Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

ISLAMIC MODES OF FINANCE

by

SIBGHATULLAH AHSAN

http://www.LearnIslamicFinance.com

ISLAMIC FINANCIAL SYSTEM- AN

INTRODUCTION

zBased on QURAN and SUNNAH

zDemands socio economic justice

zProhibits all kinds of RIBA

zProhibits all forms of exploitation

zProvides equal opportunities to all

zCondemns accumulation of wealth in few

hands

zEncourages acts of benevolence

http://www.LearnIslamicFinance.com

PRINCIPLES OF ISLAMIC FINANCE

zProhibition of RIBA

zAlkharajo bil dhaman (entitlement to profit

is associated with corresponding risk)

zProhibition of sale of goods before

acquiring ownership

zProhibition of sale of food stuff before

possession

zProhibition of debt for debt

zAvoidance of Gharar (uncertainty)

http://www.LearnIslamicFinance.com

PROHIBITION OF RIBA

z QURAN

{“ALLAH has permitted BAI’ (sale) and prohibited RIBA”

(Al Baqarah: 275)

{O you believers, fear ALLAH and give up whatever is

left in lieu of RIBA if you are indeed believer, Watch

out! If you do not obey this order (and give up all

outstanding RIBA), then there is a declaration of war

against you from ALLAH

and HIS PROPHET.

However, if you repent you have entitlement only to

your principals. Neither you inflict zulm on others, nor

the others should do zulm on you. (Al Baqarah: 278-9)

http://www.LearnIslamicFinance.com

PROHIBITION OF RIBA

z SUNNAH

Obadah ibn Samit directly reports from the

Prophet as saying: “Buy and sell gold for gold,

silver for silver, dates for dates, wheat for

wheat, salt for salt, and barley for barley on

the like for like basis. Whosoever gave more or

took more, verily he made a RIBA deal.

However, trade gold for silver as you wish

subject to the condition that the exchange be

hand to hand (spot). Trade wheat for dates or

barley for dates also likewise.

http://www.LearnIslamicFinance.com

EXCHANGE OF HOMOGENEOUS COMMODITIES OR

CURRENCIES

DELIVERY: Must be

simultaneous / spot

Commodity A

Commodity B

MEASURMENT: Must be

same in amount / weight /

count

http://www.LearnIslamicFinance.com

EXCHANGE OF HETEROGENEOUS

COMMODITIES OR CURRENCIES

DELIVERY: Must be

simultaneous / spot

Commodity B

Commodity A

MEASUREMENT: May be

different

http://www.LearnIslamicFinance.com

EXCHANGE INVOLVING RIBA IN HOMOGENEOUS

COMMODITIES OR CURRENCIES

DELIVERY: Any one

of the counter values

is delayed

Commodity A

Commodity B

MEASURMENT: Counter

values are not equal

http://www.LearnIslamicFinance.com

EXCHANGE INVOLVING RIBA IN HETEROGENEOUS

COMMODITIES OR CURRENCIES

DELIVERY: Delay in any of

the counter values would

amount to RIBA (Delivery

must be simultaneous /

spot

Commodity B

Commodity A

MEASUREMENT: May be

different

http://www.LearnIslamicFinance.com

Some principles derived from the

Hadith

zGeneral principles

{In a contract of sale counter values must be

exchanged simultaneously

{Quantity /number/measure etc. should be same

zExceptions

{Credit Sale

{Salam

{Qard-e-Hasanah

http://www.LearnIslamicFinance.com

WHAT IS RIBA

zSimple definition

{Any delay or discrimination (regarding

weight, measure or count) in any of the

counter values in a contract of exchange

is riba

{Any addition without a counter value is

RIBA

{Every loan entailing an increase is RIBA

http://www.LearnIslamicFinance.com

ISLAMIC CONTRACTS FOR

COMMERCIAL TRANSACTIONS

zMusharaka (Profit and Loss sharing)

zModaraba (Profit sharing)

zMusawamah (Bargaining sale)

zIjarah (Leasing)

zSalam (Advance payment sale)

zIstisna’ (Contract of manufacturing)

zMurabaha (Cost plus margin sale)

http://www.LearnIslamicFinance.com

MUSHARAKA

zCharacteristics

{All parties share in the capital

{All parties share profits as well as losses

{Profits are distributed as per agreed ratio

{Loss is borne by the parties as per capital

ratio

{Every partner is agent of other

http://www.LearnIslamicFinance.com

MUSHARAKA

PROFIT

Rs. 100

Rs. 60

Rs.1000

PARTNER A

Rs. 40

Rs.1000

VENTURE

Rs. 50

Must be according to

capital ratio

May be in any

agreed ratio

PARTNER B

Rs. 50

LOSS

Rs.100

http://www.LearnIslamicFinance.com

MUSHARAKA

PROFIT

Rs. 100

Rs. 50

Rs.2000

PARTNER A

Rs. 50

Rs.3000

VENTURE

Rs. 40

Must be according to

capital ratio

May be in any

agreed ratio

PARTNER B

Rs. 60

LOSS

Rs.100

http://www.LearnIslamicFinance.com

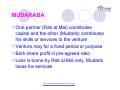

MUDARABA

zOne partner (Rab al Mal) contributes

capital and the other (Mudarib) contributes

his skills or services to the venture

zVenture may for a fixed period or purpose

zBoth share profit in pre-agreed ratio

zLoss is borne by Rab al Mal only, Mudarib

loses his services

http://www.LearnIslamicFinance.com

MUDARABA

PROFIT

50 %

50 %

SERVICES

RABBUL MAL

CAPITAL

VENTURE

ALL MONETORY LOSS

MUDARIB

LOSS OF SERVICES

LOSS

http://www.LearnIslamicFinance.com

MUDARABA

PROFIT

60 %

40 %

SERVICES

RABBUL MAL

CAPITAL

VENTURE

ALL MONETORY LOSS

MUDARIB

LOSS OF SERVICES

LOSS

http://www.LearnIslamicFinance.com

IJARAH

zUsufruct of an asset is passed to other

party against a periodic rent payment

zThe asset must have corpus (body) and

be in existence

zThe asset must not be consumable in

nature (should not vanish if used)

zOwnership will remain with the lessor and

he will bear all the risks related to

ownership

http://www.LearnIslamicFinance.com

IJARAH

Use/ usufruct Only

Ownership

LESSOR

Asset

Usufruct

Usufruct

Usufruct

Periodical payments/Rent

http://www.LearnIslamicFinance.com

LESSEE

SALAM (Advance payment)

zIt is an exception to the general

principle of instant exchange of

counter values in a contract of sale

http://www.LearnIslamicFinance.com

SALAM (Advance payment)

zFull payment of purchase price, No

deferment or installment in advance

money allowed

zNo loan adjustment is allowed

zQuality and quantity must be specified

zDate of delivery must be specified

http://www.LearnIslamicFinance.com

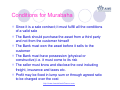

MURABAHA

z Murabaha is sale of a commodity at cost plus

margin; it must fulfill all the conditions of a valid

sale

z It may be spot sale or a deferred/credit sale

z Deferred sale Murabaha is used as financing

mode by Islamic Banks

z Deferred price becomes a debt and shall be

dealt with as a loan transaction

z Price once settled at the time of sale can not be

changed due to default of creditor, any thing

above sale price would be RIBA

http://www.LearnIslamicFinance.com

Conditions for Murabaha

z Since it is a sale contract; it must fulfill all the conditions

of a valid sale

z The Bank should purchase the asset from a third party

and not from the customer himself

z The Bank must own the asset before it sells to the

customer

z The Bank must have possession (physical or

constructive) i.e. it must come to its risk

z The seller must know and disclose the cost including

freight, insurance and taxes etc.

z Profit may be fixed in lump sum or through agreed ratio

to be charged over the cost

http://www.LearnIslamicFinance.com

MURABAHA

MURABAHA

CLASSICAL / SPOT

DEFERRED

with LUMP SUM

PAYMENT

http://www.LearnIslamicFinance.com

DEFERRED

with INSTALLMENT

PAYMENT

CLASSICAL MURABAHA

COST +MARGIN

IMMIDIATE DELIVERY

PRICE

SELLER

BUYER

GOOD

IMMIDIATE DELIVERY

http://www.LearnIslamicFinance.com

BAI’ MU’JJAL (deferred sale)

DEFERRED PAYMENT

PRICE

SELLER

BUYER

GOODS

IMMIDIATE DELIVERY

http://www.LearnIslamicFinance.com

MURABAHA WITH

DEFERRED PAYMENT

COST + MARGIN

DELAYED PAYMENT

PRICE

SELLER

BUYER

GOOD

IMMIDIATE DELIVERY

http://www.LearnIslamicFinance.com