Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

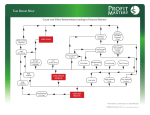

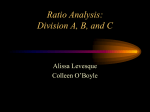

Buying a Business Chapter 5 Why acquire an existing business? • Growing your business internally can be a sluggish and high-risk strategy • Buying an existing business eliminates many of the headaches involved in getting a start-up off the ground, such as developing products, hiring the right people and building a sound customer base. • Buying a business also gives entrepreneurs a jump on the start-up phase — a time when many new businesses fail. Often, it's the only feasible way to break into a particular field, such as tourism or manufacturing, since start-up costs in these sectors can be prohibitive. Advantages • established customer base • business has been fully tried and tested • The inventories in an established business and the profitability of its product line can alert you to what works well and what needs to be improved • Workers who have been with the company for some time can provide insights into the business and industry as a whole. • A proven track record and existing cash flow make it easier to obtain additional financing • business plan and records are already in place See: http://www.bdc.ca/en/advice_centre/articles/ pages/acquisition_business_why.aspx Disadvantages • The business might need major improvements to old plant and equipment. • You often need to invest a large amount up front, and will also have to budget for professional fees for solicitors and accountants. • The business may be poorly located or badly managed, with low staff morale. • External factors, such as increasing competition or a declining industry, can affect future growth. • Under-performing businesses can require a lot of investment to make them profitable Tips When Buying • • • • • • • • • Stay in the area you know Look for the right fit Determine through research whether this type of business has a solid chance of turning a profit. If your goal is to acquire a firm to add to an existing business, you will need synergy in key areas.. Look at the firm's identity Consider the company's culture Evaluate the costs Financial records may not always reflect reality. You need to ensure that the price is in line with market conditions. Determine whether the equipment is part of the sale. If so, what condition is it in and what is it worth? Is the building for sale as well? If it is rented, can you take over the lease, and under what conditions? Don't limit yourself to examining operations and facilities or going through financial statements. You also need to investigate the parts of the business that you can't see physically by talking to employees and suppliers. Assessing the Value • Financial Factors • Ratio Analysis – – – – – – – – Quick Ratio Current Ratio Debt – to – worth Gross Margin Profit Margin Return on Assets Inventory Turnover Ratio Collection Period The Quick Ratio (Acid Test Ratio) The Quick Ratio is an indicator of a company’s short-term liquidity. The quick ratio measures a company’s ability to meet its short-term obligations with its most liquid assets. For this reason, the ratio excludes inventories from current assets, and is calculated as follows: Quick ratio = (Current assets – Inventories) / Current liabilities or (Cash and equivalents + marketable securities + accounts receivable) / current liabilities The quick ratio measures the dollar amount of liquid assets available for each dollar of current liabilities. Thus, a quick ratio of 1.5 means that a company has $1.50 of liquid assets available to cover each $1 of current liabilities. The higher the quick ratio, the better the company's liquidity position. Current Ratio • The Current ratio is mainly used to give an idea of the company's ability to pay back its short-term liabilities (debt and payables) with its short-term assets (cash, inventory, receivables). The Current ratio is a liquidity ratio that measures a company's ability to pay short-term obligations. The Current Ratio formula is: Current Assets/Current Liabilities • The higher the current ratio, the more capable the company is of paying its obligations. A ratio under 1 suggests that the company would be unable to pay off its obligations if they came due at that point. While this shows the company is not in good financial health, it does not necessarily mean that it will go bankrupt - as there are many ways to access financing - but it is definitely not a good sign. The current ratio can give a sense of the efficiency of a company's operating cycle or its ability to turn its product into cash. Companies that have trouble getting paid on their receivables or have long inventory turnover can run into liquidity problems because they are unable to alleviate their obligations. Because business operations differ in each industry, it is always more useful to compare companies within the same industry. This ratio is similar to the acid-test ratio except that the acid-test ratio does not include inventory and prepaids as assets that can be liquidated. Debt to Worth • The Debt ratio is a financial ratio that measures the extent of a company’s leverage. The debt ratio is defined as the ratio of total debt to total assets, expressed in percentage, and can be interpreted as the proportion of a company’s assets that are financed by debt. • • Debt Ratio = Total Debt / Total Assets The higher this ratio, the more leveraged the company and the greater its financial risk. Debt ratios vary widely across industries, with capital-intensive businesses such as utilities and pipelines having much higher debt ratios than other industries like technology. In the consumer lending and mortgage businesses, debt ratio is defined as the ratio of total debt service obligations to gross annual income. Gross Margin • • • Gross Margin is a company's total sales revenue minus its cost of goods sold, divided by the total sales revenue, expressed as a percentage. The gross margin represents the percent of total sales revenue that the company retains after incurring the direct costs associated with producing the goods and services sold by a company. The higher the percentage, the more the company retains on each dollar of sales to service its other costs and obligations. • • Gross Margin(%) = (Revenue – COGS) / Revenue This number represents the proportion of each dollar of revenue that the company retains as gross profit. For example, if a company's gross margin for the most recent quarter was 35%, it would retain $0.35 from each dollar of revenue generated, to be put towards paying off selling, general and administrative expenses, interest expenses and distributions to shareholders. Profit Margin • Profit Margin is the ratio of profitability calculated as net income divided by revenues, or net profits divided by sales. It measures how much out of every dollar of sales a company actually keeps in earnings. Profit Margin = Net Profit/Sales • Profit margin is very useful when comparing companies in similar industries. A higher profit margin indicates a more profitable company that has better control over its costs compared to its competitors. Profit margin is displayed as a percentage; a 20\% profit margin, for example, means the company has a net income of $0.20 for each dollar of sales. Return on Assets • Return on Assets is an indicator of how profitable a company is relative to its total assets. • ROA gives an idea as to how efficient management is at using its assets to generate earnings. Calculated by dividing a company's annual earnings by its total assets, ROA is displayed as a percentage. Sometimes this is referred to as "return on investment". • • The formula for return on assets is: • ROA = Net Income / Total Assets Inventory Turnover Ratio Inventory turnover refers to how often inventory is sold (turned over) and replaced by the firm in a period of time. A quick turnover is desired because it means that inventory is not sitting on the shelves for too long. The days in the period can then be divided by the inventory turnover formula to calculate the days it takes to sell the inventory on hand or "inventory turnover days." Inventory Turnover = Sales/Average Inventory Average Collection Period • The approximate amount of time that it takes for a business to receive payments owed, in terms of receivables, from its customers and clients. Calculated as: • ACP = (Days * AR) / Credit Sales Where: Days = Total amount of days in period AR = Average amount of accounts receivables Credit Sales = Total amount of net credit sales during period