Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

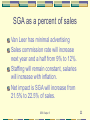

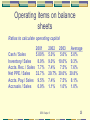

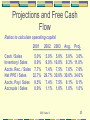

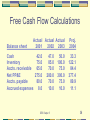

DES Chapter 5 Projecting Free Cash Flows DES Chapter 5 1 Objective Chapter 4 assumed you already had projected financial statements. In this chapter, you will construct projected financial statements. DES Chapter 5 2 Why project financial statements? Forces you to articulate your assumptions Helps you understand your firm’s value drivers Requires you to verify that your assumptions are economically reasonable Identifies external funding needed Provides data needed to project FCF and perform a valuation DES Chapter 5 3 What are the characteristics of a good forecast? Economic plausibility The statements must reflect how the firm might realistically operate in the future. Accounting consistency Do the financial statements balance? Do they “articulate?” Are they a good model of the firm’s finances? DES Chapter 5 4 Van Leer Products, Inc. Manufactures extruded plastic products. Statements are just a bit different from Acme's: They have short term investments—this is where Van Leer “parks” its excess cash. They have only net PPE. Gross PPE has been omitted. This is because many companies only report Net PPE. DES Chapter 5 5 Modeling the financial statements Operating accounts that vary directly with sales Cost of goods sold (COGS) For most firms, COGS is pretty close to proportional to sales Selling, general and administrative expenses (SGA) Although in the 1-2 year range, SGA may not be directly proportional, for most firms it is roughly proportional over our longer projection periods 6 DES Chapter 5 Operating accounts that vary directly with sales Cash We will consider only that level of cash necessary to “grease the wheels” of the company’s operations. This amount is required to keep checks from bouncing. Inventory Clearly inventory must increase with sales—this chapter assumes it is proportional to sales. DES Chapter 5 7 Operating accounts that vary directly with sales Accounts receivable Most firms must have more AR if they sell more. Net PPE In the short run, like SGA, net PPE may not be directly related to sales, but over the longer run, most firms’ net PPE is pretty closely related to sales. DES Chapter 5 8 Accounts that vary directly with sales Accounts payable If you sell more, then you produce more and use more materials. Your credit purchases will increase with sales. Accrued expenses If you sell more, then labor expense and payroll taxes due will be higher—these will also increase with sales. DES Chapter 5 9 Operating accounts that vary with other things Depreciation charges are set by the depreciation schedule—in general they will depend on net PPE, not directly on sales. DES Chapter 5 10 Modeling items required for projecting FCF You don’t need the entire statements to calculate FCF—start with what is necessary for FCF and then add the rest of the statements so we can calculate the funding mix Need operating income Need investment in operating capital DES Chapter 5 11 Projecting partial financial statements Income statement Net sales Cost of goods sold SGA Depreciation Operating profit DES Chapter 5 Forecast method Forecast growth Percent of sales Percent of sales Percent net PPE Calculated 12 Projecting partial financial statements Balance Sheet Cash Inventory Accounts receivable Net PPE Accounts payable Accrued expenses DES Chapter 5 Forecast method Percent of sales Percent of sales Percent of sales Percent of sales Percent of sales Percent of sales 13 Information about Van Leer The analysis uses some information about Van Leer that won’t come from the 10k or annual report. The analyst may have access to it as a corporate “insider” performing this valuation for internal purposes. If the analyst is an “outsider” then some of this information would have to come from extensive research on the company and industry. DES Chapter 5 14 Van Leer Products, Inc. Van Leer Products, Inc. Actual Actual Actual Income Statement 2001 2002 2003 Net Sales 840 944 1,000 Cost Of Goods Sold 520 625 640 Selling, general & administrative 200 205 215 Depreciation 41 42 45 Operating profit 79 72 100 Interest income 0 1 0 Interest expense 9 9 10 Earnings before taxes 70 64 90 Taxes 28 25 36 Net income 42 39 54 Dividends 12 11 16 Additions to RE 30 28 38 15 DES Chapter 5 Van Leer Products, Inc. Actual Actual Actual 2001 2002 2003 Balance sheet Cash 42 47 50 Short-term investments 10 15 25 Inventory 75 85 100 Accounts receivable 65 70 75 Total current assets 192 217 250 Net PP&E 275 280 300 Total assets 467 497 550 DES Chapter 5 16 Van Leer Products, Inc. Actual Actual Actual 2001 2002 2003 Balance sheet Accounts payable 80 70 75 Accrued expenses 8 10 10 Short-term debt 50 30 25 Total current liabilities 138 110 110 Long-term debt 54 84 99 Total liabilities 192 194 209 125 125 125 Common stock Retained earnings 150 178 216 Total common equity 275 303 341 Total liabilities and equity 467 497 550 DES Chapter 5 17 Choosing inputs for the model Projecting the sales growth rate Projecting operating profit Projecting operating capital Projecting taxes DES Chapter 5 18 Historical ratios used to project free cash flows Ratios to calculate operating profit 2002 12.4% 66.2% 21.7% 2003 5.9% 64.0% 21.5% Average 9.2% 64.0% 22.3% 14.9% 15.0% 15.0% 15.0% Tax rate (Taxes/EBT) 40.0% 39.1% 40.0% 39.7% Sales growth rate COGS / Sales SGA / Sales Depreciation / Net PPE 2001 na 61.9% 23.8% DES Chapter 5 19 How to think about projected sales growth rate for 2004 9.2% average growth rate over the past two years Economy is predicted to recover substantially by 2004, so the analyst predicts more rapid growth than in 2003, and more rapid than the average. After speaking with marketing and operations, the analyst predicts that Van Leer’s sales will increase by 9% next year due to increased unit sales, and by 2% due to anticipated inflation. Dollar sales therefore are projected to increase by a total of 11% from $1,000 to $1,110. DES Chapter 5 20 How to think about COGS as a percent of sales Higher COGS comes from higher production costs or lower sales price, or both. Lower COGS comes from cost containment with stable prices, or higher prices with stable costs, or both. Marketing predicts COGS will decrease from last year’s 64% to 62.5% of sales. DES Chapter 5 21 SGA as a percent of sales Van Leer has minimal advertising Sales commission rate will increase next year and a half from 9% to 12%. Staffing will remain constant, salaries will increase with inflation. Net impact is SGA will increase from 21.5% to 22.5% of sales. DES Chapter 5 22 Depreciation Depreciation schedule is set by the cost of the assets purchased and accounting rules. Overall this will change dramatically only if a company changes the type (long-term or short-term) of assets it is purchasing. Van Leer will continue using the same type of assets it has been using, so depreciation will remain at 15% of net PPE. DES Chapter 5 23 Tax rate Combined federal, state and local taxes are 39.7% of sales, and are expected to remain the same. DES Chapter 5 24 Operating items on balance sheets Ratios to calculate operating capital 2001 Cash / Sales 5.00% Inventory/ Sales 8.9% Accts. Rec. / Sales 7.7% Net PPE / Sales 32.7% Accts. Pay./ Sales 9.5% Accruals / Sales 0.9% 2002 2003 Average 5.0% 5.0% 5.0% 9.0% 10.0% 9.3% 7.4% 7.5% 7.6% 29.7% 30.0% 30.8% 7.4% 7.5% 8.1% 1.1% 1.0% 1.0% DES Chapter 5 25 Projecting operating items on the balance sheet Cash: This is the minimum cash balance required for the business to function. Has been 5% historically. Expects to drop to 3% with better information technology. DES Chapter 5 26 Operating items Accounts Receivable Depend on credit policy: Tighter policy means less accounts receivable, but also fewer sales. Looser policy means more sales, but more accounts receivable and more bad debt writeoffs. Averaged 7.6% over last 3 years. Plans to maintain same credit policy, so the percent should remain the same. DES Chapter 5 27 Operating items Inventories Higher inventory means more investment, but lower chance of a stockout. Lower inventory may increase chance of missed sales. Averaged 9% of sales. Expects to stock up in 2004 to support the projected summer recovery, so will be 11% of sales. DES Chapter 5 28 Operating items Net PPE as a % of sales This ratio will decrease as the firm uses up capacity, and will be large just after building a plant and operating at under-full capacity. Also changes as the firm alters its technology. Van Leer must invest in another plant in 2004, so PPE will increase to 34% of sales. PPE as % of sales will decrease as it grows into its new facilities. DES Chapter 5 29 Operating items Accounts payable Increasing AP means paying later, decreasing means paying earlier. Payables deferral period = AP/(COGS/365) Has been 45.6 days. This corresponds to accounts payable of 8.1% of sales. Van Leer will maintain this policy. DES Chapter 5 30 Operating items Accruals Arise from lag in reporting payroll taxes due, and actually paying the taxes. Payment schedule is set by the various government entities, so Van Leer can’t change it very much. Has been 1%, and Van Leer expects it to remain at 1%. DES Chapter 5 31 Projections and Free Cash Flow Ratios to calculate operating profit 2001 2002 2003 Avg. Proj. Sales growth rate na 9.2% 11.0% 12.4% 5.9% COGS / Sales 61.9% 66.2% 64.0% 64.0% 62.5% SGA / Sales 23.8% 21.7% 21.5% 22.3% 22.5% Depreciation / Net PPE 14.9% 15.0% 15.0% 15.0% 15.0% DES Chapter 5 32 Projections and Free Cash Flow Ratios to calculate operating capital 2001 2002 2003 Avg. Proj. Cash / Sales 5.0% 5.0% 5.0% 5.0% 3.0% Inventory/ Sales 8.9% 9.0% 10.0% 9.3% 11.0% Accts. Rec. / Sales 7.7% 7.4% 7.5% 7.6% 7.6% Net PPE / Sales 32.7% 29.7% 30.0% 30.8% 34.0% Accts. Pay./ Sales 9.5% 7.4% 7.5% 8.1% 8.1% Accruals / Sales 0.9% 1.1% 1.0% 1.0% 1.0% DES Chapter 5 33 Projections and Free Cash Flow Ratios to calculate operating taxes Tax Rate (Taxes/EBT) 2001 2002 40.0% 39.1% 40.0% DES Chapter 5 2003 Avg. Proj. 39.7% 39.7% 34 Free Cash Flow Calculations Van Leer Products, Inc. Actual Actual Actual Projected Income Statement 2001 2002 2003 2004 Net Sales 840.0 CGS 520.0 Selling, general & administrative 200.0 Depreciation 41.0 Operating profit 79.0 944.0 1000.0 625.0 640.0 1110.0 693.8 205.0 42.0 215.0 45.0 249.8 56.6 72.0 100.0 109.9 DES Chapter 5 35 Free Cash Flow Calculations Balance sheet Actual Actual Actual 2001 2002 2003 Cash 42.0 Inventory 75.0 Accts. receivable 65.0 Net PP&E 275.0 Accts. payable 80.0 Accrued expenses 8.0 47.0 85.0 70.0 280.0 70.0 10.0 DES Chapter 5 50.0 100.0 75.0 300.0 75.0 10.0 Proj. 2004 33.3 122.1 84.4 377.4 89.9 11.1 36 Operating Income Tax on Operating Income (40%) NOPAT Net Operating WC Net Operating Long Term Assets Total Net Operating Assets Investment in net operating assets Free Cash Flow ROIC Actual 2001 Actual 2002 Actual 2003 Proj. 2004 79.0 72.0 100.0 109.9 31.6 47.4 94.0 28.1 43.9 122.0 40.0 60.0 140.0 43.6 66.3 138.8 275.0 280.0 300.0 377.4 369.0 402.0 440.0 516.2 na na na 33.0 38.0 76.2 10.4 22.0 -9.9 11.89% 14.93% 15.06% DES Chapter 5 37