Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

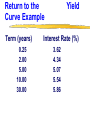

The Yield Curve Yield Curve (Term Structure of Interest Rates): A plot of the interest rates of Treasury Bills and Treasury Bonds versus their maturities at a point in time. Yield Curve: An Example Term (years) 0.25 2.00 5.00 10.00 30.00 Interest Rate (%) 3.62 4.34 5.07 5.54 5.86 The Slope of the Yield Curve Upward Sloping (Term i) -- usual case. Downward Sloping (or Inverted) Yield Curve (Term i) -- occurs periodically What information can we get from the yield curve? Observed Phenomena -Yield Curve The downward sloping (inverted) yield curve is unusual but not rare. Interest rates of bonds of all maturities move together (are positively correlated) The downward sloping (inverted) yield curve tends to occur when interest rates in general are high. Theories (Hypotheses) Which Explain Yield Curve Behavior Key difference in assumptions: How close of substitutes are bonds of different maturities? We will assess each hypothesis – how well does it predict the three observed phenomena? (1) Expectations Hypothesis The Expectations Hypothesis -- The interest rate on a long-term bond will be equal to the average of short-term rates expected to occur over the lifetime of the long-term bond. Key assumption: Bonds of different maturities are perfect substitutes. Assessment: Expectations Hypothesis The downward sloping (inverted) yield curve is unusual but not rare. Fails to predict this occurrence. (predicts 50-50 probability of upward versus downward slope) Expectations Hypothesis Interest rates of bonds of all maturities move together (are positively correlated) Accurately predicts this occurrence. (bonds are substitutes) Expectations Hypothesis The downward sloping (inverted) yield curve tends to occur when interest rates in general are high. Accurately predicts this occurrence (When are interest rates expected to decrease?) (2) The Market Segmentation Hypothesis The Market Segmentation Hypothesis -- Each investor has his/her preferred maturity sector and stays within it. Consequently, interest rates on bonds are determined by independent demand and supply conditions within that sector. Market Segmentation Hypothesis: Assumption Key Assumption: Bonds of different maturities are not substitutes at all. Market Segmentation Hypothesis: Predictions Upward sloping yield curve is the usual case -- more demand for short-term bonds than long-term bonds. Downward sloping yield curve -contractionary Federal Reserve policy, increases short-term rates without affecting long-term rates. Assessment: Market Segmentation Hypothesis The downward sloping (inverted) yield curve is unusual but not rare. Accurately predicts this occurrence. (Highly contractionary monetary policy) Market Segmentation Hypothesis Interest rates of bonds of all maturities move together (are positively correlated) Fails to predict this occurrence. (Independently determined interest rates should not move together) Market Segmentation Hypothesis The downward sloping (inverted) yield curve tends to occur when interest rates in general are high. Accurately predicts occurrence. (High expected inflation, contractionary monetary policy) (3) The Preferred Habitat Hypothesis The Preferred Habitat Hypothesis The interest rate on a long-term bond equals the average of shortterm rates expected to occur over the lifetime of the long-term bond plus a risk premium due to higher market risk in the long-term bond. Preferred Habitat Hypothesis: Assumption Key assumption -- Bonds of different maturities are close substitutes but not perfect substitutes. Major non-price difference -longer term bonds have higher market risk. Assessment: Preferred Habitat Hypothesis The downward sloping (inverted) yield curve is unusual but not rare. Accurately predicts occurrence. (Investors must expect interest rates to decrease a lot in the future.) Preferred Habitat Hypothesis Interest rates of bonds of all maturities move together (are positively correlated) Accurately predicts this occurrence. (Close substitutes) Preferred Habitat Hypothesis The downward sloping (inverted) yield curve tends to occur when interest rates in general are high. Accurately predicts occurrence (When are interest rates expected to decrease a lot?) Intepretations of a Yield Curve Different theories attach different interpretations based on assumptions Return to the Curve Example Term (years) 0.25 2.00 5.00 10.00 30.00 Yield Interest Rate (%) 3.62 4.34 5.07 5.54 5.86 Interpretations of Yield Curve from Example Expectations Hypothesis – investors expect interest rates to increase. Market Segmentation Hypothesis – normal bond market conditions. Preferred Habitat Hypothesis – investors expect interest rates in the future to either increase, say level, or decrease by a small amount. The Yield Curve: Additional Topics The U-Shaped (or J-Shaped) Yield Curve: different interpretations depending upon underlying hypothesis. Is the inverted Yield Curve a good predictor for recessions in the overall economy?