727-200 What this Subdivision is about

... 727-625 Total gain reductions not to exceed total loss reductions ...

... 727-625 Total gain reductions not to exceed total loss reductions ...

John G. Llewellyn, PLLC

... Just one entity, or many? Although some investors form only one LLC or corporation to hold all of their properties, some set up separate entities for each property. The factors to consider in determining whether to form one or more entities include, but are not limited to: the number of properties, ...

... Just one entity, or many? Although some investors form only one LLC or corporation to hold all of their properties, some set up separate entities for each property. The factors to consider in determining whether to form one or more entities include, but are not limited to: the number of properties, ...

Wahlen_1e_IM_Ch16 (new window)

... 3. Step 3. Develop a ranking of the impact of each convertible preferred stock and convertible bond on DEPS, from the most dilutive to the least dilutive 4. Step 4. Beginning with the most dilutive security first, include each dilutive convertible security in DEPS in a sequential order based on the ...

... 3. Step 3. Develop a ranking of the impact of each convertible preferred stock and convertible bond on DEPS, from the most dilutive to the least dilutive 4. Step 4. Beginning with the most dilutive security first, include each dilutive convertible security in DEPS in a sequential order based on the ...

Financial Accounting and Accounting Standards

... restrictions, as long as it does not violate its state incorporation law. ...

... restrictions, as long as it does not violate its state incorporation law. ...

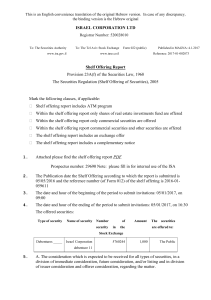

Shelf Offer

... Unit Price will be accepted in part such that each requesting part will receive, from the total Units offered that remain for distribution after acceptance of the requests that include a unit price that is greater than the Uniform Unit Price (and after acceptance of the requests of the classified in ...

... Unit Price will be accepted in part such that each requesting part will receive, from the total Units offered that remain for distribution after acceptance of the requests that include a unit price that is greater than the Uniform Unit Price (and after acceptance of the requests of the classified in ...

Does Financial Constraint Affect Shareholder Taxes and the Cost of

... equity capital is larger for those financially constrained stocks that are held disproportionately by taxable individual investors, who are subject to the shareholder taxes that were reduced, than for financially constrained firms that tend to access capital from sources that were unaffected by the ...

... equity capital is larger for those financially constrained stocks that are held disproportionately by taxable individual investors, who are subject to the shareholder taxes that were reduced, than for financially constrained firms that tend to access capital from sources that were unaffected by the ...

1MB - The Treasury

... for the amount paid for newly issued shares in an innovation company, where the amount is paid either directly to the innovation company or indirectly through a qualifying innovation fund. An investor can invest in innovation companies; innovation funds; or into both. As the offset is non-refundable ...

... for the amount paid for newly issued shares in an innovation company, where the amount is paid either directly to the innovation company or indirectly through a qualifying innovation fund. An investor can invest in innovation companies; innovation funds; or into both. As the offset is non-refundable ...

Luxembourg Reserved Alternative Investment Fund (RAIF)

... Linklaters LLP is a limited liability partnership registered in England and Wales with registered number OC326345. It is a law firm authorised and regulated by the Solicitors Regulation Authority. The term partner in relation to Linklaters LLP is used to refer to a member of Linklaters LLP or an emp ...

... Linklaters LLP is a limited liability partnership registered in England and Wales with registered number OC326345. It is a law firm authorised and regulated by the Solicitors Regulation Authority. The term partner in relation to Linklaters LLP is used to refer to a member of Linklaters LLP or an emp ...

Transcript

... organization. The first question they have to ask themselves is whether to use equity or debt financing when funding capital projects. The main difference between equity and debt financing is with debt financing the creditor receives the repayment of money loaned in full plus interest and with equit ...

... organization. The first question they have to ask themselves is whether to use equity or debt financing when funding capital projects. The main difference between equity and debt financing is with debt financing the creditor receives the repayment of money loaned in full plus interest and with equit ...

Condensed Income Statement

... Rationale: In general, we want to show all “special” pre-tax items as after-tax items. Therefore, we want to show what the tax would have been if these pre-tax items had been reported as after-tax items. (1) Add back tax that was deducted due to merger and restructuring costs shown on pre-tax basis. ...

... Rationale: In general, we want to show all “special” pre-tax items as after-tax items. Therefore, we want to show what the tax would have been if these pre-tax items had been reported as after-tax items. (1) Add back tax that was deducted due to merger and restructuring costs shown on pre-tax basis. ...

PTA005 - State Revenue Office

... K is the number of business kilometres travelled during the financial year. R is the exempt rate. The exempt rate is the rate prescribed under the income tax legislation for calculating a deduction for car expenses for a large car using the cents per kilometre method in the financial year immediatel ...

... K is the number of business kilometres travelled during the financial year. R is the exempt rate. The exempt rate is the rate prescribed under the income tax legislation for calculating a deduction for car expenses for a large car using the cents per kilometre method in the financial year immediatel ...

Ch 8 - Finance

... using smooth annual growth rate based on the five-year average growth from the residual model. ...

... using smooth annual growth rate based on the five-year average growth from the residual model. ...

25-14 - Florida Administrative Code

... that may be invested in the equity of the subsidiary where a parent-subsidiary relationship exists and the parties to the relationship join in the filing of a consolidated income tax return. (1) Where the regulated utility is a subsidiary of a single parent, the income tax effect of the parent’s deb ...

... that may be invested in the equity of the subsidiary where a parent-subsidiary relationship exists and the parties to the relationship join in the filing of a consolidated income tax return. (1) Where the regulated utility is a subsidiary of a single parent, the income tax effect of the parent’s deb ...

Quiz Part A

... 5. What type of accounts are accounts receivable and accounts payable? a. Cash accounts. b. Operating accounts. c. Financing accounts. d. Investing accounts. 6. What is implied if the accounts receivable account has increased? a. Cash flow from operating activities is greater relative to net income ...

... 5. What type of accounts are accounts receivable and accounts payable? a. Cash accounts. b. Operating accounts. c. Financing accounts. d. Investing accounts. 6. What is implied if the accounts receivable account has increased? a. Cash flow from operating activities is greater relative to net income ...