed “coupon”, or interest payment, unlike equities which pay (or not) non-fixed dividend payments, and a maturity date, unlike equities which are open-ended. en Listed corporate bonds can be traded just as listed shares can be traded. Bonds bought at issue and held to maturity do not offer capital appreciation as an equity can, but assuming no default do not offer downside capital risk either. Pricing is based on market perception of default risk, or “credit risk”, throughout the life of the bond. Bonds do offer capital risk/reward if traded on the secondary market within the bounds of issue and maturity. Coupon rates are fixed but bond prices fluctuate on perceived changes in credit risk and on changes in prevailing market interest rates. Note that the attached tables offer three “yield” figures for each issue, being “coupon”, “yield” and “running yield”. Ar If a bond is purchased at $100 face value and a 5% coupon, and face value is returned at maturity, the running yield is 5% and the yield, or “yield to maturity” is 5%. If a bond is purchased in the secondary market at greater than $100, the running yield, which is the per annum yield for each year the bond is held, is less than 5% because the coupon is paid on face value. The yield to maturity is also less than the coupon as more than $100 is paid to receive $100 back at maturity. FN If a bond is purchased in the secondary market at less than $100, the running yield, which is the per annum yield for each year the bond is held, is more than 5% because the coupon is paid on face value. The yield to maturity is also more than the coupon as less than $100 is paid to receive $100 back at maturity. Note that if a bond is trading on the secondary market at a price greater than face value the implication is the market believes the bond is less risky than at issue, and if at a lesser price it has become more risky. Bonds trading on yields substantially higher than their coupons thus do not offer a bargain per se, just a higher risk/reward investment. In all cases, bond supply and demand balances will also impact on secondary pricing. Note also that while most coupons are fixed, the attached table also provides prices for capital indexed bonds (CIB) and indexed annuity bonds (IAB). This service is provided for informative purposes only. It is not, and should not be treated as, a solicitation or recommendation to buy corporate bonds. Investors should always consult their financial adviser before acting on any information gleaned from this service. FNArena does not guarantee the accuracy of information provided. Note that while FNArena publishes this table weekly, prices are fluid and potentially changing throughout each trading day. Hence prices tabled may not potentially changing throughout each trading day. Hence prices tabled may not reflect actual market prices at the time of reading. FNArena disclaimer FN Ar en a Find out why FNArena subscribers like the service so much: "Your Feedback (Thank You)" - Warning this story contains unashamedly positive feedback on the service provided.