Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

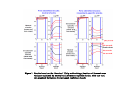

Investment-Specific and Neutral News Shocks and Macroeconomic Fluctuations∗ Luca Benati University of Bern† Abstract I use structural VAR methods to explore the role played by news and nonnews shocks–either investment-specific, or neutral–in macroeconomic fluctuations, thus allowing these four disturbances to ‘compete on equal grounds’ for the purpose of explaining the business cycle. Conceptually in line with the literature started by Beaudry and Portier (2006), news shocks almost uniformly dominate non-news disturbances. In line with Fisher (2006), investment-specific shocks play a more important role in macroeconomic fluctuations than neutral disturbances. Among the four disturbances I identify, the single most important one clearly appears to be the news investment-specific. Evidence suggest that this shock generates ‘disinflationary booms’, characterized by hump-shaped increases in hours, decreases in inflation, and increases in the ex post real rate. Keywords: Technology shocks; news shocks; structural VARs; unit roots. ∗ I wish to thank Franck Portier for helpful discussions, Lutz Kilian for extremely helpful suggestions on bootstrapping, and Eric Sims for comments. Usual disclaimers apply. † Department of Economics, University of Bern, Schanzeneckstrasse 1, CH-3001 Bern, Switzerland. Email: [email protected] 1 1 Introduction Since Fisher (2006) and Beaudry and Portier (2006), several researchers have explored the relative importance of investment-specific versus neutral technology, and of news versus non-news shocks in macroeconomic fluctuations. As it currently stands, this literature suffers from two main limitations. First, with the single exception of Beaudry and Lucke (2010), no previous study within the structural VAR literature has considered both news and non-news shocks to both neutral and investment-specific technology, thus allowing these four disturbances to ‘compete on equal grounds’ for the purpose of explaining macroeconomic fluctuations.1 For example, Beaudry and Portier (2006), Barsky and Sims (2011), Barsky and Sims (2012), and Kurmann and Otrok (2013) consider news and non-news neutral shocks, but eschew investment-specific disturbances, whereas Fisher (2006) considers neutral and investment-specific disturbances, but he does not allow for the possibility that (some of them) may be anticipated. Beaudry and Lucke (2010, henceforth, BL) considers both neutral and investment-specific shocks, allowing for the possibility that both types of shocks may be anticipated, but without further disentangling the identified news shocks into neutral and investment-specific.2 Further, as extensively discussed by Fisher (2010), BL’s (2010) analysis suffers from a number of limitations, starting from their assumption that the data contain three common stochastic trends, when, in fact, economic theory suggests that the number of common trends should be one. Second, with a single exception (discussed below), no paper within the structural VAR literature has yet explored the role of news investment-specific shocks per se. This omission in the literature is quite hard to rationalize: if there is one type of technological disturbance which, based on strictly logical grounds, we should expect to be largely anticipated, this is indeed the investment-specific one. Casual evidence clearly suggests that the technological innovations embodied in new capital or consumer durables goods are, in many cases, well publicized in advance,3 with the result that they can hardly be regarded as ‘surprises’, and belong instead most likely to the realm of news shocks. But if this is the case, then it is an open question to which extent previous analyses, by consistently focusing on surprise investmentspecific disturbances, have provided a correct picture of the role played by embodied technological change in macroeconomic fluctuations. 1 This point was stressed by Fisher (2010) in his comment on Beaudry and Lucke (2010), when he pointed out that ‘Fisher (2006) does not consider news shocks and Beaudry and Portier (2006) do not consider investment-specific shocks. So it is natural to ask what happens when you consider both at the same time.’ 2 Indeed, their identifying assumption for news shocks is that they are orthogonal, on impact, to both total factor productivity and the relative price of investment. 3 The most extreme example of this is provided by the frenzy which, over the last several years, has consistently surrounded the widely anticipated launch of new Apple products. 2 1.1 This paper: methodology, motivation, and main results In this paper I use structural VAR methods in order to explore the relative importance of these four shocks (investment-specific news and non-news, and neutral news and non-news) in macroeconomic fluctuations, thus allowing them to ‘compete on equal grounds’ for the purpose of explaining the business cycle. To the very best of my knowledge, this is the first paper to do so. The motivation for the present analysis is the same as Beaudry and Lucke’s (2010), and it is a compelling one: if, among a set of four candidate technology and news shocks, a researcher only considers some of them, it is an entirely open question just how robust the results (s)he obtains should be regarded. As a matter of logic, the only way to eliminate this problem is to jointly consider all of the four shocks together. I estimate VARs for the relative price of investment (henceforth, RPI), total factor productivity (henceforth, TFP), and six other standard macroeconomic series, and I identify neutral (henceforth, N) and investment—specific (henceforth, IS) shocks based on a slight modification of Uhlig’s (2003, 2004) ‘maximum fraction of forecast error variance’ methodology. I disentangle news and non-news disturbances based on the restriction that news shocks do not impact upon the relevant series (either TFP, or the RPI) at zero. My main results can be summarized as follows: first, in line with Fisher (2006), IS shocks (either news, or non-news) play a more important role in macroeconomic fluctuations than N disturbances. For either inflation or the ex post real rate, in particular, they consistently explain (based on median estimates) about half of the forecast error variance (henceforth, FEV) at all horizons, whereas N shocks explain about 10-15 per cent, and 15 per cent, respectively, of the corresponding FEVs of the two series. For hours, the fraction of FEV explained by IS shocks at horizons beyond 6 quarters is around 30 per cent, whereas the corresponding fraction explained by N shocks ranges between 3 and 13 per cent. Results are even stronger for consumption, with IS shocks explaining between 55 and 68 per cent of the FEV at either the business-cycle frequencies or longer horizons. Second, conceptually in line with the literature started by Beaudry and Portier (2006), news shocks almost uniformly dominate non-news disturbances. This is especially clear for consumption, stock prices, hours, inflation, and the ex post real rate, for which the differences between the fractions of FEV explained by the two types of disturbances is (based on median estimates) around 30 per cent or even more. Third, the single most important shock is the news investment-specific one. Evidence suggests that this disturbance generates a ‘disinflationary boom’, with a humpshaped increase in hours, a fall in inflation, and an increase in the ex post real rate. 1.2 Related literature To the very best of my knowledge, there are only two papers which are conceptually related to the present one. 3 BL (2010) explores the role played by ‘surprise’ IS and N disturbances , and by news shocks (which can be either IS or N, and are not further disentangled), in macroeconomic fluctuations, based on cointegrated VARs for TFP, the RPI, hours, stock prices, and the Federal Funds rate. Their main finding is that ‘[...] surprise changes in technology, whether it be of the disembodied or embodied nature, account for very little of fluctuations. In contrast, expected changes in technology appear to be an important force [...].’ Although groundbreaking, BL’s analysis suffers from a number of limitations. A first one–the imposition of three cointegrating relationships upon the data when, in fact, theory suggests that there should be only one–was already mentioned previously. As discussed by Fisher (2010, Section 2), however, several of their identifying restrictions might also be viewed with skepticism. For example, within the identification scheme BL labels as ‘ID2’, which combines long-run and short-run restrictions, N shocks are postulated to be the only shocks impacting TFP contemporaneously. This assumption, however, is problematic, because different from Fernald’s ‘purified TFP’ measure, the TFP series used by BL has not been cleansed in order to purge it from the spurious effects of unobserved input variation, with the result that any shock which affects the state of the business cycle (e.g., a monetary, or a preference shock) should be expected to impact upon it. By the same token, BL allow N shocks to have a long-run impact on IS technology, which, as pointed out by Fisher (2010), is in contrast with the standard assumption made in the literature that TFP and the RPI are driven by independent processes. After finishing the first draft of this paper, I was alerted to the the work of Zeev and Khan (2013),4 which is similar to the present work along several dimensions. Ben Zeev and Khan (2013, henceforth, BZK) estimate a nine-variable VAR in (log) levels, and identify news and non-news IS shocks, and a single N shock (without further disentangling it into a news and a non-news component), based on Uhlig’s (2003, 2004) ‘maximum fraction of forecast error variance’ approach. A problematic aspect of BZK’s analysis is that, different from both Fisher (2006), and the present work,5 they do not take the price of consumption to be the numeraire of the system, which implies that some of the key series entering their VAR–the relative price of investment, output, investment, and consumption–are not expressed in a common unit. This, in turn, logically implies that their results do not have a clearly-defined meaning, and a clearly-defined interpretation when seen from the perspective of DSGE models. Indeed, since within DSGE models consumption is routinely taken to be the numeraire of the system, for the results of structural VAR analyses to be able to meaningfully inform the construction of such models, they ought to follow the same data-normalization convention. 4 5 I wish to thank Eric Sims for alerting me to this paper. See the appendix on the construction of the data. 4 The paper is organized as follows. Sections 2 and 3 discuss in detail the key features of the reduced-form VARs used herein, and of my approach to the identification of the four structural disturbances, respectively. Section 4 discusses the evidence. Section 5 concludes. 2 The Reduced-Form VARs The VARs used in the analysis that follows feature the logarithms of the RPI and TFP; inflation; the real ex post 3-month Treasury bill rate;6 and the logarithms of hours worked, real GDP, real consumption, and real stock prices, all of them expressed in per capita terms (appendix A contains a detailed description of the series, and of the data sources). Following Fisher (2006), the price of consumption (i.e, the chainweighted deflator for non-durables and services) is taken to be the numeraire of the system, so that the relative price of investment, and consumption, GDP, and real stock prices per capita, are all expressed in a common unit. As I previously pointed out, this is key because otherwise it is as if the VAR had been estimated ‘based on apples and oranges’, with the consequence that the results it produces do not have any clearly-defined meaning. The sample period is 1948Q2-2006Q4. Both the beginning and the end of the sample are dictated by the sample period for which SGU’s RPI series is available.7 All of the VARs feature 4 lags, and are estimated in (log) levels via OLS. The key reason for estimating the models in (log) levels, rather than in (log) differences, is that, as extensively discussed by Hamilton (1994),8 the specification in levels is robust to the presence of cointegration of unknown form among the VAR’s endogenous variables, and is therefore going to produce consistent estimates of all the objects of interest (IRFs, fractions of forecast error variance, ...) without any need to take a specific stand on the number of cointegrating relationship. On the other hand, this is not the case for the specification in differences, whose inference’s reliability crucially hinges on the researcher imposing the correct number of cointegrating vectors in the VECM representation (as discussed in the introduction, this was one of Fisher’s (2010) key criticisms to Beaudry and Lucke (2010)). 6 I consider the 3-month Treasury bill rate, rather than the FED Funds rate, because the latter is only available since July 1954. 7 Ending the sample period in 2006Q4 is not really a problem, because in any case, in line with Justiniano, Primiceri, and Tambalotti (2011), I would have excluded the period of the financial crisis (which has been characterized by the zero lower bound becoming binding for the first time) in order to avoid my results being distorted. So in the end, even if I had had a longer RPI series, I would have used just a few more quarters. 8 See also the discussion in Barsky and Sims (2011). 5 3 3.1 Identification The ‘standard’ Uhlig (2003, 2004) methodology All of my evidence is based on the ‘maximum fraction of forecast error variance’ approach to identification pioneered by Uhlig (2003) and Uhlig (2004). Specifically, given the VAR(p) model = 0 + 1 −1 + + − + , 0 [ ] = Ω (1) with the moving-average representation = [(1)]−1 0 + [()]−1 ≡ () , where () ≡ − 1 − − , and () ≡ + 1 + 2 2 + 3 3 + , identification boils down to finding a mapping between the reduced-form forecast 0 errors, the , and the structural shocks, the , such that = 0 , with 0 0 = Ω. Uhlig’s approach is based on the notion of finding the first columns of 0 , with (where is the number of variables in the VAR), which identify the orthogonal shocks explaining the maximum fraction of the forecast error variance of a variable in either over some forecast horizon (e.g., between 6 and 32 quarters, which is the horizon traditionally associated with business-cycle frequency fluctuations), or at some specific horizon, say, 10 years ahead. In turn, since, given a matrix ∗0 such 0 that ∗0 (∗0 ) = Ω, and an orthonornal matrix such that 0 = , the matrix 0 0 = ∗0 also satisfies 0 0 = Ω, the search for 0 boils down–for a given starting 0 matrix ∗0 satisfying ∗0 (∗0 ) = Ω (e.g., the Cholesky factor of Ω)–to finding an appropriate orthonormal matrix . Given the -step-ahead forecast error for the -th variable in , " −1 # X 0 ∗ (2) 0 +− + − +| = =0 where is a selector vector with zeros everywhere and a 1 in the -th position, Uhlig (2003) shows that the orthogonal shocks explaining the maximum fraction of the forecast error variance of at horizon are associated with the first eigenvectors of the matrix X 0 0 0 = (∗0 ) ( ) ∗0 (3) =0 Figure 1 shows the results produced by this methodology for two possible alternative ‘orderings’ of the identified shocks. In the first two columns I start by identifying the N shocks as the two disturbances which explains the maximum fraction of the forecast error variance (henceforth, FEV) of log TFP at the 10 years-ahead horizon. I then rotate them in such a way that the news N shock does not impact upon TFP at zero. Then, conditional on having identified the N shocks, I identify the IS shocks as the two further disturbances explaining the maximum fraction of the FEV of log RPI at the same horizon, and I rotate them in such a way that the news IS shock 6 does not impact upon the RPI at zero.9 In the last two columns I instead do the opposite, by first identifying the IS shocks, and then, conditional on this, identifying the N shocks. The figure reports the fractions of FEV of TFP and the RPI at horizons up to 10 years ahead explained by the two identified types of shocks, IS and N, with one- and two-standard deviations bootstrapped confidence bands. I do not report results for the other series in the VAR because, for the present purposes, they are irrelevant. Following Barsky and Sims (2011), I bootstrap the VAR in levels, which is justified based on the results reported in Inoue and Kilian (2002).10 Finally, whereas in the entire paper I perform a bootstrap-based bias-correction of impulse-response functions (henceforth, IRFs) as in Kilian (1998), as for the fractions of FEV, both here and in the rest of the paper I do not perform any bias correction, so that the thick black lines shown in the figure 1 are just the simple estimates.11 3.1.1 The problem of ‘imperfect separation’ between IS and N shocks The results reported in Figure 1 highlight a key problem of the ‘standard’ Uhlig methodology within the present context. As the first two columns show, when N shocks are identified first, they also end up jointly explaining a comparatively large fraction of the FEV of the RPI. Further, when the ‘ordering of the shocks’ is inverted, so that IS shocks are identified first, although results clearly improve, they are still far from being satisfactory. In particular, at the 10-year horizon, the 95th percentile of the bootstrapped distribution of the fraction of FEV of TFP explained by IS shocks is around 45 per cent, whereas the median of the distribution is equal to 20 per cent. Overall, these results show that, within the present context, the standard Uhlig (2003, 2004) methodology does not succeed at ‘separating’ the two types of shocks in a fully satisfactory manner. Therefore, in what follows I will work with the modified version of the Uhlig procedure I describe in the next sub-section. 9 I also tried two alternative horizons, 15 and 20 years, and results were qualitatively the same. Although Inoue and Kilian (2002) only dealt with univariate processes, as confirmed to me by Lutz Kilian via email ‘[t]he extension of our Econometrica paper to the multivariate case is immediate [...]’. 11 The reason for this is the following. In a previous version of the paper I performed indeed a biascorrection for the fractions of FEV, with the result that, in some cases, some of the bootstrapped confidence bands ended up being either above 1 or below 0 for some horizon. Because of this, I then performed the bias-corrections based on the logit transformations of the relevant objects, and then I took the inverse-logit transformations of the resulting quantities. Although this approach, by construction, delivers bias-corrected fractions of FEV, and confidence bands, which are bounded between 0 and 1, it suffers form the drawback that, in some cases, the extent of the bias-correction turned out to be extremely (and, in my view, implausibly) large, due to the extreme non-linearity of the logit transformation for values quite close to either 0 or 1. Since neither of the two approaches appeared to be problem-free, in the end I simply decided to perform no bias correction, and to just show the simple estimates. 10 7 3.2 A ‘modified Uhlig-type methodology’ Since the problem documented in Figure 1 is ‘imperfect separation’ between N and IS shocks, I identify N shocks based on the restriction that they maximize the difference between the fraction of explained long-horizon FEV of TFP, and the corresponding fraction of explained long-horizon FEV of the RPI. The rationale for this is that we want N shocks to explain as much as possible of the long-horizon variation of TFP, and as little as possible of the corresponding long-horizon variation of the RPI. Maximizing the difference between the former and the latter achieves this objective. By the same token, I identify IS shocks symmetrically, by maximizing the difference between the explained fractions of long-horizon FEV of the RPI and of TFP. Different from the ‘standard’ Uhlig methodology, this modified version cannot be formulated as a straightforward eigenvalue-eigenvector problem (as least, I was not able to formulate it in this way), and requires instead numerical optimization methods. Specifically, for a given starting structural impact matrix ∗0 satisfying 0 ∗0 (∗0 ) = Ω, I define the orthonormal matrix as the product of all of the available rotation matrices ( ), where 2 ≤ ≤ is the dimension of the square submatrix along the diagonal of ( ) containing the sin( ) and cos( ) functions. For example, if were equal to 4 there would be three rotation matrices with = 2: ⎡ ⎡ ⎤ ⎤ sin(1 ) cos(1 ) 0 0 1 0 0 0 ⎢ -cos(1 ) sin(1 ) 0 0 ⎥ ⎢ ⎥ ⎥ 2 (2 ) = ⎢ 0 sin(2 ) cos(2 ) 0 ⎥ 1 (1 ) = ⎢ ⎣ ⎣ 0 -cos(2 ) sin(2 ) 0 ⎦ 0 0 1 0 ⎦ 0 0 0 1 0 0 0 1 ⎡ ⎤ 1 0 0 0 ⎢ 0 1 ⎥ 0 0 ⎥ (4) 3 (3 ) = ⎢ ⎣ 0 0 sin(3 ) cos(3 ) ⎦ 0 0 -cos(3 ) sin(3 ) By the same token, there would be two rotation matrices with = 3, and one with = 4, for a total of six. In our case, with = 8, the overall number of available rotation matrices is 28, and is defined as = −+1 Y Y =2 ( ) (5) =1 Then, e.g., when identifiying N shocks, I maximize the difference between the fractions of explained FEV of TFP and the RPI numerically, by searching, over the parameter space, for those specific values of the rotation angles (that is, the ’s) which maximize the criterion function. Although obviously not as fast as the standard Uhlig methodology (which, being based on the eigenvalue-eigenvector decomposition, is performed essentially ‘in zero time’) numerical optimization is quite fast, and identifying the first 8 ordered shock in the system took, on average, less than 10 seconds.12 Optimization was performed via MATLAB’s routine fminsearch.m, for random initial conditions. Since identification of the shocks is here based on numerical optimization of a criterion function, rather than on a matrix decomposition, the reader may have an obvious question: ‘How strong is identification? Is the criterion function unimodal, bimodal, or what?’. In order to address this question, I performed the following Monte Carlo experiment. Conditional on the OLS estimate of the covariance matrix of the VAR’s innovations, I performed the numerical optimization 1,000 times with random initial conditions, each time identifying the four shocks I discuss in the next sub-section (specifically: news and non-news N, and news and non-news IS). For each of the 1,000 numerical optimizations I have performed, the algorithm always converged to the same solution (up to machine precision). This clearly illustrates that identification here is as robust as it can possibly be. Finally, the strongest piece of evidence in favor of the reliability of this numerical optimization-based methodology is that when I used it–just to perform a check–in order to identify the single shock which explains the maximum fraction of the horizon forecast error variance of either TFP or the RPI, the solution I got was, up to machine precision, identical to the one produced by the ‘standard’ Uhlig methodology. Let’s now turn to the results. 4 Evidence I order the RPI and TFP first and second, respectively, I estimate the VAR, and I proceed to identify four shocks–news and non-news IS, and news and non-news N–as follows. First, I identify the news-IS shock based on the restrictions that (i) it maximizes the difference between the explained fractions of FEV of the RPI and TFP at the 10-year horizon, and (ii) it has a zero impact on the RPI at =0. Second, conditional on having identified the news-IS shock, I identify the nonnews-IS shock based on the only restriction that it maximizes the difference between the explained fractions of FEV of the RPI and TFP (for the sake of simplicity, from now on I drop the qualification ‘at the 10-year horizon’). Third, conditional on having identified the two IS shocks, I identify the newsN shock based on the restrictions that (i) it maximizes the difference between the explained fractions of FEV of TFP and the RPI, and (ii) it has a zero impact on TFP at =0. Fourth, conditional on the previously identified three shocks, I identify the nonnews-N shock based on the only restriction that it it maximizes the difference between 12 When, conditional on having identified previous shocks in the system, you move to identifying subsequent ones, computing time for these subsequent optimization problems decreases dramatically, because they are associated with smaller sub-systems, and therefore a smaller number of angles ’s upon which optimization is performed. 9 the explained fractions of FEV of TFP and the RPI. Figures 2-8 shows the results. Specifically, Figure 2 reports the fractions of individual series’ FEVs explained by each of the four types of shocks (IS, N, news and non-news), together with the one and two-standard deviations bootstrapped confidence bands; Figure 3 reports the same objects, but this time for each of the four individual identified shocks; and Figure 4 reports bias-corrected IRFs to each of the four identified shocks, together with one and two-standard deviations bootstrapped confidence bands. Bias-correction of the IRFs and computation of the confidence bands has been implemented as in Kilian (1998). On the other hand, as previously pointed out, as for the fractions of FEV shown in Figures 2-3 I do not perform any bias correction. The vertical bars reported in Figures 2-3, corresponding to 6 and 32 quarters, mark the boundaries of the business-cycle frequency band.13 IRFs have been normalized in such a way that the median 10-year ahead impact of either IS shock on the log RPI is equal to -1, whereas the corresponding median impact of either N shock on TFP is equal to 1. Finally, Figures 5-8 show results from counterfactual simulations for four key periods (the 1950s, the Great Inflation episode, the ‘New Economy’ of the second half of the 1990s, and the years leading up to the financial crisis) in which identified shocks have been ‘killed off’ one at a time. 4.1 Separation between the IS and N shocks A comparison between the results shown in the last two columns of Figure 1, and those reported in the four panels in the left uppermost corner of Figure 2 shows how, within the present context, the ‘modified Uhlig procedure’ I am using herein is significantly more successful at separating IS and N shocks than the standard Uhlig procedure. In either case, the two types of shocks explain close to 100 per cent of the long-horizon FEV of the ‘own series’ (TFP for N shocks, and the RPI for IS shocks), whereas they explain close to zero per cent of the long-horizon FEV of the other series. Let’s now turn to discussing the results in detail. 4.2 4.2.1 The role played by the different types of shocks IS versus N shocks The results reported in the first two rows of Figure 2 address the issue of the relative importance of IS versus N shocks in macroeconomic fluctuations, which was originally put forward by Fisher (2006). Overall, evidence is qualitatively, although not quantitatively, in line with Fisher’s, with the fractions of business-cycle (henceforth, BC) frequency FEVs of individual non-technology series explained by IS shocks being most of the time greater than the corresponding fractions due to N shocks. This 13 This is the standard convention in the literature, see e.g. Baxter and King (1999) and Christiano and Fitzgerald (2003). 10 is especially clear for the three non-technology series which entered Fisher’s (2006) VAR–hours, inflation, and the interest rate14 –for which IS shocks clearly dominate N shocks. Specifically, for either inflation or the ex post real rate IS disturbances consistently explain (based on median estimates) about half of the FEV at all horizons, whereas N shocks explain about 10-15 per cent, and 15 per cent, respectively, of the corresponding FEVs of the two series. As for hours, the fraction of FEV explained by IS shocks at horizons beyond 6 quarters is around 30 per cent, whereas the corresponding fraction explained by N shocks ranges between 3 and 13 per cent. Results are even stronger for consumption, with IS shocks explaining between 55 and 68 per cent of the FEV at either the business-cycle frequencies or longer horizons. For GDP results are comparatively less strong, with IS disturbances explaining between 30 and 50 per cent of the FEV at horizons beyond one year and a half, whereas N shocks explain between 20 and 37 per cent. Finally, stock prices is the only series for which N shocks dominate IS shocks, with the fraction of FEV explained by the former declining from 75 per cent on impact to 46 per cent at the 10-year horizon, whereas the fraction explained by the latter rise from about 6 per cent on impact, to a maximum of 31 per cent at the 10 year horizon. 4.2.2 News versus non-news shocks A comparison between the results reported in the last two rows of Figure 2 shows how, with only two exceptions, news shocks uniformly dominate non-news disturbances across the board, explaining significantly larger fractions of the FEV at almost all horizons. This is especially apparent for consumption, stock prices, hours, inflation, and the ex post real rate, for which the differences between the fractions of FEV explained by the two types of disturbances is (based on median estimates) in the ballpark of 30 per cent or even more. As for the RPI, the fraction of FEV explained by news shocks starts close to zero, but it rises quite rapidly with the forecast horizon, surpassing (based on median estimates) the corresponding fraction explained by nonnews disturbances at the 4-years ahead horizon. At the 10-years ahead horizon, the two types of disturbances explain 62.5 and 36 per cent of the FEV of the RPI, respectively. The only two series for which news shocks are not clearly dominant are GDP and TFP. As for GDP, at horizons beyond one year and a half neither of the two types of disturbances dominates the other, and they both explain fractions of FEV between 30 and 40 per cent. As for TFP, on the other hand, news shocks play a minor role, with a fraction of explained FEV rising to a maximum of 24 per cent at the 10-year horizon, whereas the corresponding fraction explained by non-news shocks decreases monotonically with the forecast horizon, but it is still equal to 73 per cent at the 10-year horizon. Let’s now dig deeper, looking at the role played by individual structural shocks. 14 To be precise, Fisher’s VAR featured a nominal interest rate, rather than an ex post real interest rate, so that for this variable results are not exactly comparable. 11 4.3 The role of individual shocks The following findings emerge from Figure 3. The IS news shock appears to be the single most important one among the four disturbances identified herein. This is especially clear for consumption, hours, inflation, the ex post real rate, and the RPI, whereas for GDP the importance of IS news shocks is comparable to that of non-news N disturbances. On the other hand, IS non-news shocks play a uniformly negligible role for all series with the single exception of the RPI. By the same token, news N shocks play a uniformly negligible role for all series with the single exception of stock prices, for which they explain (based on median estimates) between 40 and 60 per cent of the FEV at horizons beyond one years and a half. Finally, non-news N shocks play a dominant role for TFP; a negligible one for the RPI, stock prices, hours, inflation, and the real rate; and and non-negligible roles for consumption and GDP, explaining around 25-30 percent of the FEV of the two series at horizons beyond 3 years. Let’s now turn to the response of the economy to either of the four identified structural disturbances. 4.4 How do individual shocks impact upon the economy? As expected, either of the two identified IS shocks has a statistically significant longhorizon impact upon the RPI (which, as previously pointed out, has been normalized in such a way that the median of the 10-year ahead impact is equal to -1), and a statistically insignificant impact on TFP at all horizons. By the same token, either of the two identified N shocks has a statistically significant long-horizon impact upon TFP (which has been normalized so that its median long-horizon impact on TFP is equal to 1), and a statistically insignificant impact on the RPI at all horizons. News IS shocks have a positive and statistically significant long horizon impact on consumption, GDP, and stock prices, and an insignificant impact on hours and the ex post real rate. Contrary to what one would have expected, IS shocks are also estimated to have a negative and statistically significant impact on inflation. This, together with the analogous negative long-horizon impact on inflation of nonnews IS shocks represents the only manifestly problematic feature of the set of IRFs plotted in Figure 4. Turning to the impact of IS news shocks at =0, it is positive and statistically significant for consumption and the real rate, whereas it is negative and again strongly statistically significant for inflation. As for hours, although the impact at zero is not significant, the response going forward becomes positive and strongly statistically significant, with an overall broadly hump-shaped pattern. The first row of Figure 4 therefore suggests that, in response to a positive news IS shock, the economy experiences a ‘disinflationary boom’, with an increase in hours, a fall in inflation, and a less than one-for-one change in the nominal interest rate, which causes an increase in the ex post real rate. Conceptually in line with the analyses 12 of Greenwood, Hercowitz, and their co-authors,15 a plausible interpretation of the positive impact on hours of news IS shocks is that, in the presence of anticipation about a technological improvement embodied in capital goods which will come on the market at some future date, firms have an incentive to accelerate the depreciation of existing capital goods, and will therefore increase their utilization rate. In turn, given a plausible extent of complementarity between capital and hours worked, this will automatically translate into an analogous increase in hours worked. The IRFs shown in the second row highlight how, in response to IS non-news disturbances, none of the variables in the VAR experiences any statistically significant change on impact, and in most cases the response is insignificant even at most horizons after impact. This is especially clear for consumption, GDP, and hours. The obvious explanation for the comparatively large extent of uncertainty characterizing the response of the economy to IS non-news shocks (which is at the root of the lack of statistical significance) is that, as discussed in the previous section, these shocks explain negligible fractions of the FEV of all series with the single exception of the RPI. As a result, since all series other than the RPI contain very little information about these shocks, it is not surprising that the responses to them are very imprecisely estimated. The same problem plagues most IRFs to either of the two N shocks. Since, as discussed in the previous section, these two shocks also explain, most of the time, little to nothing of the variance of most series, it is once again to be expected that IRFs to these disturbances be imprecisely estimated. This is indeed what the last two rows of Figure 4 show, with IRFs being, in most cases, not significantly different from zero at most horizons. These results contrast sharply with those of Barsky and Sims (2011), who, based on VARs featuring the same TFP series used herein, but no RPI series, identified negative responses of hours, GDP, investment, and inflation to news N shocks. Figure 3 provides a simple explanation for the contrast between my results and those produced by Barsky and Sims (2011). Within the present framework– which, it is important to stress, encompasses Barsky and Sims’ setup in terms of both the series entering the VAR, and the identification strategy–the news N shock is compelled to compete on equal grounds not only with non-news N shocks (as in Barsky and Sims (2011)), but also with either news or non-news IS shocks. As the results in Figure 3 show, under these circumstances the news N shock clearly emerges as a loser from this competition, which is instead won, hands down, by the news IS shock. Within Barsky and Sims’ VAR, on the other hand, not only IS shocks and not identified, but no information about them is in fact contained in the VAR, because the RPI is not among the variables entering the model. As a result, their approach mechanically allocates the FEV of all the series in the VAR to shocks other than IS. For the reason discussed in the Introduction (the obvious lack of a ‘level playing field’ in the competion for the allocation of the variance among the various possible 15 See Greenwood, Hercowitz, and Huffmann (1988), Greenwood, Hercowitz, and Huffmann (1997), and Greenwood, Hercowitz, and Krusell (2000). 13 shocks) Barsky and Sims’ approach therefore necessarily provides an incomplete and possibly distorted picture of the role played by news and non-news IS and N shocks in macroeconomic fluctuations. Further, as my results show, the extent of the distortion is also not negligible, for the simple reason that, based on my results, Barsky and Sims (2011) are igoring the single most important shock out there. So my own reading of the evidence is that, since my framework encompasses the one used by Barsky and Sims (2011) in terms of both data and identification startegy, my results should be regarded as more reliable than theirs. Let’s now turn to examining how individual disturbances account for specific episodes of post-WWII U.S. economic history. 4.5 4.5.1 How do individual disturbances account for specific episodes? The 1950s Figure 5 shows results from counterfactual simulations for the period 1950Q1-1959Q4, in which I have re-run history based on the historical conditions prevailing up to the end of 1949 (that is: based on the values taken by the VAR’s endogenous variables as of 1949Q4), and by ‘killing off’ one identified shock at a time. Overall, neither of the four sets of simulations produces results which stand out in any particular way. For consumption, e.g., either of the four counterfactual paths is remarkably close to the actual historical path, and in three cases out of four it is essentially indistinguishable from it. For TFP, only killling off non-news N shocks makes a material difference, with the counterfactual path being systematically lower than the actual path until 1956, and being instead above it after that, and very much so towards the end of the decade. Such an alternative counterfactual path for TFP maps into a corresponding alternative path for GDP: as the fourth panel in the last row shows, the evolution of counterfactual GDP mimics that of TFP, being below actual GDP until the mid1950s, and above it after that. The same holds, to a slightly lesser extent, for stock prices and hours. Killing off news N shocks makes essentially no difference for either series, with the single notable exception of stock prices, for which the counterfactual path would have been mostly higher until the mid-1950s, and somehow lower at the end of the decade. The material difference news N shocks make in the case of stock prices is logically to be expected in the light of the results reported in Figure 3, in which we saw that these shocks are the only ones to play an important role for this variable. Eliminating non-news IS shocks only makes a material difference for the RPI (although the difference between the counterfactual and actual paths is never statistically significant at the 10 per cent level), whereas it makes essentially no difference for either of the other series. Finally, eliminating news IS shocks makes some difference, although not an especially large one, for several series such as GDP, hours, inflation, and the ex post rate. 14 Overall, however, counterfactuals for the 1950s do not produce especially striking or interesting results. 4.5.2 The Great Inflation Figure 6 shows results from analogous counterfactual simulations for the period 1965Q1-1979Q3, in which I have re-run history based on the historical conditions prevailing as of 1964Q4fs. Two main findings emerge from the series of counterfactuals. First, among the shocks identified herein, the only one which is estimated to have played an important role in U.S. macroeconomic dynamics between the mid-1960s and the end of the 1970s is the IS news one. Indeed, whereas killing off either of other three shocks generates counterfactual paths for the endogenous variables which are virtually indistinguishable, and not significantly different, from the actual series (the only obvious exception to this is the news N shock for stock prices), eliminating the IS news shocks makes a material difference for consumption, GDP, hours, and the ex post real rate, which would all have been lower until the early 1970s. As for inflation, the counterfactual path is somehow higher than the actual one between 1965 and 1967, and it is lower between 1973 and 1975. In both cases, however, the differences are not large. Second, with the just-mentioned, partial exception of the news IS shock, none of the identified shocks appears to have played an important role for the evolution of inflation during those years. This is consistent with the widespread notion that the main underlying cause of the Great Inflation of the 1970s was a series of policy mistakes which, through sins of either omission or commission, ultimately led to an excessively loose monetary policy stance.16 4.5.3 The Volcker disinflation As for the Volcker disinflation, counterfactual simulations17 clearly suggest that, unsurprisingly, neither of the four disturbances identified herein played any significant role in that episode. This is reassuring because, as stressed by King and Watson (1994), we should be highly suspicious of identified supply-side shocks which are estimated to have played an important role within this episode. Since these results are uniformly negative, for reasons of space I do not report them, but they are available upon request. 16 See e.g. Clarida, Gali, and Gertler (2000), Barsky and Kilian (2001), and, for an overview, Benati and Goodhart (2011). 17 I start the counterfactuals for the Volcker disinflation at 1979Q4. 15 4.5.4 The ‘New Economy’ boom of the second half of the 1990s Results for the second half of the 1990s18 are broadly in line with the evidence for the Great Inflation period, with news N shocks only making a material difference for stock prices (which would have been consistently lower), and news IS shocks emerging, once again, as the the only disturbances which would have made some difference for most series. Killing off these shocks would indeed have produced slightly lower paths for consumption, GDP, hours, and the ex post real rate, and a slightly higher path for hours. In no case, however, the difference is statistically significant at conventional levels. 4.5.5 The years leading up to the financial crisis The counterfactuals we have seen up until now do not point towards truly significant differences produced by killing off any of the four identified shocks. Things change significantly, however, when we move to the years leading up to the financial crisis.19 As the second and fourth rows of Figure 8 show, killing off either non-news IS or non-news N shocks would still have produced insignificantly different counterfactual paths for either series, and news N shocks would once again have made a material difference only for stock prices, and only for the very first years of the counterfactual. Killing off news N shocks, on the other hand, would have produced significantly lower counterfactual paths for the RPI and inflation, and significantly higher paths for consumption, GDP, stock prices, hours, and the ex post real rate. This suggests that, during the 2000s, IS news shocks’ overall contribution to growth was in fact negative, and originates from the deceleration in the rate of decrease of the RPI during those years–see panel (1,1) of Figure 8–which, within the present fixedcoefficients framework, is automatically interpreted in terms of a series of adverse shocks. 5 Conclusions In this paper I have used structural VAR methods to explore the role played by news and non-news shocks–either investment-specific, or neutral–in macroeconomic fluctuations, thus allowing these four disturbances to ‘compete on equal grounds’ for the purpose of explaining the business cycle. In line with Fisher (2006), investmentspecific shocks (either news, or non-news) are estimated to have played a more important role in macroeconomic fluctuations than neutral disturbances. Conceptually in line with the literature started by Beaudry and Portier (2006), on the other hand, 18 I start counterfactuals simulations for the New Economy period at 1995Q1. I start these counterfactuals immediately after the end of the ‘dotcom recession’, that is, in 2002Q1. 19 16 my results suggest that news shocks almost uniformly dominate non-news disturbances. The single most important shock clearly appears to have been the news investment-specific one. My results suggest that this disturbance generates ‘disinflationary booms’, characterized by hump-shaped increases in hours, decreases in inflation, and increases in the ex post real rate. 17 References Barsky, R., and E. Sims (2011): “News Shocks and Business Cycles,” Journal of Monetary Economics, 58(3), 273—289. (2012): “Information, Animal Spirits, and the Meaning of Innovations in Consumer Confidence,” American Economic Review, 102(4), 1343—1377. Barsky, R. B., and L. Kilian (2001): “Do We Really Know That Oil Caused the Great Stagflation? A Monetary Alternative,” NBER Macroeconomics Annual, 16, 137—183. Baxter, M., and R. King (1999): “Approximate Band-Pass Filters for Economic Time Series: Theory and Applications,” Review of Economics and Statistics, 81(4), 575—593. Beaudry, P., and B. Lucke (2010): “Letting Different Views About Business Cycles Compete,” In: NBER Macroeconomics Annual 2009, 24, 413—455. Beaudry, P., and F. Portier (2006): “Stock Prices, News, and Economic Fluctuations,” American Economic Review, 96(4), 1293—1307. Benati, L. (2013): “Business-Cycle Shocks,” University of Bern, mimeo. Benati, L., and C. Goodhart (2011): “Monetary Policy Regimes and Economic Performance: The Historical Record, 1979-2008,” in B. Friedman, B., and Woodford, M. (eds.), Handbook of Monetary Economics, Volume 3, North Holland. Blanchard, O. J., and D. Quah (1989): “The Dynamic Effects of Aggregate Demand and Supply Disturbances„” American Economic Review, 79(4), 655—673. Christiano, L., and T. Fitzgerald (2003): “The Band-Pass Filter,” International Economic Review, 44(2), 435—465. Clarida, R., J. Gali, and M. Gertler (2000): “Monetary Policy Rules and Macroeconomic Stability: Evidence and Some Theory,” Quarterly Journal of Economics, CXV(1), 147—180. Fisher, J. D. (2006): “The Dynamic Effects of Neutral and Investment-Specifc Technology Shocks,” Journal of Political Economy, 114, 413—451. (2010): “Discussion of: Letting Different Views About Business Cycles Compete,” in: NBER Macroeconomics Annual 2009, 24. Gali, J. (1999): “Technology, Employment, and the Business Cycle: Do Technology Shocks Explain Aggregate Fluctuations?,” American Economic Review, 89(1), 249— 71. 18 Greenwood, J., Z. Hercowitz, and G. W. Huffmann (1988): “Investment, Capacity Utilization and the Business Cycle,” American Economic Review, 73(3), 402—417. (1997): “Long-Run Implications of Investment-Specific Technical Change,” American Economic Review, 87(3), 342—362. Greenwood, J., Z. Hercowitz, and P. Krusell (2000): “The Role of Investment-Specific Technological Change in the Business Cycle,” European Economic Review, 44, 91—115. Hamilton, J. (1994): Time Series Analysis. Princeton, NJ, Princeton University Press. Inoue, A., and L. Kilian (2002): “Bootstrapping Autoregressive Processes with Possible Unit Roots,” Econometrica, 70(1), 377—391. Justiniano, A., G. Primiceri, and A. Tambalotti (2011): “Investment Shocks and the Relative Price of Investment,” Review of Economic Dynamics, 14(1), 101— 121. Kilian, L. (1998): “Small-Sample Confidence Intervals for Impulse-Response Functions,” Review of Economics and Statistics, pp. 218—230. King, R., and M. Watson (1994): “The Post-War U.S. Phillips Curve: A Revisionist Econometric History,” Carnegie-Rochester Conference Series on Public Policy, 41, 157—219. Kurmann, A., and C. Otrok (2013): “News Shocks and the Slope of the Term Structure of Interest Rates,” American Economic Review. Kydland, F. E., and E. C. Prescott (1982): “Time To Build and Aggregate Fluctuations,” Econometrica, 50, 1345—1370. Liu, Z., D. F. Waggoner, and T. Zha (2011): “Sources of Macroeconomic Fl uctuations: A Regime-Switching DSGE Approach,” Quantitative Economics, 2(2), 251—301. Prescott, E. (1986): “Response to a Skeptic,” Federal Reserve Bank of Minneapolis Quarterly Review, Fall 1986. Schmitt-Grohé, S., and M. Uribe (2011): “Business Cycles with a Common Trend in Neutral and Investment-Specific Productivity,” Review of Economic Dynamics, 14, 122—135. Uhlig, H. (2003): “What Drives GNP?,” Unpublished manuscript, Euro Area Business Cycle Network. 19 (2004): “Do Technology Shocks Lead to a Fall in Total Hours Worked?,” Journal of the European Economic Association, 2(2-3), 361—371. Zeev, N. B., and H. Khan (2013): “Investment-Specific News Shocks and U.S. Business Cycles,” European University Institute, mimeo. 20 A The Data The quarterly seasonally adjusted series for the RPI is from Schmitt-Grohé and Uribe (2011). The sample period is 1948Q1-2006Q4. The TFP series has been computed based on the quarterly seasonally adjusted series for the log-difference of ‘purified TFP’ produced by John Fernald–which is widely regarded as the best available measure of neutral technology–and found at the San Francisco FED’s website. Specifically, the series for the logarithm of TFP has been computed as the cumulative sum of Fernald’s series for the log-difference of purified TFP. A quarterly seasonally adjusted series for the consumption deflator has been computed by chain-weighting the deflators for non-durables and services consumption based on the data found in Tables 1.1.6, 1.1.6B, 1.1.6C, and 1.1.6D of the National Income and Product Accounts. Inflation has been computed as the log-difference of the consumption deflator. By the same token, a quarterly seasonally adjusted series for real consumption of non-durables and services has been computed by chainweighting the respective series for real chain-weighted consumption of non-durables, and of services, respectively, based on the data found in the same tables. A monthly series for the 3-Month Treasury bill rate (TB3MS) is from the St. Louis FED’s website, and it has been converted to the quarterly frequency by taking averages within the quarter. The series is quoted at a non-annualized rate in order to make its scale exactly comparable to that of inflation.20 The real ex post 3-Month Treasury bill rate has been computed as the difference between the thus rescaled 3-Month Treasury bill rate series and inflation. A monthly series for the civilian noninstitutional population (CNP16OV) is from the U.S. Department of Labor, Bureau of Labor Statistics, and it has been converted to the quarterly frequency by taking averages within the quarter. A quarterly seasonally adjusted series for hours of all persons in the nonfarm business sector (HOANBS) is from the U.S. Department of Labor, Bureau of Labor Statistics. A monthly series for the nominal Standard & Poor’s composite index is from Robert Shiller’s website, and it has been converted to the quarterly frequency by taking averages within the quarter. Real stock prices have been computed by deflating the nominal Standard & Poor’s composite index by the consumption deflator. Finally, quarterly seasonally adjusted series for real GDP in chained 2005 dollars (GDPC96) and for the chained GDP deflator (GDPCTPI) are from the U.S. Department of Commerce, Bureau of Economic Analysis. As discussed in the text, the price of consumption is taken to be the numeraire of the system, and real GDP is therefore multiplied by the GDP deflator, and then divided by the consumption deflator (the resulting series is near-numerically identical 20 So, to be clear, defining the original 3-month Treasury bill rate series as –with its scale such that, e.g., a ten per cent rate is represented as 10.0–the rescaled series is computed as =(1+ /100)14 -1. 21 to the one obtained by simply deflating nominal GDP by the consumption deflator). Finally, hours worked, real GDP, real consumption, and real stock prices are all expressed in per capita terms by dividing them by population. 22 Figure 1 Results based on the ‘standard’ Uhlig methodology: fractions of forecast error variance explained by neutral and investment-specific shocks, with one- and two-standard deviations bootstrapped confidence bands 22 Figure 2 Fractions of forecast error variance explained by individual shocks, by type of shock, with one- and two-standard deviations bootstrapped confidence bands (based on the ‘modified Uhlig methodology’) 23 Figure 3 Fractions of forecast error variance explained by individual shocks, with one- and two-standard deviations bootstrapped confidence bands (based on the ‘modified Uhlig methodology’) 24 Figure 4 Impulse-response functions to structural shocks, with one- and two-standard deviations bootstrapped confidence bands 25 Figure 5 Counterfactuals for the 1950s obtained by ‘killing off’ individual structural shocks, with one- and two-standard deviations bootstrapped confidence bands (based on the ‘modified Uhlig methodology’) 26 Figure 6 Counterfactuals for the Great Inflation episode obtained by ‘killing off’ individual structural shocks, with one- and two-standard deviations bootstrapped confidence bands (based on the ‘modified Uhlig methodology’) 27 Figure 7 Counterfactuals for the ‘New Economy’ period, obtained by ‘killing off’ individual structural shocks, with one- and two-standard deviations bootstrapped confidence bands (based on the ‘modified Uhlig methodology’) 28 Figure 8 Counterfactuals for the period leading up to the financial crisis, obtained by ‘killing off’ individual structural shocks, with one- and two-standard deviations bootstrapped confidence bands (based on the ‘modified Uhlig methodology’) 29