Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

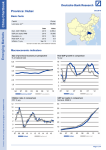

Uganda Frontier country report | August 16, 2013 Key strengths Low GDP per capita 1 9 8 7 6 5 4 3 2 1 0 700 600 500 Good growth prospects. Currently subdued relative to the past due to stagnating public spending and weak external demand, GDP growth is expected to pick up in the coming years on the back of infrastructure investments and newfound oil (production could start in 2016). Investment is pouring into the nascent oil industry. The main source of employment remains agriculture (traditional cash crops and subsistence agriculture). 400 300 200 100 Moderate public and external debts. At around 35% of GDP, public debt is relatively low, although growing. At 23%, external debt is low, too. International reserves are growing rapidly (currently at over 4 months of import cover). Sharp fall in inflation. Inflation has come down from a peak of over 30% in October 2011 to close to 5%, which is the government’s target level. Price pressures are expected to remain low, although a drought would increase food prices, which account for over a quarter of the CPI. 0 2008 2009 2010 2011 2012 2013 2014 GDP growth, % (left) GDP per capita, USD (right) Source: IMF Key weaknesses Twin deficits 2 % of GDP 0 0 -1 -2 -2 -4 -3 -6 -4 -8 -5 -10 -6 -12 -7 -14 -8 -16 2008 2009 2010 2011 2012 2013 2014 Fiscal balance (left) C/A balance (right) Source: IMF Low level of economic development. Although growth has driven a decrease in poverty (to 15% of the population in 2012 from 55% in 1993 ), Uganda’s GDP per capita (at around USD 580) is one of the lowest in the world. Rapid population growth remains a challenge: at above 6 children per woman, the total fertility rate is among the highest in the world. Infrastructure deficiencies are significant. Poor governance. Governance and doing business indicators remain low for Uganda. Weak bureaucracy, corruption and a lack of political transparency hinder Uganda’s development as a democracy. President Museveni, in power since 1986, remains politically dominant. Given that he enjoys the full support of the security forces (and due to a poorly organised political opposition), political stability is expected to continue. Heavy dependence on donors, currently strained relations. The government adopted policies that contributed to reducing the fiscal deficit (currently 3%) but the deficit is expected to widen in the lead-up to the 2016 elections. Alleged misappropriation of aid funds resulted in the suspension of support from several donors in late 2012. This has put pressure on the state’s finances and the uncertain outlook for aid underpins the government’s budget framework paper for 2013/14. (Aid is budgeted at 3.7% of GDP down from 5% of GDP in 2012/13, it typically accounts for around 25-35% of government revenue). The agreement between the IMF and Uganda in May 2013 on a successor policy support instrument (PSI) may persuade donors to reintroduce some support over time. (Priorities of the new PSI are improving public financial management and refining the inflation-targeting framework. It will also likely contribute to improving the business environment). Wide current account deficit. Currently at 13% of GDP, the current account deficit is expected to remain wide due to high import growth (oil, capital goods and consumer goods) while coffee remains the main export. The CA deficit is likely to remain high until oil production starts. Global Risk Analysis Contact Claire Schaffnit-Chatterjee | [email protected] | +49 69 910-31821 Internet http://www.dbresearch.com Uganda © Copyright 2013. Deutsche Bank AG, DB Research, 60262 Frankfurt am Main, Germany. All rights reserved. When quoting please cite “Deutsche Bank Research”. The above information does not constitute the provision of investment, legal or tax advice. Any views expressed reflect the current views of the author, which do not necessarily correspond to the opinions of Deutsche Bank AG or its affiliates. Opinions expressed may change without notice. Opinions expressed may differ from views set out in other documents, including research, published by Deutsche Bank. The above information is provided for informational purposes only and without any obligation, whether contractual or otherwise. No warranty or representation is made as to the correctness, completeness and accuracy of the information given or the assessments made. In Germany this information is approved and/or communicated by Deutsche Bank AG Frankfurt, authorised by Bundesanstalt für Finanzdienstleistungsaufsicht. In the United Kingdom this information is approved and/or communicated by Deutsche Bank AG London, a member of the London Stock Exchange regulated by the Financial Services Authority for the conduct of investment business in the UK. This information is distributed in Hong Kong by Deutsche Bank AG, Hong Kong Branch, in Korea by Deutsche Securities Korea Co. and in Singapore by Deutsche Bank AG, Singapore Branch. In Japan this information is approved and/or distributed by Deutsche Securities Limited, Tokyo Branch. In Australia, retail clients should obtain a copy of a Product Disclosure Statement (PDS) relating to any financial product referred to in this report and consider the PDS before making any decision about whether to acquire the product. 2 | August 16, 2013 Frontier country report