CPA PassMaster Questions–Auditing 4 Export Date: 10/30/08

... Choice "b" is incorrect. The use of prenumbered remittance advices is not effective in preventing theft of receipts by employees because it does not prevent employee access to cash receipts. Choice "c" is incorrect. While the performance of monthly bank reconciliations is a good control, it would no ...

... Choice "b" is incorrect. The use of prenumbered remittance advices is not effective in preventing theft of receipts by employees because it does not prevent employee access to cash receipts. Choice "c" is incorrect. While the performance of monthly bank reconciliations is a good control, it would no ...

FREE Sample Here

... Bloom’s: Remembering LEARNING OBJECTIVES: ACCT.WARD.16.01-01 - 01-01 ACCREDITING STANDARDS: ACCT.ACBSP.APC.02 - GAAP ACCT.AICPA.BB.03 - Legal ACCT.AICPA.FN.03 - MeasurementBUSPROG: Ethics 9. A business is an organization in which basic resources or inputs, like materials and labor, are assembled and ...

... Bloom’s: Remembering LEARNING OBJECTIVES: ACCT.WARD.16.01-01 - 01-01 ACCREDITING STANDARDS: ACCT.ACBSP.APC.02 - GAAP ACCT.AICPA.BB.03 - Legal ACCT.AICPA.FN.03 - MeasurementBUSPROG: Ethics 9. A business is an organization in which basic resources or inputs, like materials and labor, are assembled and ...

Does a Change in a Logo Affect the Value of the Brand? The Case

... move away from a main-street coffee shop and into a more modern espresso bar that offered a broader array of products. The company’s second major logo change occurred in 1992 when Starbucks had their initial public offering on the NASDAQ stock exchange.3 Finally, this thesis will examine the impacts ...

... move away from a main-street coffee shop and into a more modern espresso bar that offered a broader array of products. The company’s second major logo change occurred in 1992 when Starbucks had their initial public offering on the NASDAQ stock exchange.3 Finally, this thesis will examine the impacts ...

Defence Audit Guidelines_Final 25 March 2010

... DAGP prepared guidelines pertaining to different sectors and departments. Some of these guidelines are specific to an office (e.g. DG, Works), while the others are applicable across the board (Environment). These Guidelines were circulated among the FAOs for use. However, they were not found helpful ...

... DAGP prepared guidelines pertaining to different sectors and departments. Some of these guidelines are specific to an office (e.g. DG, Works), while the others are applicable across the board (Environment). These Guidelines were circulated among the FAOs for use. However, they were not found helpful ...

important notice this offering is available only to investors

... shown on, and transfers thereof will be effected only through, records maintained by Euroclear and Clearstream and their participants. It is expected that delivery of the beneficial interests in the Notes will be made through Euroclear and Clearstream, in each case on or about May 27, 2015 or such l ...

... shown on, and transfers thereof will be effected only through, records maintained by Euroclear and Clearstream and their participants. It is expected that delivery of the beneficial interests in the Notes will be made through Euroclear and Clearstream, in each case on or about May 27, 2015 or such l ...

Chapter Accounting for Leases - McGraw Hill Higher Education

... At this point it needs to be emphasised that the following discussion relates to the accounting requirements in place at the time of writing this chapter. That is, we will be discussing the accounting requirements incorporated within IAS 17. There is much discussion about the accounting for leases a ...

... At this point it needs to be emphasised that the following discussion relates to the accounting requirements in place at the time of writing this chapter. That is, we will be discussing the accounting requirements incorporated within IAS 17. There is much discussion about the accounting for leases a ...

Financial Accounting Chapter 2

... 2.1-30 Which of the following accounts are a standard component of stockholders’ equity? A) Prepaid Expenses B) Dividends C) Additional Paid In Stock D) Unearned Income Answer: B LO: 2-1 Diff: 2 EOC REF: P2-61 AACSB: Analytical skills AICPA Functional Competencies: Measurement AICPA Business Perspe ...

... 2.1-30 Which of the following accounts are a standard component of stockholders’ equity? A) Prepaid Expenses B) Dividends C) Additional Paid In Stock D) Unearned Income Answer: B LO: 2-1 Diff: 2 EOC REF: P2-61 AACSB: Analytical skills AICPA Functional Competencies: Measurement AICPA Business Perspe ...

OPEN JOINT STOCK CO LONG DISTANCE

... This communication does not constitute an offer to purchase, sell, or exchange or the solicitation of an offer to sell, purchase, or exchange any securities of OJSC “Rostelecom”, OJSC “N. W. Telecom”, OJSC “CenterTelecom”, OJSC “UTK”, OJSC “VolgaTelecom”, OJSC “Uralsvyazinform”, OJSC “SibirTelecom”, ...

... This communication does not constitute an offer to purchase, sell, or exchange or the solicitation of an offer to sell, purchase, or exchange any securities of OJSC “Rostelecom”, OJSC “N. W. Telecom”, OJSC “CenterTelecom”, OJSC “UTK”, OJSC “VolgaTelecom”, OJSC “Uralsvyazinform”, OJSC “SibirTelecom”, ...

As filed with the Securities and Exchange Commission on July 20

... rely on any unauthorized information or representations. This prospectus is an offer to sell only the ADSs offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information in this prospectus is current only as of the date of this prospectus. In connectio ...

... rely on any unauthorized information or representations. This prospectus is an offer to sell only the ADSs offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information in this prospectus is current only as of the date of this prospectus. In connectio ...

chapter 2

... 7. Prepare a trial balance and explain its purposes. A trial balance is a list of accounts and their balances at a given time. Its primary purpose is to prove the equality of debits and credits after posting. A trial balance also uncovers errors in journalizing and posting and is useful in preparing ...

... 7. Prepare a trial balance and explain its purposes. A trial balance is a list of accounts and their balances at a given time. Its primary purpose is to prove the equality of debits and credits after posting. A trial balance also uncovers errors in journalizing and posting and is useful in preparing ...

Aon plc (Form: 10-K, Received: 02/22/2013 16:07:43)

... and from insurers. These funds held on behalf of clients are generally invested in interest-bearing premium trust accounts and can fluctuate significantly depending on when we collect cash from our clients and when premiums are remitted to the insurance carriers. We earn interest on these accounts; ...

... and from insurers. These funds held on behalf of clients are generally invested in interest-bearing premium trust accounts and can fluctuate significantly depending on when we collect cash from our clients and when premiums are remitted to the insurance carriers. We earn interest on these accounts; ...

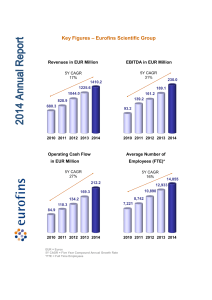

Consolidated Profit and Loss Statement

... fundamental drivers of the industry, and in particular of Eurofins, are plain to see and understand. ...

... fundamental drivers of the industry, and in particular of Eurofins, are plain to see and understand. ...

BROADCOM CORP (Form: 425, Received: 05/29/2015 09:04:49)

... and outstanding share of Class A common stock of the Company, $0.0001 par value (a “ Class A Common Share ”) and each issued and outstanding share of Class B common stock of the Company, $0.0001 par value (a “ Class B Common Share ”, and together with the Class A Common Shares, the “ Company Common ...

... and outstanding share of Class A common stock of the Company, $0.0001 par value (a “ Class A Common Share ”) and each issued and outstanding share of Class B common stock of the Company, $0.0001 par value (a “ Class B Common Share ”, and together with the Class A Common Shares, the “ Company Common ...

FREE Sample Here

... Download the full file instantly at http://testbankinstant.com 7. Which of the following is NOT a characteristic of a cdorporation? a. Corporations are organized as a separate legal taxable entity. b. Ownership is divided into shares of stock. c. Corporations experience an ease in obtaining large a ...

... Download the full file instantly at http://testbankinstant.com 7. Which of the following is NOT a characteristic of a cdorporation? a. Corporations are organized as a separate legal taxable entity. b. Ownership is divided into shares of stock. c. Corporations experience an ease in obtaining large a ...

THE BIG TENT Corporate Volunteering in the Global Age

... When analysing what a company should do in order to set up a quality corporate volunteering programme Kenn Allen suggests it is much more adequate to talk about “inspiring practices” than of “good practices.” Not all formulas work for all companies and it is up to each company to figure out what wor ...

... When analysing what a company should do in order to set up a quality corporate volunteering programme Kenn Allen suggests it is much more adequate to talk about “inspiring practices” than of “good practices.” Not all formulas work for all companies and it is up to each company to figure out what wor ...

A literature review on the evolving framework of bitcoin and its

... the parties to the transactions don’t have to share private data such as name or location22. However, all transactions are kept in the block chain, and so if a private key were compromised, it would be possible to identify them23. An unclear regulatory environment is a current concern for bitcoin. D ...

... the parties to the transactions don’t have to share private data such as name or location22. However, all transactions are kept in the block chain, and so if a private key were compromised, it would be possible to identify them23. An unclear regulatory environment is a current concern for bitcoin. D ...

Cash Operations Manual *UPDATED*

... the deposit equals the amount shown on the form and that an accurate account number is provided for posting to the General Ledger. The Cashier is performing a control designed to prevent mistakes from entering the University’s accounting system. To detect any mistakes that get through this process, ...

... the deposit equals the amount shown on the form and that an accurate account number is provided for posting to the General Ledger. The Cashier is performing a control designed to prevent mistakes from entering the University’s accounting system. To detect any mistakes that get through this process, ...

FREE Sample Here

... Full file at http://testbankwizard.eu/Test-Bank-for-Accounting-25th-Edition-by-Warren ...

... Full file at http://testbankwizard.eu/Test-Bank-for-Accounting-25th-Edition-by-Warren ...

CAPELLA EDUCATION CO (Form: S-1/A, Received

... We are committed to providing our learners with a high quality educational experience. We offer a broad array of curricula that incorporates competency-based instruction into a format specifically designed for online learning. Our faculty members bring significant academic credentials as well as tea ...

... We are committed to providing our learners with a high quality educational experience. We offer a broad array of curricula that incorporates competency-based instruction into a format specifically designed for online learning. Our faculty members bring significant academic credentials as well as tea ...

MYLAN INC. (Form: 10-K, Received: 02/27/2014 16

... On December 4, 2013 , we acquired the Agila Specialties business (‘‘ Agila ’’), a developer, manufacturer and marketer of high-quality generic injectable products, from Strides Arcolab Limited (‘‘ Strides Arcolab ’’) for approximately $1.4 billion , which includes contingent consideration estimated ...

... On December 4, 2013 , we acquired the Agila Specialties business (‘‘ Agila ’’), a developer, manufacturer and marketer of high-quality generic injectable products, from Strides Arcolab Limited (‘‘ Strides Arcolab ’’) for approximately $1.4 billion , which includes contingent consideration estimated ...

Earnings Quality and Stock Returns

... stock price reaction. Our analysis of the predictive power of accruals for stock returns confronts these hypotheses—earnings manipulation, extrapolative biases concerning future growth, or underreaction to business conditions. We distinguish between these explanations along the following dimensions. ...

... stock price reaction. Our analysis of the predictive power of accruals for stock returns confronts these hypotheses—earnings manipulation, extrapolative biases concerning future growth, or underreaction to business conditions. We distinguish between these explanations along the following dimensions. ...

threadneedle investment funds icvc - Columbia Threadneedle Investments

... Underwriting commission is recognised when the issue takes place, except where the fund is required to take up all or some of the shares underwritten, in which case an appropriate proportion of the commission is deducted from the cost of those shares. Underwriting commission is treated as revenu ...

... Underwriting commission is recognised when the issue takes place, except where the fund is required to take up all or some of the shares underwritten, in which case an appropriate proportion of the commission is deducted from the cost of those shares. Underwriting commission is treated as revenu ...

everett spinco, inc.

... This Registration Statement on Form 10 (the “Form 10”) incorporates by reference information contained in (a) the proxy statement/prospectus-information statement of Computer Sciences Corporation filed herewith as Exhibit 99.1, referred to herein as the proxy statement/prospectus-information stateme ...

... This Registration Statement on Form 10 (the “Form 10”) incorporates by reference information contained in (a) the proxy statement/prospectus-information statement of Computer Sciences Corporation filed herewith as Exhibit 99.1, referred to herein as the proxy statement/prospectus-information stateme ...

Joint Statement of the Management Board (Vorstand) and the

... (Wertpapiererwerbs- und Übernahmegesetzes - "WpÜG") ("Offer Document") concerning the voluntary public takeover bid to the shareholders of GfK SE, a company having its seat in Nürnberg, Germany, registered in the commercial register of the local court of Nürnberg under registration number HRB 25014, ...

... (Wertpapiererwerbs- und Übernahmegesetzes - "WpÜG") ("Offer Document") concerning the voluntary public takeover bid to the shareholders of GfK SE, a company having its seat in Nürnberg, Germany, registered in the commercial register of the local court of Nürnberg under registration number HRB 25014, ...

CHAPTER 7 Cash and Receivables

... Allowance for Doubtful Accounts is credited with a percentage of the current year’s credit or total sales. The rate is determined by reference to the relationship between prior years’ credit or total sales and actual bad debts arising therefrom. Consideration should also be given to changes in credi ...

... Allowance for Doubtful Accounts is credited with a percentage of the current year’s credit or total sales. The rate is determined by reference to the relationship between prior years’ credit or total sales and actual bad debts arising therefrom. Consideration should also be given to changes in credi ...