Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

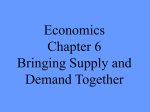

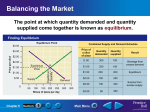

Equilibrium • The point where quantity demanded and quantity supplied come together is known as equilibrium. • It is the point of balance between price and quantity where the market for a good is stable. • If the market price or quantity is anywhere but equilibrium, the market is in a state that economists call disequilibrium. Chapter 6 Section Main Menu Balancing the Market Graphical Representation of Equilibrium Finding Equilibrium Equilibrium Point Combined Supply and Demand Schedule $3.50 $2.50 $2.00 Equilibrium Price $1.50 $1.00 $.50 Supply 0 Chapter 6 50 a Equilibrium Quantity Price per slice $3.00 Demand 100 150 200 250 300 Slices of pizza per day Section Price of a slice of pizza Quantity demanded Quantity supplied $ .50 300 100 $1.00 250 150 $1.50 200 200 $2.00 150 250 $2.50 100 300 $3.00 50 350 350 Main Menu Result Shortage from excess demand Equilibrium Surplus from excess supply Market Disequilibrium There are two causes for disequilibrium: Excess Demand (Shortage) Excess Supply (Surplus) • Quantity demanded > than quantity supplied. • Quantity supplied > quantity demanded. Buyers and sellers will always push the market back towards equilibrium. Chapter 6 Section Main Menu Shifts in Supply • Advances in New Technology • Input Costs • Govt. Regulations/Taxes/Subsidies • Futute Expectations in Price • Global Economy • Shifts in Supply Cause the market to find a new equilibrium point Chapter 6 Section Main Menu Shifts in Demand • Change in Income • Consumer Expectations • Change in Population • Trends/Fads • Price of Related Goods • Shifts in Demand cause the market to find a new equilibrium point. Chapter 6 Section Main Menu Analyzing Shifts in Supply and Demand Graph A: A Change in Supply Graph B: A Change in Demand $800 $60 a Supply $50 b Original supply $40 c Price Price $600 $400 c $30 a b $20 $200 New supply Demand New demand Original demand $10 0 1 2 3 4 5 0 100 Output (in millions) 200 300 400 500 600 700 800 Output (in thousands) • Graph A shows how the market finds a new equilibrium when there is an increase in supply. Ex. New Technology • Graph B shows how the market finds a new equilibrium when there is an increase in demand. Ex. Tastes & Preferences Chapter 6 Section Main Menu 900 Cell Phones • Shifts in Supply - Chapter 6 Section Main Menu “Tickle Me Elmo” • The toy was introduced in the United States in 1996, quickly becoming a fad. Some parents literally fought other parents in stores to purchase one for Christmas. The dolls' short supply due to the unexpected demand led stores to increase their price drastically. Newspaper classifieds sold the plush toy for hundreds of dollars. People reported that the toy, originally sold for $28.99, fetched as much as $1500. Chapter 6 Section Main Menu Price Ceilings In some cases the government steps in to control prices. A price ceiling is a maximum price that can be legally charged for a good - results in a shortage. When soldiers returned from World War II and started families (which increased demand for apartments), but stopped receiving military pay, many could not deal with the jumping rent. The government put in price controls, so soldiers and their families could pay the rent and keep their homes. However, this increased the quantity demanded for apartments and lowered the quantity supplied, meaning that available apartments were rapidly taken until none were left. Ex. Rent Control Chapter 6 Section Main Menu Price Floors • A price floor is a minimum price, set by the government, that must be paid for a good or service – results in a surplus. Ex. Minimum Wage Chapter 6 Section Main Menu The Role of Prices • What role do prices play in a free market system? • What advantages do prices offer? • How do prices allow for efficient resource allocation? Chapter 6 Section Main Menu The Role of Prices in a Free Market • Prices serve a vital role in a free market economy. • Prices help move land, labor, and capital into the hands of producers, and finished goods in to the hands of buyers. • Prices create efficient resource allocation for producers and a language that both consumers and producers can use. Chapter 6 Section Main Menu Advantages of Prices Prices provide a language for buyers and sellers. 1. Prices as an Incentive Communicate to both buyers and sellers whether goods or services are scarce or easily available. 2. Signals High price - producers need to make more. Low price – producers need to make less. 3. Flexibility 4. Price System is "Free“ •http://www.youtube.com/watch?v=ROcI2 jQH5y0&feature=results_video&playnext =1&list=PL7A63123C2AE0F722 Chapter 6 Section Main Menu Efficient Resource Allocation • Resource Allocation – A market system, with its fully changing prices, ensures that resources go to the uses that consumers value most highly. • Market Problems – Imperfect competition – Spillover costs, or externalities, are costs of production, such as air and water pollution, that “spill over” onto people. – If buyers and sellers have imperfect information on a product, they may not make the best purchasing or selling decision. Chapter 6 Section Main Menu

![[A, 8-9]](http://s1.studyres.com/store/data/006655537_1-7e8069f13791f08c2f696cc5adb95462-150x150.png)