Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

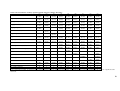

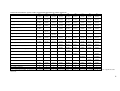

The determinants of railway development in Latin America before 1914 Vincent Bignon* Rui Esteves† Alfonso Herranz-Loncán‡ Abstract Railways were one of the main growth engines of Latin American economies during the first globalization boom. This paper analyses which were the main determinants of differences in railway development among Latin American countries, i.e. which factors made some destinations more attractive than others for foreign investors. It tries to ascertain if differences in railway expansion were mainly the consequence of fundamental geographical characteristics or if institutional factors and financial rationing dynamics had also a significant effect on each country’s degree of railway development. The results of the analysis provide evidence in favour of a significant impact of political instability and financial rationing on the pace of railway expansion in each country. This might be taken as evidence that the first globalization constituted a lost opportunity for some Latin American economies, which could not take advantage of all their economic potential. Very preliminary, please do not quote * Banque de France; email: [email protected] Brasenose College, Oxford; email: [email protected] ‡ University of Barcelona; email: [email protected] We thank Rodrigo Rivero and César Yáñez for sharing with us unpublished population data. † 1 1. Introduction Railways were one of the main growth engines of Latin American economies during the first globalization boom. Their potential capacity to transform the economies they served was probably much more important in that region than in the Western European countries, where the railway technology had actually been developed, for two reasons. Firstly, due to the almost total absence of transport infrastructure and the scarcity of waterways in the region by the mid-nineteenth century, railways constituted the only available way to connect most of the territory of those countries with the international markets. Secondly, during the first globalization wave, Latin American economies’ expansion was mainly based on natural resources exports and, therefore, the growth potential of the region crucially depended on the spread of a good transport system throughout the largest possible portion of the territory. As a consequence, in those countries that built extensive railway networks during the first globalization, export expansion and, therefore, GDP growth was closely linked to railway development. This direct link allowed Summerhill (2006: 297) to suggest that it “(…) seems unlikely that any other technological or institutional innovation was more important in the transition to economic growth in Latin America before 1930”. The crucial role of Latin American railways before 1914 has been confirmed, for some countries, by the social saving literature. In Argentina (Summerhill, 2000; Herranz-Loncán, 2011), Mexico (Coatsworth, 1979) and Brazil (Summerhill, 2003), because of the lack of cheap transport alternatives, the railways provided social savings amounting on average of ca. one quarter of total GDP by 1910-13. Social savings were much lower in Uruguay (Herranz-Loncán, forthcoming), because the geography of this country provided it with exceptional natural transport advantages, which made the railways less indispensable. But, apart from this case, it seems that those Latin American countries that built extensive railway networks before 1914 obtained huge direct benefits from railway transport. However, despite the high potential growth impact of the railways, in many Latin American countries, railway development was sluggish and the final network mileage was disappointingly low. Actually, apart from Mexico, Cuba, and the Southern Cone countries (Chile, Argentina and Uruguay), no integrated national railway network was constructed in Latin America and, in many countries, railways consisted just of a few isolated lines running from some production areas to the ports. As a consequence, the new infrastructure seems to have exerted a minor role in several Latin American economies during the first globalization boom. For instance, in the case of Colombia, the estimates of the social savings of railway freight transport in the late 1920s are just 3 to 8 percent of GDP (Ramírez, 2001), i.e. not higher than estimates for industrialized economies in the late 19th century. This paper looks into the potential reasons that may explain differences in railway development among Latin American countries during the first globalization. More specifically, given that most Latin American railway investment was financed by foreign private capital, it aims at analyzing which factors made some destinations more attractive than others for foreign investors. In this regard, decisions on the allocation of investment might have responded to the profitability prospects of each line, which depended in turn on the potential international demand of the specific natural resources of each area, the potential sources of internal transport demand (such as population 2 density), or ruggedness and its effect on construction costs. However, they may also have been influenced by the perceived degree of institutional instability of each country, as well as by the existence of some kind of rationing of some countries by the financial markets. The latter, in turn, might have had an informational origin (if, for instance, a country was poorly included in the networks of international financial intermediaries), or could be linked to other factors, such as previous defaults, or the financial intermediary that dominated each country’s relationship with the international capital markets (Clemens and Williamson, 2004; Haber, 1997; Marichal, 1989). The answers to these questions are highly relevant to get a better understanding of the reasons of the differential growth record of Latin American countries in a crucial period of their economic development. As has been indicated, in many cases, a sufficient endowment of transport infrastructure was an absolutely essential condition to take advantage of the opportunities open by the international markets during the first globalization. If the absence of railways was mainly the consequence of fundamental geographical hindrances (such as bad relief, or the scarcity of valuable natural resources), insufficient transport infrastructure would just be another dimension of some countries’ bad luck in the commodity lottery of the late 19th century (Díaz Alejandro, 1984). If, by contrast, institutional factors and financial rationing dynamics had an effect on the degree of railway development in each country, this might be taken as evidence that the first globalization constituted a lost opportunity for some Latin American economies and, more generally speaking, as an additional argument in favour of the crucial role of institutions on long-term economic development. We are not aware of any previous research on the factors explaining differences in railway development among Latin American countries. The main antecedent of this paper is Bogart (2009), which examines whether nationalizations reduced railway mileage growth in a sample of 29 countries of all over the world between 1860 and 1912. In this paper, we take a similar approach, although with a different cross-section and time sample, and considering a different potential set of determinants of railway development. The next section provides a very quick overview of the history of railway expansion in Latin America before 1914; Section 3 presents an econometric model in which we try to ascertain the influence of several factors on the dynamism of railway construction in each economy; and finally Section 4 concludes. 2. Railway expansion in Latin America before 1914 By 1914 railways were present all over Latin America, although their development had been highly unequal among countries. The first railway line in the region was open in Cuba in 1837, only 12 years after the inauguration of the first British railway. Cuba would not be joined by any other Latin American economy until the 1850s, when railway construction started slowly in Argentina, Brazil, Chile, Colombia, Costa Rica, Mexico or Peru. By 1900, all countries of the region had some railways in operation. Railway construction was especially intense in Argentina, Brazil and Mexico. These countries accounted, since the late 1880s, for approximately 75 percent of the whole Latin American railway mileage. However, in terms of railway density, they fell behind some small Central American and Caribbean countries, as may be seen in Tables 3 1 and 2, due to their large surface area and the low settlement rates of some parts of their territory. Table 1. Railway mileage in Latin America (1890-1912) (km) 1890 1900 Argentina 9,254 16,767 Brazil 9,973 15,316 Mexico 9,718 13,585 Chile 2,747 4,354 Cuba 1,731 1,960 Peru 1,599 1,800 Uruguay 983 1,730 Bolivia 209 972 Colombia 358 644 Venezuela 454 858 Guatemala 186 640 Costa Rica 241 388 Ecuador 92 92 Paraguay 240 240 Puerto Rico 18 223 Nicaragua 143 225 El Salvador 87 116 Dominican R. 115 182 Honduras 96 96 Haiti 0 37 Panama TOTAL 38,244 60,225 Source: See the Appendix. Note: Panama is included within Colombia both in 1890 and in 1900. 1912 32,212 23,491 20,447 7,260 3,803 3,276 2,522 1,284 1,061 858 808 619 587 373 354 322 320 241 170 103 76 100,187 4 Table 2. Railway density in Latin America (1890-1912) (km per 100 km2) 1890 1900 1912 Puerto Rico 19.77 244.95 388.84 Cuba 151.90 171.99 333.72 Salvador 41.99 55.98 154.44 Uruguay 52.71 92.77 135.24 Costa Rica 46.53 74.90 119.50 Argentina 32.72 59.28 113.89 Chile 38.99 59.19 109.71 Mexico 49.31 68.93 103.74 Guatemala 17.10 58.83 74.28 Dominican R. 23.37 36.98 48.97 Haiti 0.00 12.99 36.15 Brazil 11.98 18.39 27.60 Nicaragua 11.04 17.37 24.86 Paraguay 14.95 14.95 23.23 Peru 12.76 12.68 23.08 Ecuador 3.23 3.23 20.60 Honduras 8.62 8.62 15.26 Colombia 2.56 5.16 10.34 Panama 10.12 Bolivia 1.24 6.39 9.93 Venezuela 4.25 9.41 9.41 WEIGHTED AV. 18.90 29.90 50.44 Source: See the Appendix. Note: Panama is included within Colombia both in 1890 and in 1900. Tables 1 and 2 may be taken as preliminary evidence of the different role that railways performed in the growth of each Latin American economy before 1914. Whereas some countries could benefit from relatively dense networks since an early date, in other cases the expansion of the new infrastructure was extremely slow, and railway systems were scarcely integrated, consisting mainly of a series of isolated lines that connected production areas with the main ports, and hardly affecting large shares of the territory of their countries. In Latin America, railway capital and entrepreneurial initiative came from three different origins: governments, domestic capitalists and foreign firms. The first two sources were relatively important at the beginning of the period, but gradually lost prominence. As a result, by 1899 governments owned just 16 percent and domestic capital 13 percent of the total Latin American railway mileage. Public capital was especially important in some Central American economies and in Chile, although its presence was also significant in the railway systems of Colombia, Brazil and Argentina. In some countries (especially in Central America), public railways, which were largely financed through foreign debt, were used as a substitute for foreign private capital when no foreign direct investment was received. By contrast, in large economies such as Argentina and Chile, they were, to some extent, complementary to private undertakings, being sometimes built in poor and distant regions, as an instrument of political integration and with very low profitability prospects. As for domestic private capital, it was especially present in Cuba (where it owned 40% of the network in 1899, but had 5 controlled almost 100% until the 1880s), Puerto Rico, Brazil and Venezuela (with percentages of 20 to 30% in 1899), and also, to a certain extent, in Chile, and was highly connected with certain export activities, such as Cuban sugar, Brazilian coffee, or Chilean copper mining (Sanz Fernández, 1998). However, by far the largest share of Latin American railway capital came from foreign private investment, which entered the region both in the form of new construction initiatives and through the taking over of public and private domestic firms. The process of privatization of pre-existing public firms was very relevant in some countries, such as Peru, where foreign capital bought a large percentage of public railways in 1890, and it was also important in Argentina and Mexico in the closing years of the 19th century. The relevance of foreign capital increased since the 1880s, specially after the Baring crisis led to the failure of several local initiatives, such that foreign enterprise ended up controlling almost 75% of the railway mileage in 1899, and an even higher percentage (80 to 90%) in the years immediately before 1914. Among foreign investors, British capital was absolutely dominant during the late 19th century, accounting for 70% of foreign railway firms’ mileage in 1899. However, since 1900, the importance of US capital grew rapidly, and it was especially relevant in the US closest area of influence i.e. Mexico, the Caribbean and Central America (Sanz Fernández, 1998). Public subsidies appear to have been a condition for foreign capital to be invested in Latin America. They took different forms, such as guarantees of interest (often at 7% of invested capital), or a fixed amount per mile (as in the cases of Mexico and Honduras). Apparently, when subsidies were absent or were eliminated (such as in Venezuela in 1892), foreign capital disappeared completely. Railway subsidies constituted a huge burden on Latin American countries’ public budgets, and their size (relative to each State’s financial capabilities) often forced governments to renegotiate them, and to look for additional sources of foreign capital in the form of public debt. Latin American railway history has usually associated railway construction waves in each country with both periods of institutional stability and the growth of exports of one or several products of increasing world demand. This might help to explain that, in most countries, significant construction only started in the 1870s, when post-independence political turmoil substantially diminished, while world trade was expanding rapidly. In this regard, the two main exceptions to late construction were Cuba and Chile, which were among the most institutionally stable countries during the post-independence period. Cuba, which remained linked to the Spanish Empire until 1898, was in fact one of the first countries to build railways, starting in 1837, and in Chile construction was very active since the early 1850s. In both cases, primary exports (sugar in Cuba, saltpetre in Chile) were essential to foster construction. The link between railway development and export expansion was extremely strong in the region, as may be seen in Figure 1. The close association between railway density and export density is an obvious sign of the mutual causation between both variables. Railway development allowed the exploitation of natural resources in the inner areas of each country and the subsequent export expansion, whereas export growth increased both state resources and the profitability prospects of private investment. In this context, this work aims at ascertaining if this virtuous circle between railway and export development (and therefore economic growth) was hindered in some 6 countries by factors not directly related to the economic potential of each economy, such as political instability or some sort of financial rationing. In order to do this, in the next section we analyse the determinants of railway density growth across the Latin American countries in the half century before World War One. Figure 1. Railway density and exports density in Latin American economies in 1913. 6 R² = 0,7873 5 ARG Log railway density MEX CUB SLV URY CRI CHL GTM 4 DOM BRA PER NIC ECU HND PAR 3 COL BOL VEN 2 1 2 3 4 Log exports value / surface area (pounds per sq. km) 5 6 Source: See the Appendix. 3. The model In this section we analyse the determinants of railway development in Latin American countries through the estimation of a panel data model of railway mileage expansion. The analysis is based on a rational expectations model of investment in Latin American railways, which assumes that there was an ideal size for each country’s railway network given a vector of geographic, economic, political and financial variables. More specifically, ܻ௧∗ = ߚ + ߚଵ ܺ௧ + ߳௧ (1) where Yt* is the ideal railway density (in logs) and Xt a vector of covariates. In this context, the (public or private) investors would catch up each period with the desired network size. In other words, the growth rate of railway density would be a fraction of the gap between its ideal level and the density of the inherited network: ∗ ܻ௧ − ܻ௧ିଵ = ߜ(ܻ௧ିଵ − ܻ௧ିଵ ) (2) Replacing (2) in (1), we obtain the equation to estimate: 7 ܻ௧ − ܻ௧ିଵ = ߜߚ − ߜܻ௧ିଵ + ߜߚଵ ܺ௧ିଵ + ߜ߳௧ (3) Since we are interested in the coefficients of equation (1) (i.e. the relationships between the covariates and the desired network density level), we may recover them as β1=(δβ1)/δ. Regarding the covariates, here we consider a number of economic, political and financial variables. Among the former, we include population density and several indicators of economic dynamism (exports pc, terms of trade and GDP per capita), which are intended to approach the evolution of the profitability prospects of investment.1 In addition, we also include the effective distance to the European economies, under the assumption that cheaper access to the core markets would have increased the latent demand for transportation in Latin America, to take advantage of the easier access to international trade. Finally, railway density in the neighbouring countries would account for possible “contagion effects” among countries, as well as the possibility that incentives to build new lines increased with the availability of other lines to connect with; and the square lagged dependent variable would account for the possibility that railway network growth slowed down as the saturation point was closer. As for the potential influence of political and institutional variables, we include the incidence of wars, as well as the share of railways that were publicly owned in each year. We consider the first one as representative for the degree of institutional instability. This might have been a deterrent to railway investment, both directly (i.e. through the lower friendliness of the business environment) and indirectly (because of the difficulty to reach consensus on taxes and therefore to finance public subsidies to private railway capital). In order to account for this double link, we also consider the effect of government revenue per capita.2 As for the share of public railways, Bogart (2009) observes, for a different sample of economies, that the fraction of miles nationalised in each country between 1860 and 1912 had a negative effect on mileage growth. This might be related to private investors fear that the government would expropriate their investments, and also to the possibility that governments limited network expansion after nationalisations, in order to increase its own profits from stateowned railways. However, the share of public railways might also be an indicator of the State’s relative fiscal capacity (which might stimulate foreign capital imports), especially in those cases in which public railways were the result of direct State’s investment, rather than nationalisations. Finally, we take into account several potential determinants of financial rationing, such as the number of defaults in the previous years. According to both historical and contemporary evidence, the corporate sector suffers a big penalty from default in terms of lack of access to external finance (Bergquist, 1978; Arteta and Hale, 2008). In addition, some defaults might have been related to the use of public money to subsidize unprofitable railways or even unscrupulous foreign railway promoters, which 1 Investment potential profitability would also be affected by other essentially time-invariant variables, such as construction costs (largely dependent on geography, especially ruggedness), or the presence of alternative cheap transport means (e.g. waterways). We assume these to be accounted for by country fixed effects in the regression. 2 According to Flandreau and Zumer (2004), the main determinant of lending to countries was their ability to repay the debt, which depended in turn on the debt burden per capita. However, data on the volume of debt is very scarce, and in this paper we take the preliminary assumption that the ability to repay the debt was determined by the level of government revenue per capita. 8 would be a deterrent for additional investment. As alternative financial variables, we also include the level of spreads of the sovereign debt, and each country’s adherence to the gold standard. Lagged variables are dated 5 years before the dependent variable, in order to account for the fact that railway construction took a long period to be completed since the time of the investment decision. Table 3 lists the results of the estimation of the model for the whole railway system, and Table 4 presents the same results when the dependent variable is limited to the growth of private railways. The first three columns in each table refer to the baseline model, which only considers the potential economic determinants of railway investment. Each of those columns considers a different indicator of each country’s economic dynamism. Two of them (terms of trade and GDP pc) are only available for a reduced number of countries. Therefore, the results are not totally comparable, since they refer to different samples. Estimates are OLS with country fixed effects, and standard errors are robust to the presence of serial correlation. 9 Table 3. The determinants of railway expansion in Latin American countries (1870-1913) (1) (2) (3) (4) Constant -0.886 -1.245 -5.072*** -1.433** (0.665) (1.225) (0.955) (0.697) Log railway density (t-5) -0.708*** -0.558*** -0.952*** -0.761*** (0.081) (0.132) (0.114) (0.096) Sq. log railway density (t-5) -0.037 -0.026 -0.094*** -0.042* (0.027) (0.033) (0.025) (0.023) Log pop. density (t-5) 0.789** 0.587 1.173*** 0.949*** (0.353) (0.466) (0.280) (0.337) Log exports p.c. (t-5) 0.00001 -0.025 (0.046) (0.045) Terms of trade (t-5) 0.224 (0.183) Log GDP pc (t-5) 0.713*** (0.149) Log eff. distance (t-5) -0.123 -0.171 -0.271** -0.022 (0.171) (0.115) (0.117) (0.166) Log neighbouring countries’ rw density (t-5) 0.009 -0.008 0.184 -0.055 (0.114) (0.151) (0.133) (0.119) No. of years with war (t-5 to t-9) -0.050** (0.020) Share of public railways (t-5) 0.002 (0.002) Log government revenues pc (t-5) No. of defaults (t-5 to t-9) (5) 0.108 (0.542) -0.855*** (0.088) -0.071*** (0.018) 1.263*** (0.254) -0.049 (0.040) (6) -1.239* (0.679) -0.752*** (0.095) -0.042* (0.023) 0.963*** (0.337) -0.049 (0.046) (7) -0.219 (0.365) -0.835*** (0.093) -0.047*** (0.016) 0.844*** (0.250) -0.048 (0.030) (8) -0.701 (0.488) -0.797*** (0.118) -0.028 (0.025) 0.931*** (0.350) -0.046 (0.031) (9) -0.137 (0.340) -0.883*** (0.088) -0.050*** (0.015) 0.871*** (0.245) -0.033 (0.032) -0.099 (0.121) 0.047 (0.093) -0.037** (0.017) 0.0002 (0.002) 0.294*** (0.046) -0.093 (0.166) -0.026 (0.120) -0.046** (0.020) 0.002 (0.002) -0.306*** (0.111) 0.053 (0.083) -0.063*** (0.014) -0.001 (0.002) -0.140 (0.136) 0.035 (0.136) -0.070*** (0.018) 0.003 (0.002) -0.314*** (0.111) 0.038 (0.085) -0.057*** (0.013) -0.003 (0.002) -0.033* (0.019) -0.023 (0.021) Spread (t-5) -0.0001*** -0.0001** (0.00004) (0.00004) Years in gold standard between t-5 and t-9 -0.030 -0.049*** (0.026) (0.018) Time trend 0.021** 0.015 0.008 0.026*** 0.012* 0.021** 0.019*** 0.017** 0.023*** (0.009) (0.010) (0.008) (0.008) (0.007) (0.009) (0.005) (0.008) (0.006) Country fixed effects YES YES YES YES YES YES YES YES YES N 469 348 226 389 347 389 238 269 238 Nº countries included 18 8 9 18 18 18 7 8 7 Adj. R2 0.576 0.558 0.775 0.664 0.706 0.674 0.798 0.780 0.816 Notes: i) Dependent variable: growth in log railway density between t-5 and t; ii) standard errors in brackets. *** Significant at the 1% level; ** Significant at the 5% level; * Significant at the 10% level. 10 Table 4. The determinants of private railway expansion in Latin American countries (1870-1913) (1) (2) (3) (4) (5) Constant -0.937 -1.728* -6.136*** -1.946** -0.334 (0.825) (1.017) (0.949) (0.793) (0.733) Log railway density (t-5) -0.778*** -0.809*** -1.017*** -0.833*** -0.911*** (0.123) (0.135) (0.143) (0.110) (0.113) Sq. log railway density (t-5) -0.066** -0.061** -0.097** -0.049** -0.081*** (0.028) (0.028) (0.038) (0.022) (0.021) Log pop. density (t-5) 1.111*** 1.171*** 1.410*** 1.390*** 1.637*** (0.395) (0.401) (0.362) (0.345) (0.328) Log exports p.c. (t-5) -0.016 -0.065 -0.050 (0.056) (0.048) (0.047) Terms of trade (t-5) 0.262 (0.171) Log GDP pc (t-5) 0.890*** (0.186) Log eff. distance (t-5) -0.224 -0.308 -0.354 -0.247 -0.364* (0.250) (0.235) (0.284) (0.218) (0.188) Log neighbouring countries’ rw density (t-5) 0.010 -0.012 0.239 -0.137 -0.046 (0.106) (0.118) (0.157) (0.120) (0.126) No. of years with war (t-5 to t-9) -0.082*** -0.070*** (0.021) (0.021) Share of public railways (t-5) 0.010*** 0.008*** (0.002) (0.003) Log government revenues pc (t-5) 0.234*** (0.060) No. of defaults (t-5 to t-9) (6) -1.836** (0.773) -0.833*** (0.109) -0.050** (0.022) 1.415*** (0.353) -0.073 (0.049) (7) -0.598 (0.525) -0.887*** (0.121) -0.058*** (0.018) 1.450*** (0.337) -0.078* (0.041) (8) -1.080** (0.501) -0.910*** (0.123) -0.049** (0.019) 1.485*** (0.338) -0.058 (0.036) (9) -0.582 (0.453) -0.938*** (0.118) -0.061*** (0.016) 1.452*** (0.325) -0.056 (0.043) -0.292 (0.212) -0.114 (0.125) -0.080*** (0.021) 0.010*** (0.002) -0.645*** (0.182) -0.065 (0.126) -0.105*** (0.018) 0.011*** (0.002) -0.440*** (0.158) -0.088 (0.139) -0.104*** (0.017) 0.013*** (0.002) -0.604*** (0.187) -0.100 (0.133) -0.098*** (0.015) 0.010*** (0.029) -0.020 (0.023) -0.011 (0.029) Spread (t-5) -0.0001** -0.0001 (0.00004) (0.00005) Years in gold standard between t-5 and t-9 -0.053** -0.067*** (0.025) (0.023) Time trend 0.019* 0.020** -0.0004 0.014* 0.015* 0.023*** 0.015** 0.022*** 0.024*** (0.010) (0.010) (0.012) (0.007) (0.009) (0.009) (0.007) (0.008) (0.008) Country fixed effects YES YES YES YES YES YES YES YES YES N 378 301 213 359 328 365 238 269 238 Nº countries included 18 8 9 18 18 18 7 8 7 Adj. R2 0.546 0.587 0.703 0.671 0.673 0.673 0.743 0.781 0.765 Notes: i) Dependent variable: growth in log railway density between t-5 and t; ii) standard errors in brackets. *** Significant at the 1% level; ** Significant at the 5% level; * Significant at the 10% level. 11 The inherited railway density (Yt-1 in equation 3) is always significant and has the right sign, and the lagged square of railway density also has always a negative (albeit sometimes non-significant) effect on railway density growth, which would be consistent with the gradual deceleration of railway construction as the saturation point is approached. As for the coefficient of population density, it is always positive and significant, except for column (2) of Table 3. By contrast, the economic dynamism indicators are rarely significant. This might indicate that, broadly speaking, railways tended to precede the expansion of the economy rather than the other way around, which is consistent with the idea that the new transport infrastructure was a necessary condition for the extensive exploitation of a large share of the region’s natural resources. Finally, the reduction in the effective distance to the core markets also seems to have stimulated Latin American railway investment throughout the first globalisation, although its coefficient is not significant in many cases. By contrast, we find no sign of a significant contagion effect across countries. Columns 4 to 9 of each table incorporate the political and financial variables. To make the exposition short, we only show the results of the regressions that include exports per capita as the indicator of economic development. However, the outcomes of the estimation using the other two variables are very similar. The results indicate that political instability (approached through the incidence of internal or international wars) was clearly detrimental to railway expansion. As has been indicated, this might reflect both the direct effect of institutional stability and its indirect impact through the difficulty to reach consensus on taxes and therefore to repay the debt and finance public subsidies to private railway capital. In this regard, when government revenue per capita is included in the regression it has a clearly positive and significant effect, and the coefficient of the incidence of wars is reduced. As for the influence of the share of public railways, whereas it seems to have been immaterial for the development of the whole railway network, in Table 4 it appears to have been beneficial from the point of view of the attraction of private investment. This result is not necessarily in contradiction with Bogart (2009). Actually, it might be just the consequence of the relative high importance of public railways in some countries of the region at the beginning of the period under study, and its slow growth or its privatisation as time went by. Therefore, this might not be reflecting the influence of nationalisations on private decision making, but a change in the ownership structure of some railway networks of the region. Finally, columns 6 to 9 present the result of the estimation of the model with some financial variables. The coefficient on the number of previous defaults is negative but rarely significant. By contrast, evidence in favour of the influence of the spreads on sovereign debt over railway investors’ decisions seems to be stronger. And, finally, opposite to what might be expected, each country’s previous adherence to the gold standard appears to have been negative from the viewpoint of railway expansion. In this context, it seems that financial risk would be better captured by spreads, whereas the negative sign of the adherence to gold might be interpreted in terms of the efforts made by each country to belong to the “gold club”. For a not so rich country, these would involve fiscal conservatism, in a context in which the growth of the network until its “ideal” level was dependent on the presence of public subsidies. 12 4. Conclusions This paper provides a very preliminary approach to the potential determinants of railway expansion in Latin American countries. The results are necessarily provisional. The rate of railway density growth seems to have had a non-linear relationship with network mileage, slowing down as this approached its saturation point. In addition, railway density growth was directly related with the demographic evolution of each country, but does not seem to have reacted to changes in exports dynamism, which would be consistent with railways being constructed ahead of demand. On the other hand, we found strong evidence in favour of the influence of institutional instability on railway expansion, both directly and through its effects on each country’s fiscal position. Finally, the results of our analysis indicate that the development of the different railway systems might have been affected by financial rationing, and that railway density growth might have been hindered in those countries with a highest spreads on sovereign debt. Given the importance of railways for the economic development of Latin American countries during the first globalisation boom, this might be taken as preliminary evidence that some of the economies of the region could not fully benefit from the export boom due to the difficulty to access to international capital markets for financing its basic infrastructure. Appendix: data sources Railway data Yearly railway mileage has been taken from Mitchell (2003), except in the following cases: Argentina (from Dirección General de Ferrocarriles, Estadística de los ferrocarriles en explotación, 1892-1913); Chile before 1870 (own estimation from Marín Vicuña, 1901, and Alliende Edwards, 1993); and Uruguay (own estimation from the country’s statistical yearbooks). The length of public railways has been taken from Sanz Fernández (1998); gaps between close or very similar observations have been filled through interpolation. Population and pcGDP Population figures have been taken from recent research by Rivero (2011), who has carried out a critical joint revision of the different available demographic datasets for Latin America (mainly Maddison, 2003; Mitchell, 2003; and the MOxLAD and ECLAC databases); in the case of Bolivia, we have used our own figures (see HerranzLoncán and Peres-Cajías, 2011). GDP per capita comes from Maddison (2003), except in the case of Bolivia (our own data; see Herranz-Loncán and Peres-Cajías, 2011). Effective distance to the core markets We estimated effective distance following Clemens and Williamson (2004)’s procedure, i.e. we coded this variable as the product of a measure of geographic distance and an index of cost of shipping between each country and the main European trading partners. For most countries, geographical distance has been taken as the prePanama canal distance between the main port of each country and London or Hamburg, 13 as listed in Philip (1914). For the majority of nations we have used the index of tramp shipping freight charges from Isserlis (1938: 122), with base year 1869 = 100. Exports, government revenues and exchange rates Foreign trade statistics in local currency were were mainly obtained from Mitchell (2003) with the following exceptions. Brazil from Motta et al. (1990); Chile from Wagner et al. (2000); and Mexico from INEGI (2009) and El Colégio de Mexico (1960). Total government revenue, in local currency units were obtained from Accominotti et al. (2011) for the period 1880-1913. For the earlier period or countries not covered in this database, information was gathered from the following sources. Argentina from Cortes Conde (1989); Brazil from Motta et al. (1990) and several issues of the Brazilian budget laws; Chile from Wagner et al. (2000) and the Sinópsis Estadística (1918); Colombia from Mitchell (2003) and Kalmanovitz (2010); Mexico from El Colégio de Mexico (1960), Wilkie (1967) and Mitchell (2003); Peru from Mitchell (2003) and Tantaléan Arbulú (1983); and Uruguay from Millot and Bertino (1996, 2005) and the Uruguayan Statistical Yearbooks. The majority of the exchange rate (local currency units per pound sterling) data comes from the compilation by Schneider et al. (1911) or Accominotti et al. (2011) with the following exceptions. Argentina from Cortes Conde (1989); Brazil from Motta et al. (1990); Colombia from Ocampo (1984) and the MOxLAD database at http://oxlad.qeh.ox.ac.uk/; Cuba from the MOxLAD database. Terms of trade Given that the UK was by far the main trading partner of Latin American countries throughout the period under analysis, for each country we have used the ratio between a trade-weighted index of commodity export prices and an index of UK export prices, as compiled by Christopher Blattman (see Blattman et al., 2007). Defaults, spreads and adherence to gold standard Defaults were coded from Esteves (2007b) and Suter (1990); spreads over British consols use mostly four sources: Accominotti et al. (2011), Ferguson and Schularick (2006), Esteves (2007b) and Clemens and Williamson (2004); and adherence to gold standard has been taken from Accominotti et al. (2011), Meissner (2005) and Esteves (2007a). Wars The number of internal and international wars that affected each country has been compiled from the Correlates of War database (we have incorporated the independence wars of Cuba and Puerto Rico). References Accominotti, O., M. Flandreau and R. Rezzik (2011) “The Spread of Empire: Clio and the Measurement of Colonial Borrowing Costs,” Economic History Review, 64 (2): 385-407. 14 Alliende Edwards, M. P. (1993), Historia del ferrocarril en Chile, Santiago, Pehuén Editores. Anuario estadístico de la República Oriental del Uruguay, Montevideo: Dirección General de Estadística. Arteta, C.; Hale, G. (2008), “Sovereign debt crises and credit to the private sector”, Journal of International Economics, 74 (1): 53-69. Bergquist, C.W. (1978), Coffee and Conflicts in Colombia, 1886-1910, Duke University Press. Blattman, C.; Hwang, J.; Williamson, J.G. (2007), “Winners and losers in the commodity lottery: The impact of terms of trade growth and volatility in the Periphery 1870–1939”, Journal of Development Economics, 82: 156-179. Bogart, D. (2009), “Nationalizations and the Development of Transport Systems: CrossCountry Evidence from Railroad Networks, 1860–1912”, Journal of Economic History, 69 (1): 202-237. Clemens, M.A. and Williamson, J.G. (2004), “Wealth Bias in the First Global Capital Market Boom, 1870-1913", Economic Journal, 114: 304-37. Coatsworth, J. H. (1979), “Indispensable Railroads in a Backward Economy: The Case of Mexico”, Journal of Economic History, 39 (4): 939-960. Cortes Conde, R. (1989) Dinero, deuda y crisis. Evolución fiscal y monetaria en la Argentina 1862-1890, Buenos Aires: Editorial Sudamericana. Diaz-Alejandro, C. (1984), “Latin America in the 1930s”, in Thorp, R. (ed.), Latin America in the 1930s, London, Macmillan. El Colegio de México (1960) Estadísticas economicas del Porfiriato. Comercio Exterior de Mexico 1877-1911, Mexico City. Esteves, R. (2007a) “Between Imperialism and Capitalism. European Capital Exports Before 1914,” University of Oxford, Mimeo. Esteves, R. (2007b) “Quis custodiet quem? Sovereign Debt and Bondholders’ Protection Before 1914,” University of Oxford, Department of Economics Working Paper no. 323. Flandreau, M. and Zumer, F. (2004), The Making of Global Finance, 1880-1913, Paris, OECD. Ferguson, N. and M. Schularick (2006) “The Empire Effect: The Determinants of Country Risk in the First Age of Globalization, 1880–1913,” Journal of Economic History, 66(2): 283-312. Haber, Stephen, ed. (1997), How Latin America fell behind: essays on the economic histories of Brazil and Mexico, 1800-1914, Stanford: Stanford University Press. Herranz-Loncán, A. (2011), “El impacto directo del ferrocarril sobre el crecimiento económico argentino durante la Primera Globalización”, Revista Uruguaya de Historia Económica, 1 (1): 34-52. Herranz-Loncán, A. (forthcoming), “The Role of Railways in Export-Led Growth: the Case of Uruguay, 1870-1913”, Economic History in Developing Regions. Herranz-Loncán, A. and Peres-Cajías, J.A. (2011), “La economía boliviana en el muy largo plazo: una aproximación preliminar al crecimiento económico de Bolivia desde la independencia”, paper presented at the V Jornadas Uruguayas de Historia Económica, Montevideo, nov. 2011. INEGI (2009) Estadisticas históricas de México, 5th edition, 2 v. Mexico City: Instituto Nacional de Estadística y Geografía. Isserlis, L. (1938), “Tramp Shipping Cargoes, and Freights,” Journal of the Royal Statistical Society, 101(1): 53-146. Kalmanovitz, S., ed. (2010) Nueva Historia Económica de Colombia, Bogotá: Taurus. 15 Maddison, A. (2003), The World Economy. Historical Statistics, Paris, OECD. Marichal, Carlos (1989), A Century of Debt Crises in Latin America. From Independence to the Great Depression, 1820-1930, Princeton: Princeton University Press. Marín Vicuña, S. (1901), Estudios de los ferrocarriles chilenos, Santiago, Imprenta Cervantes. Meissner, C. (2005) "A New World Order: Explaining The International Diffusion Of The Gold Standard, 1870-1913," Journal of International Economics, 66 (2): 385-406. Millot, J. And M. Bertino, eds. (1996) Historia económica del Uruguay. Volume II 1860-1910, Montevideo : Fundación de Cultura Universitaria. Millot, J. And M. Bertino, eds. (2005) Historia económica del Uruguay. Volume III 1910-1930, Montevideo : Fundación de Cultura Universitaria. Mitchell, B.R. (2003), International Historical Statistics: The Americas, 1750-2000, Houndmills, Palgrave. Motta, R. da, F. Versiani and W. Suzigan, eds. (1990) Estatísticas Históricas do Brasil. Séries econômicas, demográficas e sociais de 1520 a 1988. 2ª edição revista e atualizada, Rio de Janeiro: Instituto Brasileiro de Geografia e Estatística. Ocampo, J. (1984) Colombia y la economía mundial, 1830-1910, Bogotá: Siglo XXI. Philip, G. (1914), Philip’s Mercantile Maritime Atlas, London, The London Geographical Institute, 4th ed. Ramírez, M. T. (2001), “Los ferrocarriles y su impacto sobre la economía colombiana”, Revista de Historia Económica, 19 (1): 81-122. Rivero, R. (2011), “La población de los países latinoamericanos en los siglos XIX y XX”, unpublished MSc Thesis. Sanz Fernández, J. (coord.) (1998), Historia de los ferrocarriles de Iberoamérica (1837-1995), Madrid, Ministerio de Fomento. Schneider, J., O. Schwarzer, and M. Denzel (1991) Währungen der Welt, Stuttgart: Franz Steiner Verlag, 11 vols. Sinópsis Estadística de la República de Chile, Santiago: Oficina Central de Estadística, 1918. Summerhill, W. (2000), “Profit and Productivity on Argentine Railroads, 1857-1913”, Los Angeles, UCLA, Department of History, UCLA (mimeo). Summerhill, W. (2003), Order Against Progress. Government, Foreign Investment, and Railroads in Brazil, 1854-1913, Stanford, Stanford University Press. Summerhill, William R. (2006), “The Development of Infrastructure”, in BulmerThomas, Victor; Coatsworth, John and Cortés Conde, Roberto (eds.), The Cambridge Economic History of Latin America. Vol. 2: The Long Twentieth Century, Cambridge, Cambridge University Press, pp. 293-326. Suter, C. (1990) Schuldenzyklen in der Dritten Welt : Kreditaufnahme, Zahlungskrisen und Schuldenregelungen peripherer Länder im Weltsystem von 1820 bis 1986, Frankfurt/ Main: A. Hain. Tantaléan Arbulú, J. (1983) Política económico-financiera y la formación del estado, siglo XIX, Lima: Centro de Estudios para el Desarrollo y la Participación. Wagner, G., J. Jofré and R. Lüders (2000) "Economía Chilena 1810-1995. Cuentas Fiscales," Pontificia Universidad Catolica de Chile, Instituto de Economia: Documento de Trabajo no. 188. Wilkie, J. (1967) The Mexican Revolution: Federal Expenditure and Social Change Since 1910, Berkeley: University of California Press. 16