Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

United States housing bubble wikipedia , lookup

Financialization wikipedia , lookup

Money supply wikipedia , lookup

History of the Federal Reserve System wikipedia , lookup

Global saving glut wikipedia , lookup

Interbank lending market wikipedia , lookup

Monetary policy wikipedia , lookup

Interest rate ceiling wikipedia , lookup

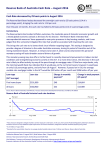

Economics | April 4 2017 Reserve Bank softens its views on the economy Reserve Bank Board meeting The Reserve Bank has left the cash rate at a record low of 1.50 per cent for the eighth straight month. The Reserve Bank has maintained its “neutral stance” – meaning rate hikes are as likely as rate cuts in the period ahead. What does it all mean? The Australian economy is very much a Curate’s egg at present – it is good in parts. Manufacturing is doing well and business conditions generally are favourable. But consumers are more cautious. Retail spending is soft while job markets are mixed, as are housing markets. So as you would expect the Reserve Bank is a little more considered when discussing the position of the Australian economy. But the Reserve Bank is by no means downcast, rather it is probably a little disappointed that the economy is largely marking time. The Reserve Bank sets policy by looking at where inflation is going to go. Inflation is still tipped to move above 2 per cent so clearly the Bank won’t be cutting rates any time soon. Housing has dominated the commentary. The Reserve Bank has added its voice to the need for lenders to be careful in assessing the serviceability of loans. And the Bank believes it would be positive if there was less reliance on interest only loans for home purchase. Perspectives on interest rates The Reserve Bank has left the cash rate at 1.50 per cent. The previous move was a rate cut in August 2016 (25 basis points). There have now been 12 rate cuts since November 2011, with the Reserve Bank cutting rates from 4.75 per cent to 1.50 per cent. The Reserve Bank had previously lifted rates seven times from October 2009 to November 2010 – a total of 1.75 percentage points, from 3.00 per cent to 4.75 per cent. What are the implications of today’s decision? The next move in interest rates is still more likely to be a rate hike than a rate cut. But in our view, policy is unlikely to change over 2017, so any rate hike is some way off. The Reserve Bank believes inflation will push into the 2-3 per cent target band. And economic growth is expected to lift over the year. Add in the fact that home prices are recording solid gains in many capital cities and it seems clear that rate cuts are off the agenda. Then there is the global environment. Global economic growth has improved and deflationary risks have receded. The US is lifting interest rates. And there are early signs that the Euro zone will reduce stimulus later this year. So the global environment supports the domestic policy leaning. The Reserve Bank is expected to maintain its neutral Craig James, Chief Economist (Author) Twitter: @CommSec Produced by Commonwealth Research based on information available at the time of publishing. We believe that the information in this report is correct and any opinions, conclusions or recommendations are reasonably held or made as at the time of its compilation, but no warranty is made as to accuracy, reliability or completeness. To the extent permitted by law, neither Commonwealth Bank of Australia ABN 48 123 123 124 nor any of its subsidiaries accept liability to any person for loss or damage arising from the use of this report. The report has been prepared without taking account of the objectives, financial situation or needs of any particular individual. For this reason, any individual should, before acting on the information in this report, consider the appropriateness of the information, having regard to the individual’s objectives, financial situation and needs and, if necessary, seek appropriate professional advice. In the case of certain securities Commonwealth Bank of Australia is or may be the only market maker. This report is approved and distributed in Australia by Commonwealth Securities Limited ABN 60 067 254 399 a wholly owned but not guaranteed subsidiary of Commonwealth Bank of Australia. This report is approved and distributed in the UK by Commonwealth Bank of Australia incorporated in Australia with limited liability. Registered in England No. BR250 and regulated in the UK by the Financial Conduct Authority (FCA). This report does not purport to be a complete statement or summary. For the purpose of the FCA rules, this report and related services are not intended for private customers and are not available to them. Commonwealth Bank of Australia and its subsidiaries have effected or may effect transactions for their own account in any investments or related investments referred to in this report. Economic Insights: Reserve Bank softens its views on the economy policy stance for now. Inflation is still low, economic indicators are more mixed and the higher Australian dollar is acting as a modest cap on economic growth. The Reserve Bank will especially watch the following in coming months: the upcoming French presidential election; US fiscal policy (the flagged tax cuts); Chinese economic activity; commodity markets; Australian home prices; inflation expectations; and the local job market. We expect the Reserve Bank to stay on the interest rate sidelines for the 2017 year. Comparing the two most recent statements The statement from the March 2017 meeting is on the left; the statement from today’s April 2017 meeting is on the right. Emphasis has been added to significant changes in the wording in the statements. Media Release Media Release No: 2017-06 Date: 7 March 2017 Embargo: For Immediate Release No: 2017-07 Date: 4 April 2017 Embargo: For Immediate Release Statement by Philip Lowe, Governor: Monetary Policy Decision At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent. Conditions in the global economy have continued to improve over recent months. Business and consumer confidence have both picked up. Abovetrend growth is expected in a number of advanced economies, although uncertainties remain. In China, growth is being supported by higher spending on infrastructure and property construction. This composition of growth and the rapid increase in borrowing mean that the medium-term risks to Chinese growth remain. The improvement in the global economy has contributed to higher commodity prices, which are providing a significant boost to Australia's national income. Headline inflation rates have moved higher in most countries, partly reflecting the higher commodity prices. Long-term bond yields are higher than last year, although in a historical context they remain low. Interest rates are expected to increase further in the United States and there is no longer an expectation of additional monetary easing in other major economies. Financial markets have been functioning effectively and stock markets have mostly risen. The Australian economy is continuing its transition following the end of the mining investment boom, expanding by around 2½ per cent in 2016. Exports have risen strongly and non-mining business investment has risen over the past year. Most measures of business and consumer confidence are at, or above, average. Consumption growth was stronger towards the end of the year, although growth in household income remains low. The outlook continues to be supported by the low level of interest rates. Financial institutions remain in a good position to lend. The depreciation of the exchange rate since 2013 has also assisted the economy in its transition following the mining investment boom. An appreciating exchange rate would complicate this adjustment. Labour market indicators continue to be mixed and there is considerable variation in employment outcomes across the country. The unemployment rate has been steady at around 5¾ per cent over the past year, with employment growth concentrated in part-time jobs. The forward-looking indicators point to continued expansion in employment over the period ahead. Inflation remains quite low. With growth in labour costs remaining subdued, underlying inflation is likely to stay low for some time. Headline inflation is expected to pick up over the course of 2017 to be above 2 per cent, with the rise in underlying inflation expected to be a bit more gradual. Conditions in the housing market vary considerably around the country. In some markets, conditions are strong and prices are rising briskly. In other markets, prices are declining. In the eastern capital cities, a considerable additional supply of apartments is scheduled to come on stream over the next couple of years. Growth in rents is the slowest for two decades. Borrowing for housing by investors has picked up over recent months. Supervisory measures have contributed to some strengthening of lending standards. Taking account of the available information the Board judged that holding the stance of policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time. Statement by Philip Lowe, Governor: Monetary Policy Decision At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent. Conditions in the global economy have improved over recent months. Both global trade and industrial production have picked up. Labour markets have tightened in many countries. Above-trend growth is expected in a number of advanced economies, although uncertainties remain. In China, growth is being supported by higher spending on infrastructure and property construction. This composition of growth and the rapid increase in borrowing mean that the medium-term risks to Chinese growth remain. The improvement in the global economy has contributed to higher commodity prices, which are providing a significant boost to Australia’s national income. Headline inflation rates have moved higher in most countries, partly reflecting the higher commodity prices. Core inflation remains low. Long-term bond yields are higher than last year, although in a historical context they remain low. Interest rates have increased in the United States and there is no longer an expectation of additional monetary easing in other major economies. Financial markets have been functioning effectively. The Australian economy is continuing its transition following the end of the mining investment boom. Recent data are consistent with ongoing moderate growth. Most measures of business confidence are at, or above, average and non-mining business investment has risen over the past year. At the same time, some indicators of conditions in the labour market have softened recently. In particular, the unemployment rate has moved a little higher and employment growth is modest. The various forward-looking indicators still point to continued growth in employment over the period ahead. Wage growth remains slow. The outlook continues to be supported by the low level of interest rates. Lenders have recently announced increases in mortgage rates, particularly those paid by investors. Financial institutions remain in a good position to lend. The depreciation of the exchange rate since 2013 has also assisted the economy in its transition following the mining investment boom. An appreciating exchange rate would complicate this adjustment. Inflation remains quite low. Headline inflation is expected to pick up over the course of 2017 to be above 2 per cent. The rise in underlying inflation is expected to be a bit more gradual with growth in labour costs remaining subdued. Conditions in the housing market continue to vary considerably around the country. In some markets, conditions are strong and prices are rising briskly. In other markets, prices are declining. In the eastern capital cities, a considerable additional supply of apartments is scheduled to come on stream over the next couple of years. Growth in rents is the slowest for two decades. Growth in household borrowing, largely to purchase housing, continues to outpace growth in household income. By reinforcing strong lending standards, the recently announced supervisory measures should help address the risks associated with high and rising levels of indebtedness. Lenders need to ensure that the serviceability metrics that they use are appropriate for current conditions. A reduced reliance on interest-only housing loans in the Australian market would also be a positive development. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time. April 4 2017 2