Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

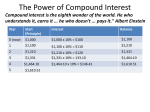

Agribusiness Library LESSON L060013: THE TIME VALUE OF MONEY Objectives 1. Describe the time value of money. 2. Explain the concepts of simple and compound interest. 3. Explain the concept of discounting. Terms •Compound interest •Compounding •Discounting •Inflation •Interest rate •Principal •Risk •Simple interest •Time value of money The time value of money states that a dollar (or other unit of currency) has a greater value at the present time than the same amount of money at a future time because of the interest that can be gained by investing the money. A. An interest rate is the amount of money that will be paid to an investor for allowing an institution to use the money for a set period of time. Normally, the longer the institution uses the money, the higher the interest rate, which serves as the mechanism for comparing the time value of money. B. The interest rate is considered the exchange price between the current and future value of the dollar. In other words, interest rates show the difference in what the dollar is worth now and what it will be worth (with the interest it earns) in the future. C. Interest rates represent risk and inflation. The greater the investment risk, the larger the interest rate paid out on the investment. 1. Risk is the amount of uncertainty in the investment and its future growth. 2. Interest rates also reflect the amount of inflation —the rise of the price of goods and services in our economy. Banks that loan money to individuals charge interest on the loans. More people are likely to borrow and spend money when interest rates are low, so they are not charged as much to borrow the money. D. Interest is paid to individuals in return for putting money in savings accounts or other investments. The interest rates vary from institution to institution and can change in response to factors in the economy. As defined previously, interest is the charge (or payment) for using an amount of money for a set period of time. There are many ways that banks and investment organizations calculate interest on investments, but two of the most common methods are simple and compound interest. A. Simple interest is the amount earned over the life of the investment on the original principal —the amount of money invested that is earning interest. 1. To determine the amount of money earned through simple interest, the following equation can be used: FV = PV + n(PV × i). FV = future value, PV = present value, n = number of conversion periods, and i = interest rate. 2. For example, using simple interest, $1,000 invested today with an interest rate of 5 percent for 10 years would yield: FV = 1,000 + 10(1,000 × 0.05) FV = 1,000 + 10(50) FV = 1,000 + 500 FV = $1,500 B. Compound interest is earned interest that is added to the principal, which then earns more interest as a larger amount. As the amount of principal increases, the earning power and the interest payments also increase. Compounding is the process of calculating the value of money at some future time. 1. To determine the amount of money earned through compound interest, the following equation can be used: 2. For example, if farmland has been selling for $2,000 per acre, what can you expect it to sell for in 25 years if it increases in value at an annual rate of 3 percent? FV = PV(1 + i)n. FV = future value, PV = present value, n = number of conversion periods, and i = interest rate. FV = 2,000(1 + 0.03)25 FV = 2,000(1.03) 25 FV = 2,000(2.094) FV = $4,188 per acre 3. Compounding can be used to determine salaries or the price of an item, assuming a given annual increase in value. While compounding calculates the future value of money in an individual’s possession currently, discounting calculates the present value of money that is received in the future. A. The discount is a result of the investor waiting to receive the future payment rather than receiving it now and investing it in an alternative way. B. To determine the present value of money earned in the future, the following equation can be used: PV = FV/(1 + i)n. 1. For instance: If farmland has been selling for $2,000 per acre and has been increasing at the rate of 5 percent per year, what was its price six years ago? Answer: PV = 2,000/(1 + 0.05)6 PV = 2,000/(1.05)6 PV = 2,000/(1.34) PV = $1,492 per acre 2. Another example using discounting is to calculate the amount of principal needed presently to reach a target amount at some point in the future. Assume an individual wants to have $50,000 in 15 years. Using an investment with an interest rate of 6 percent, how much would need to be invested today to reach the goal? Answer: PV = 50,000/(1 + 0.06)15 PV = 50,000/(1.06)15 PV = 50,000/(2.396) PV = $20,868 (needed presently to invest) REVIEW •What is the time value of money? •What is simple interest, and what is compound interest? •What is discounting?